Think of flight school insurance as a custom-built safety net, specifically woven to catch the unique risks that come with training new pilots. It’s not just about protecting your planes; it’s a comprehensive package designed to safeguard your instructors, students, and the business itself from the high-stakes environment of flight training. This is more than just a policy—it’s an essential shield for your operation.

Why Your Flight School Needs Specialized Insurance

You wouldn't use your personal car insurance to cover a fleet of taxi cabs, right? The same logic applies here. A standard policy for a private aircraft owner just doesn't cut it for a flight school. The risk profiles are worlds apart.

A flight school is a hub of constant activity, where minor incidents are a statistical probability, not a remote "what if." You're dealing with a blend of expensive assets (your aircraft), inexperienced students, professional instructors, and public safety all at once. Every training flight introduces a level of risk that a private pilot flying for leisure simply doesn't face. This is precisely why specialized flight school insurance exists—it’s built from the ground up to address this complex, high-traffic reality.

The Higher-Risk Training Environment

Let's break it down. Your training aircraft will see far more takeoffs and landings than almost any privately owned plane. These are, statistically, the most critical phases of any flight. Now, add a student pilot at the controls, and the potential for a hard landing, a runway excursion, or worse, climbs significantly. Your insurance policy needs to reflect this intense operational tempo and the steep learning curve of your students.

Your insurance isn't just a piece of paper; it's your business continuity plan. It accepts that while you aim for a perfect safety record, you have to be ready for the financial fallout when things don't go perfectly. A single major incident without the right coverage could ground your school for good.

The risks don't disappear when the engines are off, either. Your assets are vulnerable on the ground, too. We’re talking about "hangar rash" from shuffling planes around, accidental damage during maintenance, or even events like theft or fire. A robust flight school policy includes specific ground risk coverage that a basic plan might completely miss.

And it’s not just the planes. Many schools now rely on sophisticated flight simulators. It's smart to look into how equipment breakdown insurance can protect these expensive and vital training tools.

A well-crafted flight school insurance plan anticipates these scenarios, creating a protective layer around every part of your business. It covers liabilities stemming from instruction, student errors, and your physical assets, freeing you up to focus on what you do best: shaping the next generation of pilots.

At-a-Glance View of Flight School Insurance Policies

To get a clearer picture, let's quickly summarize the key insurance types that form a comprehensive protection plan for any flight training operation. These coverages work together to create a solid foundation of security for your school.

| Coverage Type | What It Safeguards | Why It's Non-Negotiable for Your School |

|---|---|---|

| Aircraft Hull Insurance | Your physical aircraft fleet from damage or loss. | A single damaged aircraft can halt training and revenue. This helps you repair or replace it quickly. |

| Aviation Liability Insurance | Bodily injury and property damage to third parties. | Protects your business from catastrophic lawsuits if an incident harms people or property on the ground. |

| Instructor & Student Liability | Legal protection for instructors and students named in a lawsuit. | Gives instructors and students peace of mind, knowing they have coverage if an accident occurs during training. |

| Premises Liability | "Slip-and-fall" incidents at your facility (hangar, office). | Accidents can happen anywhere, not just in the air. This covers non-aviation-related injuries on your property. |

| Non-Owned Aircraft Insurance | Aircraft you rent or borrow for training purposes. | Essential if you lease aircraft to expand your fleet, ensuring you're covered even for planes you don't own. |

Having these policies in place isn't just about mitigating risk; it’s about building a resilient business that can withstand the unexpected challenges inherent in aviation.

