For generations, the insurance industry ran on a simple, time-tested formula: look at past data, group people into broad categories, and set prices based on historical averages. It was a reactive model, built on paying out claims after something had already gone wrong. But that old playbook is being completely rewritten.

Today, we're seeing a fundamental shift. Insurance is moving away from relying on static, historical information and toward a dynamic, predictive model powered by a constant stream of data.

A New Blueprint for Modern Insurance

Think of it like this: a traditional insurer was like a captain navigating with an old paper map. It showed where the rocks and shoals used to be, but it couldn't account for a sudden storm or a changing tide. A modern, data-driven insurer, on the other hand, is using a live, sophisticated GPS. It doesn't just show the map; it shows real-time weather, sea conditions, and other vessels, allowing the captain to anticipate problems and chart a much safer, more efficient course.

That "GPS" is data analytics. It's the engine that processes massive volumes of information—what we call big data—to help insurance companies see around the corner. This approach isn't just a fancy add-on anymore; it's becoming the core of how smart insurers operate, compete, and grow. It's about building an industry that's more intelligent, responsive, and ultimately, more resilient.

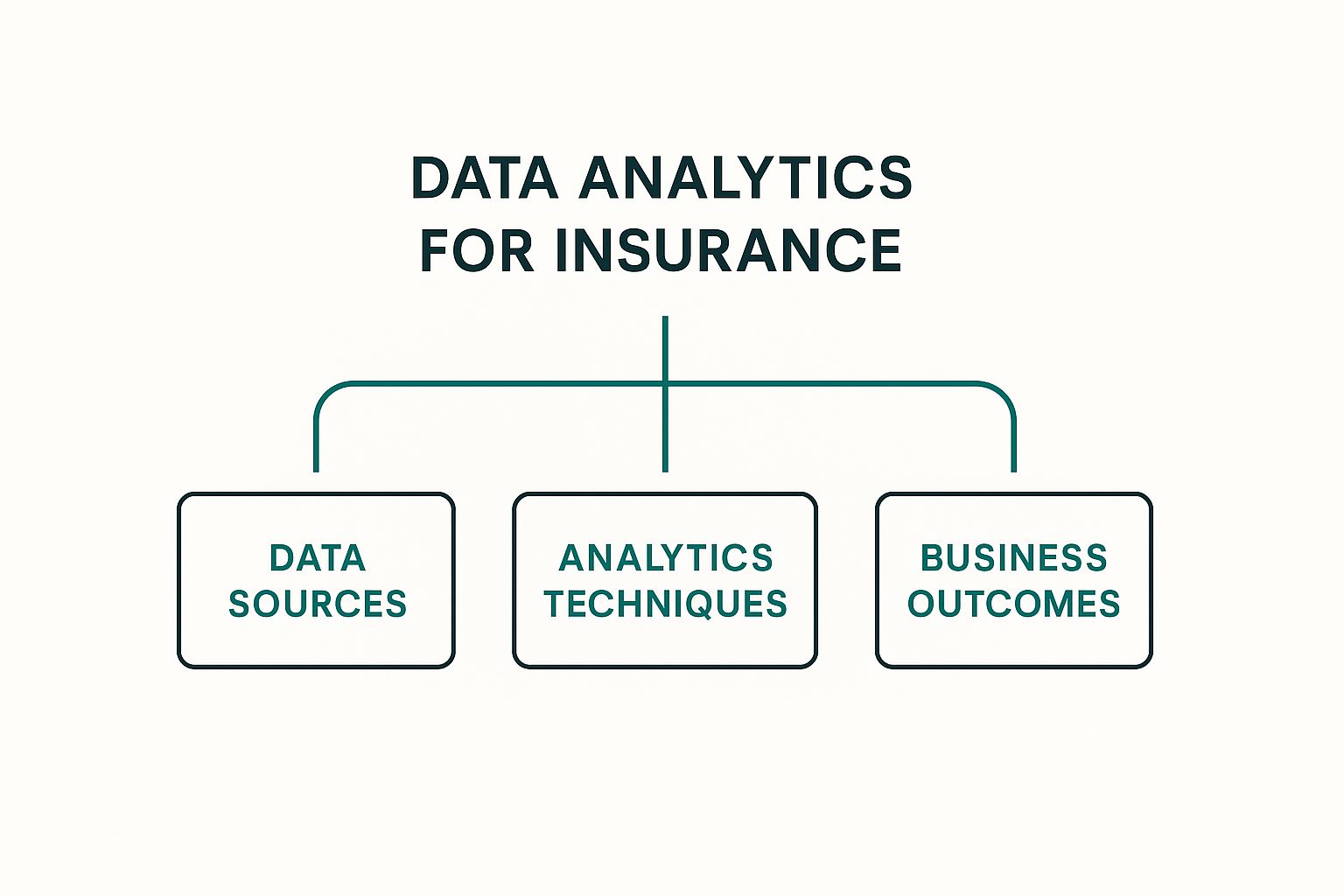

From Raw Data to Real Insight

At its core, data analytics is all about turning a sea of raw information into clear, actionable intelligence. The process involves pulling data from all sorts of places, running sophisticated analyses to spot patterns and trends, and then using those discoveries to make better business decisions.

