Understanding Your Financial Safety Net (And Why It Matters More Than You Think)

For many, homeowners insurance feels like just another bill tied to a mortgage—a required expense you pay without much thought. But looking at it this way means missing its true purpose. A solid policy is one of the most important financial shields you can own. Think of it as a personal bodyguard for your home, your most significant asset, always on duty. While you hope you never need to call on it, its presence offers incredible peace of mind and protects your family’s financial future from unexpected disasters.

This isn’t just a gut feeling; it’s a reality reflected in global economics. The home insurance market was valued at around USD 234.6 billion in 2024 and is expected to continue growing. This huge number shows that homeowners everywhere are making it a priority to protect their properties. In fact, coverage for the physical structure of the home makes up over 71% of the market, which tells us that people see their homes as more than just buildings—they are the foundation of their financial stability. You can read more about these global insurance market trends and their drivers to get a fuller picture.

The Real Value: Beyond Bricks and Mortar

Smart homeowners view their policy as an investment in security, not just a recurring cost. Picture this: a major storm tears through your town and a tree smashes through your roof. Without insurance, you’d be looking at tens of thousands of dollars in out-of-pocket repairs, a bill that could wipe out your savings or push you into debt. With the right coverage, however, that financial catastrophe becomes a manageable problem. The real value is in this transfer of risk—moving the financial burden from your shoulders to your insurer’s.

Data from the Insurance Information Institute shows just how often the unexpected happens, highlighting the most common reasons for home insurance claims.

This chart makes it clear that events like wind, hail, fire, and lightning are major sources of property damage. It reinforces why any good guide to homeowners insurance needs to focus on preparing for things that are completely out of our control.

The Psychological Comfort of Being Prepared

Beyond the numbers, having the right coverage provides a huge psychological benefit. It’s the freedom to sleep soundly, knowing that a burst pipe or a kitchen fire won't lead to financial ruin. When disaster strikes, homeowners tend to tell one of two stories:

- The Prepared: These are the people who took the time to understand their policy. They feel relieved and grateful for their foresight as they navigate the claims process, rebuild, and move forward.

- The Unprepared: These homeowners often chose the cheapest, most basic plan available. They discover critical gaps in their coverage when it's far too late, learning a difficult lesson about the real cost of cutting corners.

Ultimately, this isn’t about being pessimistic. It’s about being empowered. Taking the time to understand your policy is the first step toward true peace of mind, giving you confidence that you have a strong plan to protect your family and your future, whatever comes your way.

Decoding The Coverage Maze (What Actually Gets Protected)

Trying to understand a homeowners policy can often feel like you're assembling a complex puzzle without the picture on the box. It’s not just one big safety net; think of it more like a specialized toolkit. Each tool, or coverage type, is designed for a very specific job, protecting a different piece of your property and financial life. Knowing what each tool does is the first step to making sure you're properly covered.