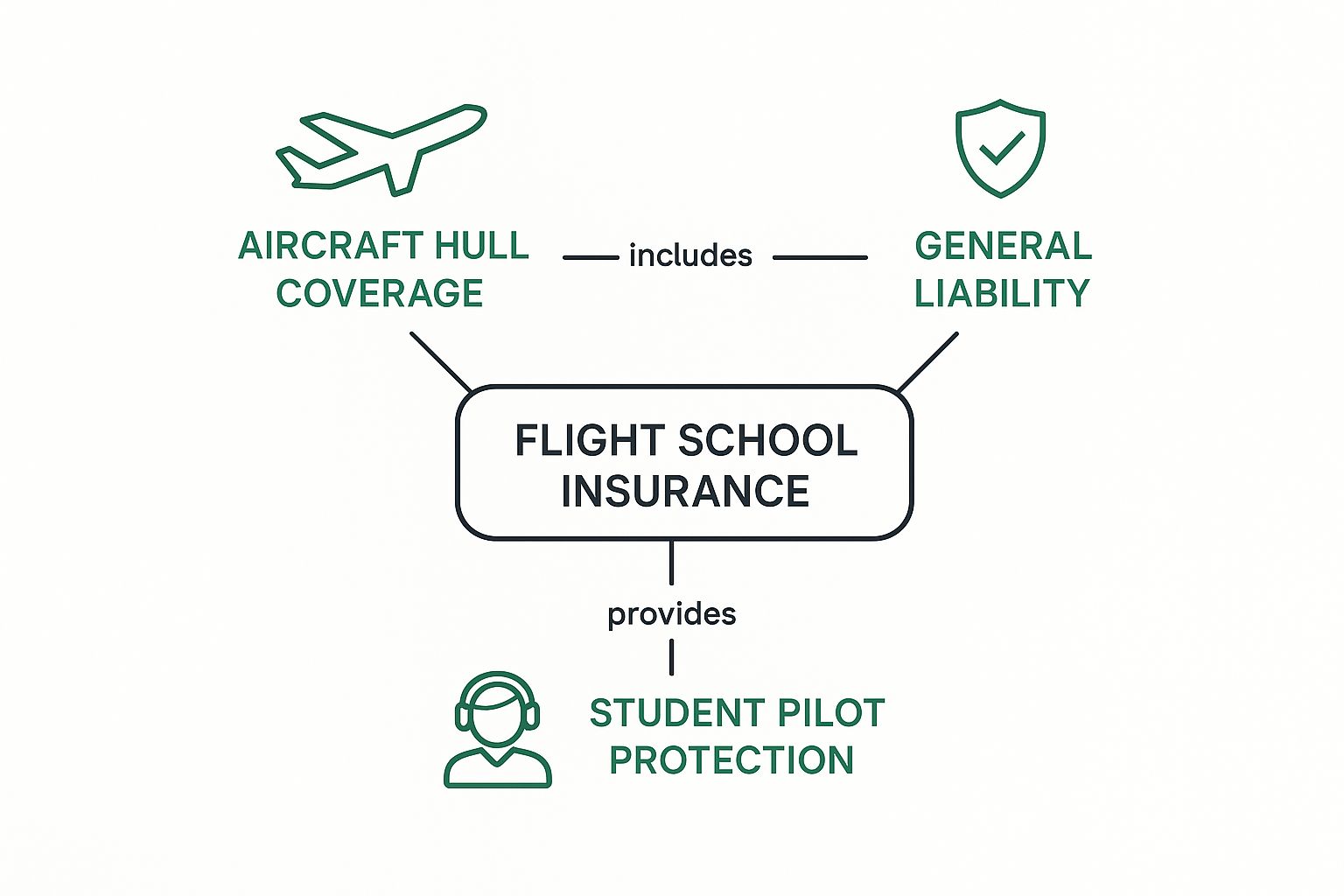

Alright, let's break down what's actually in your flight school insurance policy. It's easy to see it as one big, complicated document, but it's more helpful to think of it like a suit of armor. Each piece—the helmet, the breastplate, the gauntlets—protects a different, vital part of your operation.

Knowing how these individual pieces work together is the secret to building a truly resilient business. We’ll go through the core coverages every flight school needs, using real-world examples to show you exactly why you can't operate without them. This isn't just about money; it's about making sure your school can weather a storm and get back to its mission.

This infographic gives you a great visual of how everything fits together.

As you can see, solid protection is a mix of covering your physical assets (the planes), your operational liability (the "what ifs"), and the people at the center of it all.

Aircraft Hull Insurance: The Body Armor for Your Fleet

This one is the most straightforward, but don't underestimate its importance. Aircraft Hull Insurance is what pays to repair or replace the physical airplane if it gets damaged or is a total loss. Simple as that.

