Why Smart People Switch (And What Stops The Rest)

Let's be honest, insurance isn't exactly a fun topic. We tend to see it as just another bill, something we set up once and then try to forget about. But this "set it and forget it" approach can actually drain your wallet. People often stick with the same insurance provider for years, even when there are better deals out there. It's that old "better the devil you know" thinking, and insurance companies know it.

This inertia is often rooted in the fear of hassle. We imagine mountains of paperwork, endless phone calls, and the dreaded coverage gap. These worries, though understandable, are usually blown way out of proportion. Switching insurance providers is typically much smoother than we anticipate. The potential savings, however, are very real. I've personally seen friends save hundreds, even thousands, just by shopping around. One friend, absolutely convinced she had the lowest rate on her car insurance, finally switched after years of putting it off. She ended up saving 15% – enough for a nice weekend getaway!

Cost savings are a huge motivator for people making the switch. Global insurance premiums saw an 8.6% jump in 2024, surpassing inflation in many areas. Learn more about insurance trends here. This has naturally pushed more people to look for better prices. For example, 12% of Australian households switched insurers in 2023. Still, a surprising 70% of consumers stay put, often because of loyalty discounts or automatic renewals. Those who do switch in Germany save an average of 15% on their premiums.

Another thing that keeps people stuck with their current providers is the clever tactics used by the insurance companies themselves. Take those "loyalty" discounts, for instance. They're designed to make you feel like a valued customer, but you're often paying more for your loyalty. They frame it as a special deal, but new customers might be getting even better introductory rates. Then there are auto-renewals – convenient, yes, but they can lock you into another year without you even noticing. Breaking free from these subtle traps is the first step to taking control of your insurance costs and finding a policy that truly works for you.

To help illustrate this further, let's look at a comparison of the factors influencing these decisions:

To get a clearer picture of why people switch or stay, let’s take a look at this table:

Common Reasons People Switch vs. Stay With Current Insurance: A comparison of motivating factors for switching insurance providers versus reasons people stay with their current provider

| Reasons to Switch | Reasons to Stay | Impact Level |

|---|---|---|

| Lower Premiums | Loyalty Discounts | High |

| Better Coverage | Inertia/Fear of Hassle | High |

| Improved Customer Service | Established Relationship with Agent | Medium |

| Negative Experiences (e.g., Claim Denial) | Auto-Renewal | Medium |

| Recommendations from Friends/Family | Perceived Lack of Better Options | Low |

| Bundling Options with Other Insurance Needs |

This table summarizes the push and pull factors affecting insurance decisions. As you can see, cost and coverage are major drivers for switching, while perceived hassle and loyalty programs often keep people anchored to their existing policies.

Let's not forget the paperwork, either! No, wait, scratch that! As I mentioned earlier, most of us overestimate the hassle factor.

Decoding What You Actually Have Right Now

Before you even start thinking about switching insurance providers, take a good look at your current coverage. Don't just glance at your policy documents – really dig in and become an insurance detective. I can’t tell you how many times I've seen people completely blindsided, realizing they were either drastically underinsured or paying through the nose for coverage they didn't even need.

I had a friend, Mark, who was paying a hefty premium for "comprehensive" car insurance. He was convinced he was covered for anything and everything. Then his car was damaged in a flood, and he found out the hard way that "comprehensive" didn’t actually include flood damage. Expensive lesson!

This screenshot from Insurance.com shows a typical interface for comparing insurance quotes. Sites like these can be overwhelming, which is why understanding your existing coverage is so important. If you know exactly what you need, comparing different plans becomes much easier – like comparing apples to apples.

So, how do you decode your current policy? Start by creating a coverage inventory. This isn’t just a list of what's covered, it's about understanding your coverage limits. What's the actual dollar amount your policy will pay out in different situations? Your liability coverage might be fine for a minor fender bender, but what if you're at fault for a more serious accident? Suddenly, those cryptic numbers on your policy become very important. Don’t hesitate to call your current provider and ask them to explain anything you’re unsure about.

Next, look for coverage gaps. These are situations where you think you're covered, but actually aren't. Think about things like flood insurance, earthquake coverage, or specific types of liability. These are often separate add-ons that can have major financial implications if you’ve overlooked them. My friend Sarah found this out when a pipe burst in her condo. The resulting water damage wasn’t covered by her basic homeowner’s insurance, leaving her with a mountain of repair bills.