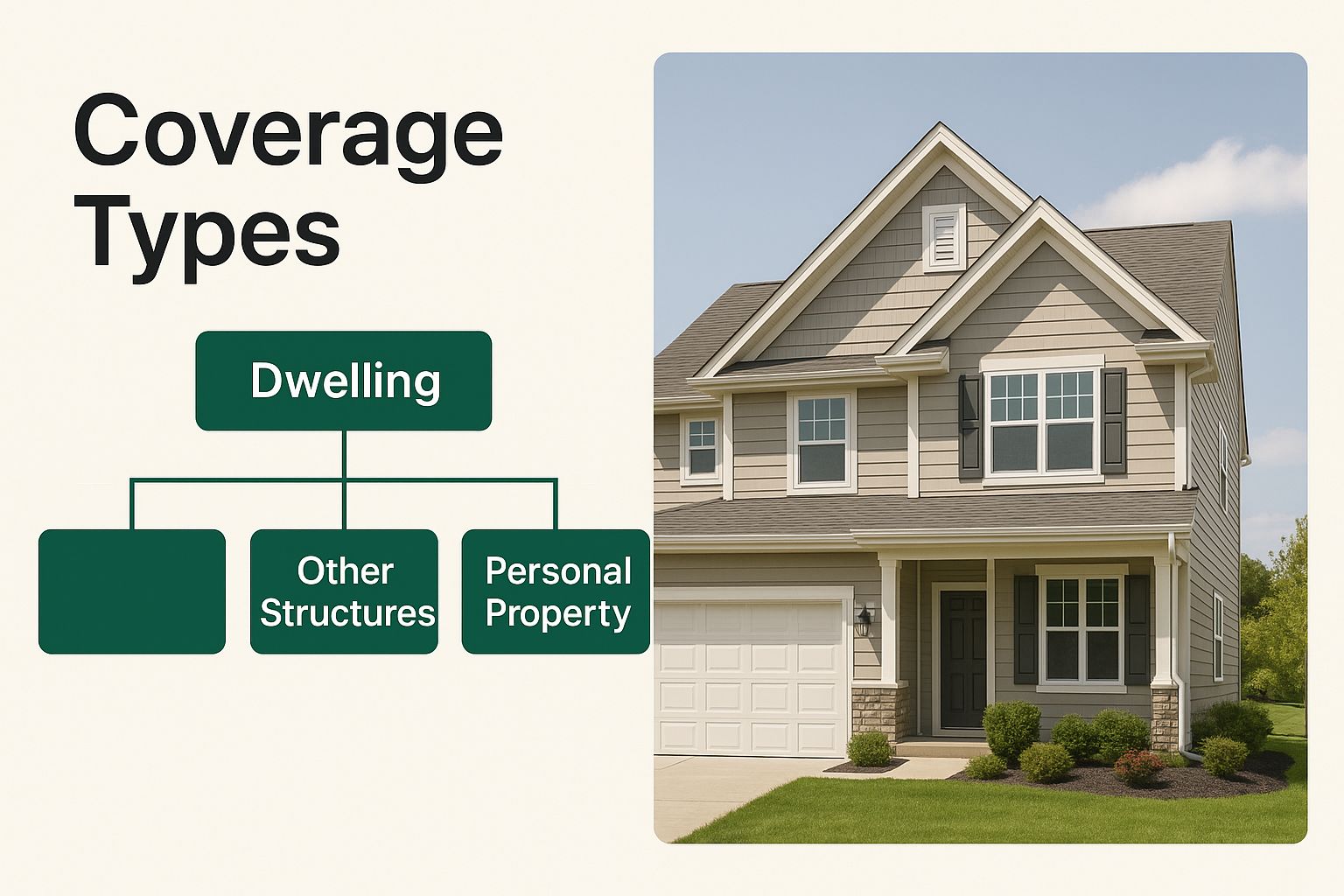

This infographic shows the main types of coverage you'll find in a standard policy.

As you can see, a policy layers different protections, beginning with your home’s structure and branching out to cover your belongings, personal liability, and even the costs of living elsewhere if your home is damaged.

The Four Pillars Of A Standard Policy

A typical guide to homeowners insurance will show that policies are built around four main coverage types, each with a distinct purpose:

- Dwelling Coverage (Coverage A): This is the core of your policy. It protects the physical structure of your house—the roof, walls, and foundation—plus any attached structures, like your garage. If a fire or a powerful storm damages your home, this is the coverage that funds the repairs or rebuild.

- Personal Property Coverage (Coverage C): Imagine everything you own inside your home—from your couch and TV to your clothes and kitchen gadgets. This coverage helps you replace those items if they are stolen, damaged, or destroyed. It often follows you, covering possessions even when they're outside your home, like a laptop taken from your car.

- Liability Protection (Coverage E): This part acts as your financial shield if you're found legally responsible for injuring someone else or damaging their property. For example, if a visitor slips and falls on your icy walkway and decides to sue, this coverage helps with legal defense costs and any potential settlement.

- Additional Living Expenses (Coverage D): If a covered event like a fire makes your home unlivable, this coverage steps in to pay for reasonable living costs. This could include hotel stays, restaurant meals, and laundry services while your home is under repair.

Knowing What Isn't Covered

A frequent and costly mistake is believing a standard policy covers every possible disaster. For example, most basic policies specifically exclude damage from floods and earthquakes. This is a critical distinction. One homeowner might have their claim for a kitchen fire fully paid, while their neighbor’s claim for a flooded basement after a hurricane is denied. This isn't arbitrary; it reflects the need for separate, specialized policies for certain high-risk events. To learn more, it's worth exploring the differences between flood insurance vs. homeowners insurance to see if you need both.

The National Association of Insurance Commissioners (NAIC) offers clear guidance on what is typically covered and what is left out.

This resource highlights that you, as the homeowner, must be proactive. It's your job to find potential gaps in your standard policy and purchase extra protection if needed. Other common exclusions include sewer backups and damage from poor maintenance, which makes reading the fine print of your policy essential.

The Hidden Forces Behind Your Premium (Why You Pay What You Pay)

Have you ever looked at your homeowners insurance bill and wondered why it costs what it does? It’s not just a random number. Insurers use a detailed recipe to figure out your premium, mixing together information about your home, where you live, and even your personal history. This explains why you and your neighbor might have nearly identical houses but pay very different rates. A good guide to homeowners insurance should pull back the curtain on these factors, giving you the power to manage your costs.