Most people immediately think of a flight-related accident—a gear-up landing or a runway excursion. And yes, it absolutely covers that. But from my experience, a huge number of claims come from incidents that happen right on the ground.

Think about these everyday risks:

- Hangar Rash: It happens all the time. A student is taxiing a little too fast and scrapes a wingtip on another plane.

- Maintenance Mishaps: A mechanic drops a heavy wrench, putting a nasty dent in the fuselage.

- Weather: A surprise hailstorm rolls through overnight and pounds the aircraft you left tied down on the ramp.

- Facility Failures: A hangar door sensor fails, and the door comes down right on the tail of an airplane.

Without good hull insurance, any of these scenarios could easily take an aircraft out of commission for weeks and stick you with a repair bill for thousands of dollars. That's a direct hit to your revenue and your training schedule.

Aviation Liability Insurance: Your Shield Against the World

If hull insurance protects your stuff, Aviation Liability Insurance protects your business from claims brought by other people. This is, without a doubt, the most critical part of your policy. Liability lawsuits can climb into the millions faster than you can imagine.

This coverage is usually split into a couple of key areas:

Passenger Liability: This kicks in if someone on a flight—like a prospective student on a discovery flight—is injured or worse. It pays for your legal defense and any judgment or settlement that comes from it.

Third-Party Liability: This covers injury or property damage to people and things on the ground. Let's say a student has an engine failure on final and has to put the plane down in a farmer's field. If they damage crops or take out a fence, this is the coverage that pays for it.

Key Insight: Liability coverage is the firewall between an accident and a lawsuit that could shutter your business for good. It's designed to absorb the crushing financial weight of a legal battle so you can focus on the operational and human side of the crisis.

The need for this protection is only growing. The global aviation insurance market was recently valued at USD 4.49 billion and is projected to expand, driven by more and more flying. Consider that US airlines carried 853 million passengers in a single recent year—a 30% increase from the year before. More activity means more risk exposure for everyone, including flight schools. You can get a deeper look at these trends in this detailed aviation insurance report.

CFI and Student Pilot Protection

A great insurance program also understands the unique risks faced by the people doing the training and learning.

Certified Flight Instructor (CFI) Liability is a non-negotiable endorsement. If an accident leads to a lawsuit that claims negligent or improper training was the cause, this coverage defends both the school and the instructor. Without it, your CFIs' personal assets are exposed, which makes it incredibly difficult to hire and keep the best instructors.

Non-Owned Aircraft Insurance adds another crucial layer of protection, especially for students flying solo in your aircraft. This is often misunderstood. While your school's policy covers the plane itself, a non-owned policy (which students often purchase as "renter's insurance") can cover your main policy's deductible and give liability protection directly to the student. In fact, many flight schools now require students to carry their own non-owned policy. It creates a much stronger, multi-layered defense against risk for everyone involved.

Understanding What Drives Your Insurance Costs

When an insurance quote for your flight school lands on your desk, the final premium can feel a bit arbitrary. But rest assured, insurers aren't just pulling numbers out of thin air. The process is a lot like a pilot’s pre-flight check—a detailed risk assessment where every factor is weighed carefully. Getting a handle on these cost drivers is the first real step toward managing them.

Some of these factors you can control directly, while others are simply the reality of the market. Let's break down what underwriters are really looking at when they price your policy.

Your Fleet and Its Mission

No surprise here: the single biggest factor driving your insurance cost is the aircraft you fly. It’s pretty simple when you think about it. Insuring a brand-new, high-performance aircraft with a glass cockpit is a completely different ballgame than insuring a trusty old Cessna 172. Every plane has its own risk profile.

Here’s what insurers zoom in on when evaluating your fleet:

- Aircraft Type and Value: The higher the agreed value of an aircraft, the more you'll pay for hull insurance. A shiny new Cirrus SR22 just costs more to fix or replace than a 40-year-old Piper Cherokee.

- Engine Type: Turbine-powered planes almost always cost more to insure than piston-engine aircraft. Their complex systems and expensive parts mean higher potential repair bills.