Finally, check for any red flags with your current policy. Are your premiums constantly creeping up for no apparent reason? Have you had a nightmare trying to file a claim? These could be signs that it’s time to look at other insurance providers.

Taking the time to understand your current coverage might seem like a chore, but it’s the key to switching providers effectively. It’s the foundation for finding a policy that genuinely meets your needs and your budget, and not just one that sounds good on paper.

Shopping Strategies That Actually Save You Money

So, you're thinking about switching insurance? Excellent! Let me give you some insider tips before you get bogged down with online quotes and endless phone calls. Trust me, a little strategy goes a long way in saving you both time and cash.

A lot of people assume comparison websites are the magic bullet. They are great for a quick snapshot of what's out there, but they don’t always show you the whole picture. Going directly to an insurance company can sometimes unlock special deals you won’t find on aggregator sites. Think smaller, specialized insurers, or maybe you have some specific needs that aren't easily categorized. I've known people who had no luck on comparison sites, only to find amazing rates by going direct.

Another thing to consider is timing. Believe it or not, shopping around for insurance too close to your renewal date can sometimes raise red flags. It might sound strange, but starting your search a few weeks before your renewal can actually get you better offers. It gives you breathing room to compare without that looming deadline. Speaking of which, timing can even affect your liability coverage. Here's something you might find useful: Liability Insurance for Employees.

Technology has really shaken things up in the insurance world. It's so much easier to shop around and switch these days. Online aggregators now grab 30% to 60% of new insurance sales in developed countries, which is pretty impressive. Check out this article for more info. In the US, switching car insurance online can often be done in under 30 minutes – a far cry from the days of paperwork and endless waiting. Interestingly though, only about 30% of insured people in Europe and North America fully trust digital-only insurers. Shows you that some people are still hesitant about service and security.

Don’t forget the power of negotiation! A polite conversation with an agent can sometimes work wonders. You might snag a discount or get better terms. Just avoid aggressive haggling; it can really backfire. Remember, you're trying to build a relationship with a company you’ll be relying on if things go wrong. Building rapport is much more effective than burning bridges. Also, asking the right questions is key. Don't just focus on price. Make sure you understand the details of the coverage and what’s not covered. That way, you'll avoid any nasty surprises later on.

Reading Between The Lines Of Insurance Quotes

Getting insurance quotes is easy. Understanding them? That’s where most people get tripped up. We're going to dive deeper than just the price and break down what you're actually getting for your money. I've seen firsthand how seemingly small differences can cost people big time down the road. For example, a friend thought she was saving money with a lower deductible, but her coverage limits were so low she was left high and dry after an accident.