Insurance costs aren't set in stone; they move with bigger economic and environmental shifts. Lately, homeowners across the country have seen prices climb. In 2024, new policies jumped by an average of 17.4%. This increase is a result of inflation, more frequent severe weather, and rising costs for the insurance companies themselves. You can discover more insights about these 2025 home insurance predictions to get a sense of where the market is headed. In this climate, knowing exactly what drives your premium is more crucial than ever.

Your Home's Unique Risk Profile

The first ingredient in the premium recipe is your house itself. Insurers examine its specific characteristics to estimate how likely you are to file a claim and how much it might cost.

- Age and Construction: An older home with original wiring or plumbing is often considered a higher risk than a brand-new house. Likewise, a brick home is tougher against fire and wind than one with wood siding, which can lead to a lower premium.

- Roof Condition: The age and material of your roof are very important. A new, impact-resistant roof is your home’s main defense against storms and can earn you a significant discount.

- Attractive Nuisances: Think of these as fun features that also add risk. Things like swimming pools or trampolines increase the chances of someone getting hurt on your property, which can raise your liability coverage costs.

Location, Location, and Micro-Location

Where you live plays a huge role, and it's more specific than just your city or zip code. Insurers zoom in on hyper-local data to pinpoint risk.

- Proximity to a Fire Department: Being close to a fire station and a fire hydrant means help can arrive faster. This can reduce potential damage and, in turn, lower your insurance rate.

- Local Crime Rates: If you live in an area with more break-ins or vandalism, you can expect your insurance costs to be higher to reflect that risk.

- Natural Disaster History: Living in a region known for hurricanes, tornadoes, or wildfires will almost always mean a higher premium. Insurers use advanced mapping to see how vulnerable your specific property is.

This chart gives a great snapshot of the many moving parts that determine what you pay.

As you can see, everything from your past claims to your credit score has a part to play in the final number. Understanding these hidden forces is the first step toward influencing them. Many of these factors are within your control, and a few smart adjustments could lead to real savings. If you're looking for practical ways to save, you might want to read our article on how to lower home insurance premiums.

Reading The Market Tea Leaves (What Current Changes Mean For You)

The homeowners insurance market is anything but predictable. It’s constantly shifting under the weight of economic pressures, climate events, and new regulations. Understanding these forces gives you a serious advantage, turning you from someone who just pays the bill into a homeowner who can see changes coming before they hit your wallet. This isn’t about predicting the future with a crystal ball; it’s about reading the market signs to make smarter choices for your policy and your budget.

After years of relentless price increases, we're starting to see a potential shift. The insurance world has seen major ups and downs recently, creating both hurdles and opportunities for homeowners. According to Marsh's Global Insurance Market Index, property insurance rates actually declined by 6% worldwide in the first quarter of 2025. This was the third quarter in a row with decreasing rates, following a tough seven-year stretch of non-stop hikes. While some areas are still struggling, this trend hints that a wider market correction could be on the horizon. You can discover more about these global property insurance trends to get the complete picture.

This chart from Marsh clearly shows the recent cooling-off period in global property insurance costs after a long and painful climb. The downward trend is a positive sign for homeowners, suggesting the intense pricing pressure of the last few years might finally be letting up in some places.

Navigating Regional Turbulence

While global trends give us the big picture, the homeowners insurance market is extremely local. Think of it like the weather: a sunny forecast for the country doesn't mean it isn't pouring rain in your specific town. Some areas, especially those at high risk for hurricanes, wildfires, or severe storms, are still dealing with shocking rate increases and even being dropped by major insurance companies. Insurers are getting much pickier about the risks they're willing to cover.

This has split the market into two different realities for homeowners:

- Challenged Regions: In states like Florida, California, and along the Gulf Coast, finding affordable coverage can be a real struggle. In these places, the game is all about mitigation—making your home stronger against specific threats to make you a more appealing customer to insurers.

- Stable Regions: In areas with a lower risk of natural disasters, the recent market stabilization could lead to more competitive prices. If you're in one of these regions, now is an excellent time to shop around for your policy to make sure you're getting the best deal.

Figuring out which category your home fits into is the first step toward building a smart strategy. This insight helps you decide when to look for a new policy or how to negotiate your renewal, putting you in the best position to secure good terms in this ever-changing environment. This is a critical part of any modern guide to homeowners insurance.

Smart Shopping Tactics That Actually Work

Forget the idea of simply snagging the cheapest homeowners insurance policy you can find. A much better approach is to hunt for the best value—solid coverage from a dependable company at a fair price. This calls for a clear strategy, one that goes beyond basic online quote tools to help you truly understand what you're buying. A disciplined shopping process is a central part of any effective guide to homeowners insurance.