- Advanced Features: Does the plane have retractable gear? A high-performance engine? Complex avionics? In a training environment, these features add layers of risk, and that’s reflected in the premium.

- Fleet Size: While more planes mean more assets to cover, a larger, well-managed fleet can sometimes give you leverage for better per-aircraft rates, especially if you have a strong safety program in place.

What you do with your aircraft matters just as much. A plane used only for primary private pilot training will be priced very differently from one used for advanced aerobatic maneuvers or multi-engine instruction. The perceived risk of those activities is worlds apart. The same logic applies to your ground vehicles; you can see the parallels by exploring how business auto insurance costs are determined.

The Human Element: Your Instructors and Students

Beyond the hardware, underwriters put a massive emphasis on the people in the cockpit. Your team of Certified Flight Instructors (CFIs) is one of your biggest assets—and a huge factor in your insurance profile.

A school staffed by seasoned CFIs with thousands of hours and spotless safety records is a much lower risk than one that leans on newly minted instructors. Insurers will dig into the total flight hours, experience in specific aircraft types, and any incident history for every pilot on your payroll. Bottom line: investing in experienced instructors is a direct investment in a lower-risk operation.

Your safety culture, demonstrated through proactive risk management and continuous training, is your most persuasive argument to an underwriter. It proves you are a partner in minimizing risk, not just a customer buying a policy.

This focus naturally extends to your students. The kind of training you provide—from private pilot certificates all the way up to airline transport pilot programs—shapes your student risk profile. A school with tough pre-solo screening and rigorous progress checks shows underwriters a commitment to safety that they absolutely value.

Market Conditions and Your School’s History

Finally, the big-picture market forces and your school's unique track record complete the pricing puzzle. Nothing speaks louder than your claims history. A school with a pattern of frequent claims, even small ones, will face steeper premiums than a school with a clean slate. It’s the most direct evidence of how safe your operation really is.

The broader aviation insurance market also plays a role. The mid-2020s have seen a fairly competitive market with a good amount of capacity, which helps keep a lid on pricing. But that's balanced by some serious headwinds, like soaring aircraft repair costs, a shortage of qualified mechanics, and ongoing supply chain issues for parts. These trends drive up claim costs for insurers, forcing them to be extra cautious when underwriting flight schools.

By actively managing your fleet, investing in top-tier instructors, and maintaining a stellar safety record, you are building the strongest possible case for the best flight school insurance rates you can get.

Choosing the Right Insurance Partner and Policy

Picking out insurance for your flight school isn’t like grabbing a new policy for your car online. You're not just ticking boxes and buying a product; you’re bringing on a business partner who will be your first call when things go sideways. The single most important decision you can make is to work with an insurance broker who lives and breathes aviation.

A generalist broker who can't tell a yoke from a rudder simply won't grasp the unique risks you manage every single day.

Think of it this way: you wouldn't trust a boat mechanic to overhaul your aircraft's engine. The same logic applies here. An aviation insurance specialist speaks the language of underwriters, knows the fine print in aviation policies backward and forward, and has built relationships with the key carriers who actually write flight school coverage. That expertise is your biggest advantage in getting a policy that truly has your back.

Vetting Your Aviation Insurance Broker

Before you even glance at a premium quote, you need to vet the person who's bringing it to you. A great broker is more than a salesperson; they are your advocate and risk advisor. When you're interviewing potential brokers, don't hold back. The survival of your business could literally hinge on their competence.

Here are some critical questions to ask:

- How many flight schools do you currently insure? You're looking for someone with a deep bench of clients just like you, not a broker for whom you’d be a learning experience.

- Can you walk me through a recent flight school claim you handled? Their answer will tell you everything about their real-world experience and whether they truly understand the process from the initial incident to a final resolution.

- Which aviation insurance carriers do you have appointments with? A well-connected broker has access to multiple A-rated underwriters, which means they can shop the market properly to find the best terms and price for your specific operation.

- How will you help us with risk management beyond just selling a policy? The best brokers are partners in safety. They should offer valuable insights on your training programs, safety management systems, and other strategies to make you a more attractive risk to insurers.