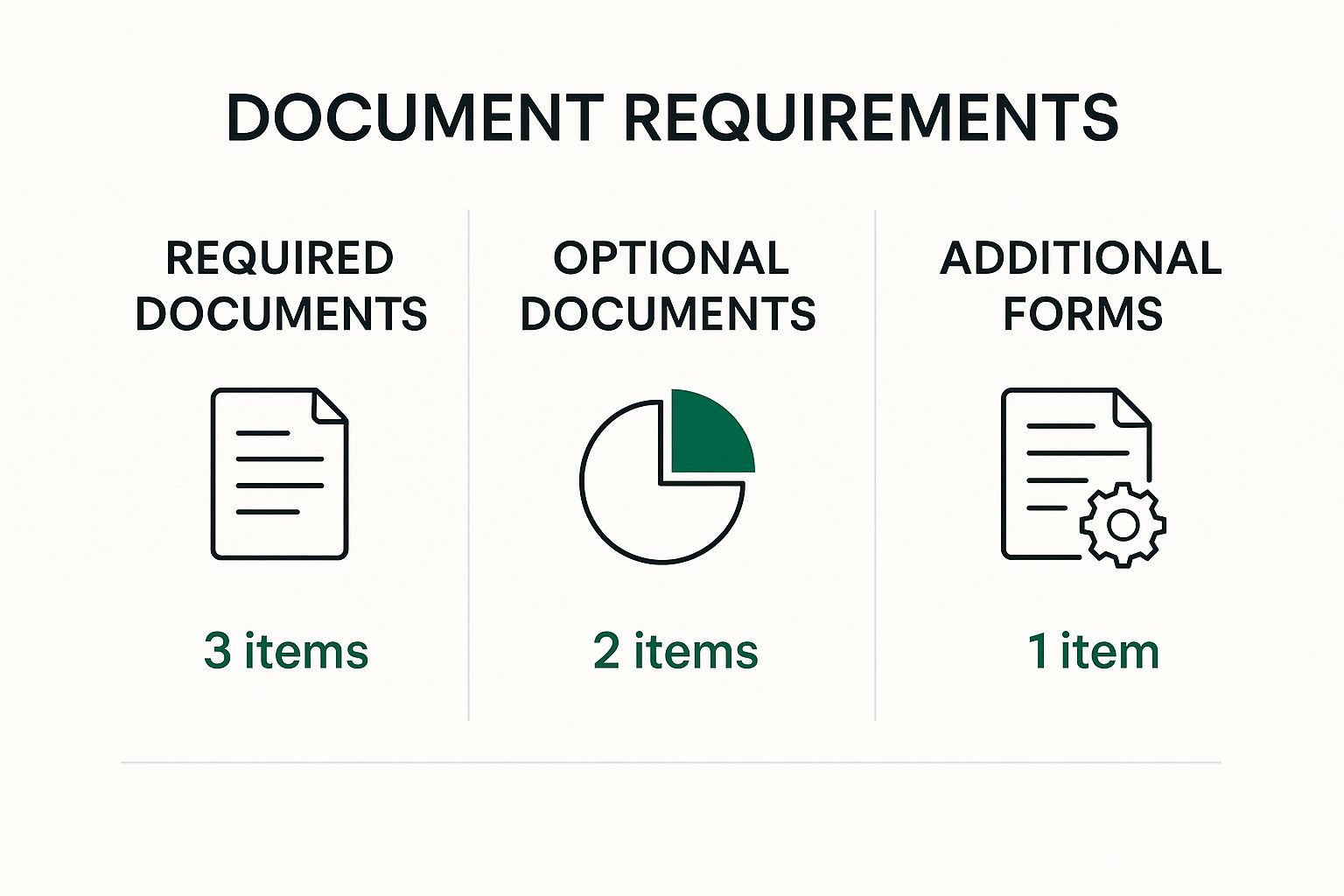

This infographic shows the paperwork typically involved in switching insurance providers. It outlines required, optional, and additional forms. Being organized upfront really does save headaches later. Knowing what to expect streamlines the whole process.

One of the biggest mistakes is fixating only on the premium – your monthly payment. A lower premium is tempting, but it usually means compromises elsewhere. A lower premium might mean a higher deductible – the amount you pay before your insurance kicks in. So, while you save monthly, a claim could hit you hard.

Hidden Factors That Affect Your Rates

Many things can quietly inflate your premiums. For example, your credit score can play a surprising role. Insurers use it as a risk indicator. Your location, age, and even your job can impact your rates. Two people with identical cars and driving histories can pay completely different premiums.

Getting Honest Quotes: Present Yourself Strategically

When getting quotes, be upfront about your needs. Don't try to game the system for a lower price. It can seriously backfire. For example, underestimating your annual mileage could invalidate your insurance after an accident. And ask questions! A good agent will appreciate them. Anyone who seems evasive might be hiding something. Ask about coverage limits, exclusions, and the claims process.

Learning From Others' Mistakes

I’ve heard so many stories of people thinking they got an amazing deal, only to discover their coverage was worthless when they needed it most. A family I know bought a homeowners policy with rock-bottom premiums. Then a fire damaged their house. Their policy didn't cover rebuilding costs, leaving them in a terrible spot. Don't repeat these mistakes!

Comparing quotes isn't about the lowest price; it's about the best value. Understanding the details makes all the difference. Switching insurance providers effectively takes research, planning, and smart decisions.