The real goal is to compare policies, not just price tags. The cheapest option might come with a sky-high deductible or glaring coverage gaps that could leave you financially vulnerable when you need help the most. A policy that costs a little more might offer far better terms, like replacement cost value for your belongings instead of actual cash value, which could save you thousands after a claim.

How to Compare Quotes Like a Pro

To make a true apples-to-apples comparison, you need to gather several quotes using the same coverage limits and deductibles. Once you have those in hand, it’s time to put on your detective hat and investigate the real value behind each offer.

Here are the critical factors to examine when you're shopping around:

- Coverage Limits: Make sure the dwelling, personal property, and liability limits are identical across all quotes.

- Deductibles: How much will you have to pay out of your own pocket for a claim? A higher deductible means a lower premium, but it also increases your immediate financial risk.

- Special Sub-Limits: Pay close attention to the caps on valuable items like jewelry, art, or electronics. A standard policy might only cover $1,500 for stolen jewelry, which could be a painful surprise.

- Exclusions: What isn't covered? Read the fine print for specific language about events like floods, earthquakes, mold, or sewer backups.

To help you stay organized and make an informed decision, we've put together a checklist of what to look for when comparing insurance providers.

| Comparison Factor | Why It Matters | What to Look For | Red Flags |

|---|---|---|---|

| Coverage Types & Limits | This is the core of your policy. Mismatched limits make a true price comparison impossible. | Identical limits for dwelling, personal property, and liability. Endorsements for specific items. | Quotes with significantly lower limits to appear cheaper. Missing essential coverages like water backup. |

| Deductible Amount | Directly impacts both your premium and how much you pay out-of-pocket after a loss. | A deductible you can comfortably afford. Compare how different deductible levels affect your premium. | A very high deductible that would cause financial hardship. An agent who doesn't explain the trade-offs. |

| Company Financial Strength | A policy is only a promise. You need to know the company can pay claims, especially after a major disaster. | High ratings from agencies like A.M. Best (A- or better is a good benchmark). | Low or unrated financial strength. A history of financial instability. |

| Customer Service & Claims | How a company treats you during a claim is when your policy truly proves its worth. | Positive customer reviews on independent sites. High rankings in claims satisfaction surveys. | A pattern of negative reviews about slow claims processing or poor communication. |

| Discounts & Bundling | These are easy ways to lower your premium without sacrificing coverage. | Multi-policy (home/auto) bundles, security system discounts, new roof credits. | An insurer that offers very few discounts or doesn't proactively apply them. |

| Policy Exclusions | Knowing what isn't covered is just as important as knowing what is. | Clear language on what is excluded (e.g., floods, earthquakes, wear and tear). | Vague or confusing exclusion clauses. Critical exclusions that are not clearly communicated. |

This table serves as your roadmap to a smarter insurance choice. By systematically evaluating each of these factors, you move beyond just price and start to see the true value each insurer offers, ensuring you're not just covered, but well-protected.

This screenshot from Consumer Reports reinforces this idea, showing key areas where homeowners should focus, such as company satisfaction and how claims are handled.

The data serves as a powerful reminder: a policy is only as good as the company that backs it up. This makes customer service and claims satisfaction essential parts of your decision.

Don't Overlook Discounts and Bundling

Insurers provide a variety of discounts, and you shouldn't have to go on a treasure hunt to find them. A good agent will proactively look for every discount you're eligible for. Common savings opportunities include having smoke detectors, a home security system, or a newer roof. One of the biggest ways to save is by bundling your policies. You can learn more about how bundling home and auto insurance can simplify your finances and lower your overall insurance bill.

In the end, smart shopping isn't about speed; it’s about being thorough. By asking the right questions and carefully comparing the details, you can find a policy that delivers both financial security and genuine peace of mind. Your diligence now is your best defense against inadequate coverage later.

Money-Saving Strategies That Don't Compromise Protection

Lowering your homeowners insurance premium doesn't have to mean gutting your coverage and leaving yourself vulnerable. With a thoughtful approach, you can find real savings while keeping your financial safety net intact. The trick is to think like an insurer: what steps can you take to make your home a safer, less risky property to cover? This perspective is a core part of any practical guide to homeowners insurance.

Leverage Discounts and Bundles

One of the fastest ways to save money is by taking advantage of discounts. While bundling home and auto insurance is a well-known strategy, you can often deepen the savings by adding other policies, like umbrella or valuable items coverage, into the mix. Beyond bundling, insurers offer a range of discounts that many homeowners overlook:

- Safety and Security: Installing a centrally monitored security system, smoke detectors, and quality deadbolt locks can often earn you a discount of 5% or more. These are small investments that signal to an insurer that you're serious about preventing loss.