Choosing the right expert is the foundation of a solid insurance strategy. A great broker won't just find you a policy—they’ll help you become a better, safer, and more insurable flight school for the long haul.

A cheap policy from a generalist broker is often the most expensive one you can buy. The real cost is revealed when you file a claim and discover the gaps in coverage that an aviation specialist would have identified from the start.

Looking Beyond the Premium

Once you have quotes from a qualified broker, it’s all too easy to let your eyes jump straight to the lowest price. That's a huge mistake. The premium is just one piece of the puzzle. You have to learn how to dissect the policy to understand what you’re actually getting for your money.

Focus on these key areas:

- Coverage Limits: Are the liability limits actually enough for a worst-case scenario? A $1,000,000 limit might sound like a lot, but that can get eaten up frighteningly fast in a serious incident.

- Deductibles: Look closely at the hull deductibles for both in-motion and not-in-motion events. A tempting low premium might be hiding a painfully high deductible you'll have to shell out for any minor hangar rash claim.

- Exclusions: This is where many flight schools get burned. Read the exclusions section with a fine-tooth comb. Does the policy exclude coverage for certain types of instruction you offer, like aerobatics or tailwheel training?

This process can feel overwhelming, especially if it leads you to realize your current provider isn't the right fit. If you're in that spot, it’s critical to handle the transition correctly. To help, we’ve put together a simple guide on how to switch insurance providers without creating dangerous gaps in your coverage.

Implementing Smart Risk Management to Lower Premiums

When it comes to your flight school insurance costs, you’re not just a passenger. You’re in the pilot's seat. While you can't control the broader insurance market, you absolutely can control how you run your school. This is where you have real power to make a difference—not just by creating a safer environment, but by proving to insurers that you're a low-risk, professional operation worth insuring at a better rate.

Think of your risk management program as a direct conversation with the underwriter. Every safety checklist you enforce, every training procedure you standardize, it all sends a powerful message. You're telling them you are serious about stopping incidents before they ever get a chance to happen. This proactive mindset is your single best tool for earning better coverage and lower premiums year after year.

Build a Living Safety Management System

A Safety Management System (SMS) can't just be a thick binder gathering dust on a shelf. For it to mean anything, it has to be a living, breathing part of your school's culture. An SMS is your formal, documented game plan for safety—outlining who's accountable, what the policies are, and how you execute them.

A truly robust SMS includes:

- Proactive Hazard Identification: Creating simple, clear ways for instructors and students to report potential safety issues without any fear of getting in trouble.

- Formal Risk Assessment: Having a set process to analyze any reported hazards, figure out how serious they could be, and prioritize what needs to be fixed first.

- Continuous Monitoring: Regularly looking at your safety data to spot trends, see if your initiatives are working, and find new ways to improve.

When an underwriter sees a well-documented and actively used SMS, they don't just see a school that's compliant. They see a business that's disciplined, professional, and genuinely committed to minimizing risk.

A truly effective Safety Management System transforms your school's culture from being reactive to proactive. It shifts the focus from asking "What happened?" after an incident to asking "What could happen?" before one ever occurs, making you a much more attractive risk for insurers.

The aerospace insurance market, which covers flight schools, was recently valued at USD 896.5 million and is expected to hit USD 1.16 billion within the next decade. This isn't surprising, given the growing demand for new pilots. Insurers in this space are acutely aware of the risks unique to flight training, and they actively look for schools that demonstrate superior risk management. You can dive deeper into these aerospace insurance market dynamics to see how they shape coverage for training operations like yours.

Invest in Your Instructors and Technology

Your Certified Flight Instructors (CFIs) are on the front lines of your risk management every single day. Pouring resources into their continued development is a direct investment in your school's safety and insurability.

CFI Standardization Programs: Holding regular, documented meetings to ensure all your instructors are teaching maneuvers and procedures the exact same way is critical. This consistency cuts down on student confusion and, more importantly, helps prevent the formation of bad habits—a major cause of training incidents.

Advanced Training Tools: Modern technology isn't just a "nice-to-have"; it's a powerful way to de-risk the training environment.