Before we go any further, let's take a look at the table below to understand the key factors to compare when you're evaluating those insurance quotes. It's not just about the bottom line!

| Factor | Why It Matters | Questions to Ask |

|---|---|---|

| Deductible | The amount you pay out-of-pocket before your insurance kicks in. | What deductible can I comfortably afford? How does the deductible affect the premium? |

| Coverage Limits | The maximum amount your insurance will pay for a covered loss. | What are the coverage limits for different types of losses? Are these limits sufficient for my needs? |

| Exclusions | Specific situations or events not covered by the policy. | What are the specific exclusions in this policy? Are there any common risks that are not covered? |

| Claims Process | The steps involved in filing and resolving a claim. | How do I file a claim? What is the typical turnaround time for claims processing? |

| Customer Service | The quality of support provided by the insurance company. | How can I contact customer service? Are there online resources available? |

| Financial Stability | The insurer's ability to pay out claims. | What is the financial strength rating of this company? Are they likely to be able to handle a large claim? |

This table highlights the importance of looking beyond the premium when comparing insurance quotes. Understanding these factors will help you make an informed decision and choose the policy that best fits your individual needs and risk tolerance. Remember, peace of mind is priceless.

Making The Switch Without Losing Your Mind

Switching insurance providers can feel daunting, like navigating a minefield of paperwork and potential pitfalls. But honestly, it’s not nearly as bad as you might think. With a little planning and a proactive approach, the process can be surprisingly smooth.

One of the biggest tips I can offer is to start early. Ideally, begin shopping around a few weeks before your current policy is up for renewal. This gives you ample time to compare quotes, finalize your new policy, and—crucially—avoid any gaps in coverage. Believe me, a lapse in coverage is a headache you don't want. It leaves you vulnerable financially and can complicate things down the line.

Speaking of your old policy, don't just assume it magically disappears when your new one kicks in. Be strategic about the cancellation. Get the cancellation date confirmed in writing from your current provider, and make absolutely sure any automatic payments are deactivated. I've heard too many stories of people accidentally paying for two policies at once because they overlooked this step!

Handling The Paperwork

Now, let's talk about the paperwork. I know, it's nobody's favorite thing, but it's usually less painful than it seems. Gather all the documents your new provider needs. This will typically include proof of identification, details about your prior insurance, and maybe some vehicle information if we’re talking car insurance. My golden rule? Keep copies of everything. Seriously, you never know when you might need them. A friend of mine learned this the hard way when her claim was initially denied because the insurer claimed they'd lost her proof of prior coverage. Luckily, she had copies and was able to straighten things out, but it was a hassle she could have avoided.

It's interesting to see how insurance switching habits actually vary. In the UK, for instance, nearly 79% of people who considered switching actually went through with it. Compare that to the US, where only about 16% of shoppers switched in 2022. Discover more insights on insurance switching trends. It makes you wonder why so many people stick with policies that might not be the best fit anymore. Maybe it’s the perceived hassle, or maybe it’s just plain inertia.

Communication Is Key

Communication is your best friend throughout this process. Stay in touch with both your old and new providers. Confirm that they’ve received all necessary documents, ask questions if anything is unclear, and don't hesitate to follow up. Being proactive can save you a lot of grief later on. By the way, while you're at it, you might find this interesting: You might be interested in: How Much Umbrella Insurance Do I Need?

Think of switching insurance providers like moving to a new home. There's the initial excitement of a potential fresh start, maybe even some cost savings, but there's also the unavoidable process of packing, unpacking, and getting settled. It takes a bit of effort, but the benefits—better coverage, lower premiums, and greater peace of mind—are often worth it. Don’t let inertia or fear hold you back from finding a policy that truly meets your needs. With a little planning and a proactive approach, switching insurance can be a manageable, and even rewarding, experience.

Dodging The Landmines That Trip Up Most Switchers

Switching insurance can feel a bit like tiptoeing through a minefield, right? Even if you're super careful, it's easy to make a costly mistake. I've heard horror stories from friends who thought they'd snagged an amazing deal, only to find some nasty surprises lurking down the road. So let's talk about some of the common traps and how to avoid them.

One biggie is the coverage gap. This is when you cancel your old policy before the new one kicks in, leaving you temporarily without coverage. It sounds simple enough to avoid, but you'd be surprised how often it happens. Make absolutely sure you double-check those dates! Seriously, set a calendar reminder – confirming that new effective date before canceling your old policy can save you a world of headache.