- Disaster Mitigation: If you live in an area prone to storms, adding features like storm shutters or reinforcing your roof can lead to significant premium reductions.

- Loyalty and Claims History: Many companies offer rewards for long-term customers and for those who have been claim-free for several years. It never hurts to ask your provider if you qualify for these perks.

Strategic Home Improvements and Deductibles

Certain home upgrades can pay for themselves over time through lower insurance costs. Installing a new roof, updating old electrical wiring, or modernizing your plumbing reduces the risk of common claims like fires or water damage, which your insurer will recognize.

Another powerful lever you can pull is your deductible—the amount you agree to pay out-of-pocket on a claim before your insurance coverage starts. Simply raising your deductible from $500 to $1,000 can cut your annual premium by as much as 25%. The goal is to find a balance: a deductible high enough to lower your premium but low enough that you could comfortably pay it in an emergency. It's a calculated risk, but one that often makes sense if you maintain a solid emergency fund. Before making a change, it's wise to understand what it means in a real-world scenario; our article on the homeowner insurance claim process breaks down what you can expect.

This screenshot from NerdWallet highlights several common ways to save on homeowners insurance.

As the image shows, saving money isn't about one single trick. It’s a combination of shopping around, making smart home upgrades, and adjusting your policy details.

Improve Your Insurance Score

Finally, your credit-based insurance score has a surprisingly significant impact on your premium. Insurers use this score to predict the likelihood of a future claim. Simple financial habits like paying bills on time, keeping credit card balances low, and avoiding opening too many new lines of credit can improve this score. Over time, a better score can lead to lower insurance costs.

By combining these different strategies—bundling policies, making proactive home upgrades, choosing the right deductible, and maintaining good credit—homeowners can often reduce their premiums by hundreds of dollars annually without sacrificing the protection they need.

Your Action Plan For Insurance Success

Now that you have a solid grasp of how homeowners insurance works, you can create a practical plan to stay protected. This isn’t just about buying a policy and forgetting it; it’s about actively managing your coverage to make sure it keeps up with your life. Think of your policy not as a dusty document in a drawer, but as a living shield that adapts as your circumstances change. A key part of any good **guide to homeowners insurance** is learning how to be the pilot of your own policy.

Establish a Regular Review Rhythm

Your life is always evolving, and your insurance should too. Major life events—like getting married, welcoming a child, launching a business from home, or finishing a big renovation—all have a direct impact on what you need to protect.

Set a yearly reminder on your calendar for an insurance review. This one simple habit is the best way to avoid being underinsured when you need coverage most. During this review, make a point to:

- Update your home inventory: Keep a running list of your belongings, especially after buying expensive items like new electronics or furniture.

- Reassess your liability limits: Are your liability limits high enough to protect your growing assets?

- Talk to your agent about life changes: Let them know about any new risks (like a trampoline) or assets (like a new garage) that need coverage.

This checklist from Insurance.com offers a great framework for your annual review.

This visual guide covers the essential checkpoints, from your deductible to potential discounts, helping you conduct a complete and effective review.

Build a Strong Professional Relationship

Your insurance agent is more than a salesperson; they are your advisor. A dedicated agent will search for opportunities to strengthen your coverage and find ways to save you money. They can break down confusing policy details into simple terms and act as your advocate if you ever need to file a claim. Finding a responsive and knowledgeable agent means you’ve gained a partner in your long-term financial security.

It's also important that your agent has their own professional liability coverage. To understand how insurance professionals protect themselves, you might find our article on what is errors and omissions insurance insightful.

Stay Informed and Adapt

The insurance world doesn't stand still. New products, changing regulations, and emerging risks like cyber threats or new weather patterns constantly appear. Pay attention to trends in your local area, especially those related to natural disasters. Subscribing to financial blogs or industry newsletters is a simple way to stay current. By taking an active role, you can ensure your homeowners policy remains a reliable source of security, safeguarding your home and family for years to come.

Ready to put your action plan into motion with a team of dedicated experts? At Wexford Insurance Solutions, we offer the personalized guidance you need to secure the right protection. Contact us today to schedule your complimentary policy review and take the first step toward real insurance confidence.

What Is Errors And Omissions Insurance? Your Essential GuideHigh Value Home Insurance: Protect Your Luxury Home

What Is Errors And Omissions Insurance? Your Essential GuideHigh Value Home Insurance: Protect Your Luxury Home