This is what that process looks like in practice, broken down into its essential parts.

As the diagram shows, you need the right blend of data sources, analytical methods, and business goals. When these elements come together, the result is tangible: better profitability, happier customers, and a stronger bottom line.

To truly grasp the change, it helps to see the old and new ways side-by-side.

Traditional vs. Data-Driven Insurance Practices

This table shows just how stark the contrast is between the insurance of the past and the data-powered insurance of today.

| Area of Operation | Traditional Approach (The Past) | Data-Driven Approach (The Future) |

|---|---|---|

| Pricing | Based on broad demographic groups and historical loss data. | Based on individual behavior, real-time risk, and predictive models. |

| Underwriting | Manual review of applications, relying on generalized risk pools. | Automated, data-rich analysis of individual risk factors for precision. |

| Claims | Slow, manual processing involving extensive paperwork and investigation. | Automated, AI-driven verification for faster, more accurate payouts. |

| Risk Management | Reactive; identifying and paying for losses after they occur. | Proactive; using data to predict and prevent losses before they happen. |

| Customer Interaction | Limited, often only at renewal or time of claim. | Continuous and personalized, offering risk-reduction tips and tailored advice. |

The evolution is clear. We're moving from a one-size-fits-all model to one that is highly personalized and proactive, creating value for both the insurer and the customer.

Why This Shift Is Happening Now

So, what's driving this massive change? A few key things. First, the explosion of data is undeniable. Information from smart home sensors, vehicle telematics, wearables, and even our online activity gives insurers a remarkably detailed picture of risk that was unimaginable just a decade ago.

The financial incentive is also a huge catalyst. The global insurance analytics market was valued at $13.84 billion in 2023 and is expected to grow at an impressive 14.7% compound annual growth rate through 2030, according to Grandview Research. That kind of money shows this isn't a trend; it's a fundamental industry-wide investment.

This transformation isn’t just for the big players, either. It helps everyone, from large corporations to small businesses, get the right protection. For example, analytics can more accurately pinpoint a company’s unique risks, helping determine if they need specialized coverage. You can see how this applies by learning what a business owners policy includes.

At its heart, data analytics for insurance is about switching from a reactive posture to a proactive one. Instead of just paying for losses after they happen, insurers can now help prevent them.

This new blueprint creates a more dynamic and collaborative relationship between insurers and their customers. It opens the door for:

- Fairer Pricing: Your premium can be based on your actual driving habits or how well you maintain your property, not just your zip code or age.

- Faster Service: Claims can be verified and paid out in a fraction of the time by automating the busywork and flagging exceptions for human review.

- Enhanced Risk Management: Insurers can spot a potential water leak from a smart sensor and alert a homeowner before it becomes a catastrophic flood.

How Data Analytics Gives Underwriters Superpowers

Underwriting has always been the heart of the insurance business. It’s the critical process of figuring out just how risky a potential client is. For decades, this was a manual job that relied almost entirely on an underwriter's gut feeling and a few static data points—age, location, and maybe a few other general details. It felt more like an art than a science, often resulting in broad, imprecise risk categories.

Today, data analytics is completely reshaping that tradition. It injects hard science into the art of underwriting. Instead of just looking at who someone is on paper, modern underwriting can analyze what they do. We've moved from static snapshots to a dynamic, live stream of information.

Beyond Basic Demographics

The real magic here is the sheer depth and variety of data we can now access. Machine learning models can sift through thousands of variables at once, painting a multi-dimensional picture of risk that was simply unimaginable a generation ago. We're talking about much more than the basics.

This data-rich approach makes granular pricing possible. Insurers are finally able to move away from one-size-fits-all premiums and toward rates that truly reflect an individual's or a business's specific risk profile.

By looking at diverse data sources, predictive models can generate a highly precise risk score. This isn’t just about fairer pricing for customers; it creates a more stable and profitable portfolio for the insurer.

The market is certainly betting on this shift. The insurance analytics market was valued at around $11.47 billion and is expected to grow at a compound annual rate of 15.90% through 2033. This explosion is fueled by the tidal wave of new data, which demands sophisticated analytics to make sense of it all. You can dive deeper into the trends driving this growth in the full market report.

Uncovering Hidden Risks and Opportunities

Let's look at a real-world example. Imagine two businesses applying for workers' compensation insurance. On paper, they look like twins: same industry, similar revenue, and the same number of employees. In the old days, they’d probably get nearly identical quotes.

But data analytics tells a much richer story.

- Business A: A closer look reveals a pattern of frequent but minor safety incidents, a high employee turnover rate, and a location in an area prone to severe weather that could disrupt operations.

- Business B: The data shows a stellar safety record, documented investment in employee training programs, and proactive maintenance to protect their property from weather damage.

With this level of detail, it’s clear that Business B is a much lower risk. Predictive analytics brings these hidden factors to light, allowing the insurer to offer a more competitive premium to Business B while adjusting the rate for Business A to accurately cover its higher risk. This kind of precision is especially vital for complex policies; understanding workers' comp experience mods and how they affect your premium demonstrates how directly data can impact the bottom line.