Another landmine is skimming over the fine print. Don't just fixate on the premium; dig into the policy details. What are the deductibles, coverage limits, and exclusions? A friend of mine switched car insurance to save a few dollars a month, but his new policy had significantly lower property damage limits. He ended up paying thousands out of pocket after an accident. This is a good time to think about extra coverage options, too. Maybe an umbrella policy is something you need: Read also: What Does a Personal Umbrella Policy Cover?

The Emotional Rollercoaster of Switching

Believe it or not, switching insurance can be an emotional experience. You might get a little buyer's remorse, especially if your old provider starts calling with sweet deals to lure you back. This is totally normal! Just remember why you switched in the first place. Was it a better price? Better coverage? Focus on your original reasons and resist the urge to second-guess yourself.

Some companies can get pretty aggressive trying to keep your business. They might try to make switching seem incredibly complex or warn you about losing valuable benefits. Don't let these scare tactics get to you. You have the right to choose the insurance that works best for you. Stay confident in your decision.

Staying Grounded Amidst the Doubts

Even after you’ve made the switch, doubts can still sneak in. "Did I do the right thing?" "Is my new provider reliable?" These are totally natural feelings. To ease these anxieties, have a reality check strategy. Keep your new policy handy and review it from time to time. Remind yourself of the advantages you gained by switching. Talking to others who have successfully switched insurers can also be really helpful. Their experiences can reassure you and reinforce that you've made a smart choice. You did your homework, made an informed decision, and you’re in the driver’s seat when it comes to your insurance.

Making Your New Insurance Relationship Actually Work

So, you switched insurance providers? High five! That's a big one ticked off the list. But now comes the part where you make sure that shiny new policy really works for you. It's not just about paying your premiums on time (although that's important too!), it's about building a relationship with your insurer that brings you actual value and peace of mind.

First things first, get online! Seriously. Most insurers have online portals these days – think of them as your insurance command center. You can manage your policy, pay bills, even file claims, all from your couch. Trust me, setting this up early will save you headaches later. I learned this the hard way when my parents switched home insurance and never bothered with their online account. When a storm took a chunk out of their roof, tracking the claim was a nightmare because they couldn't access anything online.

Understanding the Claims Process

Speaking of claims, don't wait until disaster strikes to figure out how it all works. Take some time to familiarize yourself with your new insurer's claims process. How do you file a claim? What documents do you need? How long does it usually take? Knowing what to expect beforehand can make a stressful situation so much smoother. It's like having a game plan before the game even starts.

Reviewing and Adjusting Your Coverage

Life has a funny way of throwing curveballs. You buy a house, get married, welcome a new little one into the family, or land that dream job. All these milestones usually mean your insurance needs change too. Don't let your policy sit in a drawer gathering dust. Review it at least once a year, or any time you have a major life change, to make sure it still fits your needs. And remember, reviewing doesn't just mean adding more coverage. Sometimes, you can actually reduce coverage and save some money. For instance, when my kids flew the coop, my husband and I realized we could lower our life insurance coverage and free up some cash.

Staying Ahead of the Game: Annual Review Techniques

Make a date with your insurance policies once a year. I know, it doesn't sound thrilling, but it's important. Compare what you have with what other insurers are offering. Don't be shy about shopping around for quotes. You might be pleasantly surprised by a better deal, or you might realize your current provider isn't the right fit anymore. A friend of mine was stunned to find she could get the exact same coverage from another company for 20% less! She’d been with the same insurer for a decade, thinking loyalty meant savings, but it turns out she was wrong.

Being proactive with your insurance is all about staying in control of your costs and making sure you're getting the best value. Think of it as a partnership, not just a transaction. By building a solid relationship with your insurer, understanding your coverage, and regularly reviewing your policies, you're putting yourself in the driver's seat and protecting your financial well-being.

Ready to experience the Wexford difference? Visit Wexford Insurance Solutions today for a personalized insurance plan that fits your unique needs.

Management Liability Coverage: Essential Guide for Business OwnersDefine Health Insurance Premium: Smart Guide to Real Costs

Management Liability Coverage: Essential Guide for Business OwnersDefine Health Insurance Premium: Smart Guide to Real Costs