- Flight Simulators: High-fidelity simulators are the perfect place for students to practice emergency procedures and complex maneuvers with zero actual risk. If you document how you use simulators for specific training goals, you're showing insurers you’re using every tool at your disposal to build safer pilots.

- Flight Data Monitoring (FDM): Installing FDM systems in your fleet gives you objective data on every single flight. It lets you spot trends like consistently hard landings or overly aggressive maneuvering, so you can step in with targeted training before a small issue becomes a big one. These proactive steps can also help manage other operational risks. For more on that, exploring the business interruption insurance cost can offer valuable insight into protecting your school's overall financial health.

By putting these smart strategies into practice, you stop being a passive insurance buyer. You start actively shaping the terms of your own coverage, building a powerful case that your school is a preferred partner worthy of the best rates the market has to offer.

Answering Your Top Insurance Questions

Once you have the big picture of your policies, the real-world questions start to pop up. These are the day-to-day scenarios that can leave flight school owners scratching their heads. Let's walk through some of the most common questions we get from clients to clear up these critical details.

Getting these specifics right is what makes your insurance work for you when it counts, turning abstract policy language into practical protection.

Does My Policy Cover Students Flying Solo?

The short answer is yes, but it comes with a big "if." The key is a clause in your policy called the "Open Pilot Warranty." Think of this as the rulebook that spells out the bare-minimum qualifications a pilot needs to be covered when flying your aircraft. It will have specific requirements for student pilots going on their first solo flights.

For extra peace of mind, many schools now require students to get their own non-owned aircraft insurance (often called renter's insurance). This is a smart move. It creates another layer of protection that can help cover your policy’s deductible and provides the student with their own liability coverage. It's always best to talk this through with your broker to see how it fits your specific operation.

What If a CFI Is Sued for Improper Training?

This is exactly why Certified Flight Instructor (CFI) Liability coverage exists. If an incident happens and a lawsuit claims that shoddy instruction was a factor, this is the part of your policy that kicks in. It provides the money to defend both the flight school and the individual instructor named in the suit.

Without this specific protection, a single lawsuit could jeopardize a CFI’s personal assets and put the entire financial future of your school on the line. We consider this an absolutely non-negotiable part of any flight school insurance program.

This coverage is all about protecting the people who are the heart of your business.

How Does Insurance Work for a Mixed Fleet?

Don't worry, insurers see mixed fleets all the time. Your policy will simply list out each aircraft individually and assign it a specific "agreed value." This is the number that dictates the payout you'd receive if the hull is a total loss.

The premium is then built on a plane-by-plane basis, looking at things like:

- Aircraft Type: A trusty Cessna 172 is going to be priced very differently from a complex Piper Seminole.

- Aircraft Age & Features: A brand-new plane with a glass cockpit presents a different risk profile than an older aircraft with classic steam gauges.

- Intended Use: The rate will change depending on whether a plane is used for primary training, advanced multi-engine work, or even aerobatics.

This approach gives you customized protection for each asset you own, all bundled neatly into one policy.

Is Damage During Ground Maintenance Covered?

Yes, this is a classic example of what the "ground risk" part of your Aircraft Hull Insurance is for. It covers your planes from non-flight-related damage—basically, any harm that comes to them when they aren't moving under their own power. We're talking about things like hangar rash, a mechanic dropping a heavy tool on a wing, or damage from a windstorm while tied down.

It’s a good idea to check your policy for the difference between "ground risk not in motion" and "ground risk in motion" (which covers taxiing), as the deductibles can be different for each. Understanding these finer points is just as important as knowing the fundamentals of general business insurance, which form the bedrock of any commercial policy.

Navigating the complexities of flight school insurance requires a partner who understands the unique risks of aviation. The experts at Wexford Insurance Solutions specialize in finding the right coverage to protect your fleet, your instructors, and your business. Contact us today to ensure your operation is fully protected.

A Guide to Equipment Breakdown InsuranceCyber Security Risk Management | Essential Strategies & Tips

A Guide to Equipment Breakdown InsuranceCyber Security Risk Management | Essential Strategies & Tips