Empowering Human Expertise, Not Replacing It

This evolution doesn't make human underwriters obsolete. Far from it. It actually elevates their role. By automating the grunt work of analyzing routine applications, data analytics frees up seasoned professionals to tackle what they do best: manage complex, high-value, or unusual cases that require human judgment and creative thinking.

This blend of machine efficiency and human expertise is incredibly powerful. The benefits are impossible to ignore:

- Increased Efficiency: Automating routine applications slashes underwriting turnaround times.

- Greater Accuracy: Models process massive datasets without human bias, leading to more consistent and precise risk assessments.

- Enhanced Profitability: Fairer pricing means insurers avoid accidentally taking on underpriced risks, which strengthens the entire insurance portfolio.

Ultimately, giving underwriters predictive power creates a win-win. Low-risk customers get the better rates they deserve, and insurers build more sustainable businesses by making smarter, data-backed decisions.

Building a Smarter and Faster Claims Process

For an insurer, the claims process is where the rubber meets the road. It’s the moment of truth when a promise made on paper becomes a real-world action. For the customer, it’s often a period of high stress and uncertainty. Traditionally, this has been a slow, paper-heavy ordeal, but modern data analytics is completely reshaping it, making it faster, more accurate, and more secure for everyone involved.

Think of the old claims journey as a long, winding country road with frequent, manual toll booths. Data analytics effectively builds a multi-lane highway, creating an express lane for straightforward claims while carefully guiding any suspicious activity to a dedicated inspection lane. This isn't just about efficiency; it's about delivering a far better customer experience when it matters most.

Fast-Tracking Claims with Intelligent Automation

One of the biggest game-changers here is Natural Language Processing (NLP), a type of AI that can read and understand human language. The moment a claim is submitted, NLP algorithms can scan adjuster notes, customer emails, and police reports in an instant. The system immediately figures out the type of claim, gauges its complexity, and checks if all the necessary information is there.

Simple, low-risk claims—say, a cracked windshield with clear photos and a receipt—can be put on a fast track for immediate approval and payment. This “touchless claims” approach can settle a case in a matter of hours, not weeks. This speed is a huge relief for customers and, just as importantly, it frees up your experienced human adjusters to focus their brainpower on the complex, sensitive cases that truly need their expertise.

The impact is easy to see:

- Speed: Simple claims get paid in a fraction of the time.

- Accuracy: Automation cuts down on the human errors that can creep into data entry and routine checks.

- Efficiency: Your best people are focused on high-value work, not administrative tasks.

Uncovering Fraud with Predictive Power

Speed is fantastic, but so is security. Insurance fraud is a massive headache for the industry, costing billions every year and ultimately pushing up premiums for honest policyholders. Data analytics gives insurers a powerful new tool, moving fraud detection from a reactive, after-the-fact process to a proactive defense.

Predictive models sift through mountains of data in real time, looking for strange patterns and red flags that a person would never catch. These systems work like a digital detective, connecting seemingly random dots to expose suspicious activity before a fraudulent payout is made.

A data-driven system can identify and flag suspicious activity with incredible precision, preventing major losses before they happen. This protects the insurer’s bottom line and ensures that honest customers aren't left subsidizing crime.

Here’s a real-world example: A brand-new medical clinic starts submitting a flurry of workers' compensation claims within its first few months. Looked at one by one, each claim might seem perfectly fine to a human reviewer. An analytics system, however, can instantly cross-reference data points. It might flag that the same clinic, doctor, and lawyer have appeared together on an unusually high number of claims filed with different insurers in a very short time. That’s a classic sign of a coordinated fraud ring, triggering an investigation that would have otherwise been missed.

This kind of deep insight is vital across all types of coverage. To get a better handle on the fundamental policies that data analytics helps protect, check out our guide on business insurance basics, which breaks down the core coverages that benefit most from these advanced fraud detection tools.

A Dual Victory for Insurers and Customers

In the end, integrating data analytics into the claims process creates a clear win-win. Insurers operate more efficiently, slash their operational costs, and protect themselves from serious financial losses.

Even more importantly, customers get a fundamentally better, more human experience. Their legitimate claims are paid quickly and with less hassle, building genuine trust and loyalty. By systematically weeding out fraud, insurers can also keep premiums more stable and competitive for everyone. This blend of speed, security, and service is what a modern, customer-first claims experience looks like.

Optimizing Pricing Through Personalization

The days of one-size-fits-all insurance policies are numbered. Today's customers expect more—they want pricing that feels fair and transparent, reflecting their unique behaviors and risks, not just lumping them into broad, outdated categories. Hyper-personalization, powered by data analytics for insurance, is no longer a futuristic concept; it's a critical competitive advantage.

This shift fundamentally changes the relationship between an insurer and a policyholder. Insurance becomes less of a static, set-it-and-forget-it product and more of a dynamic service. A policy can now adapt to a customer's real-world actions, creating a powerful, positive feedback loop. When people know their good habits can directly lower their costs, they're incentivized to make safer choices. It’s a win-win.

The industry is pouring money into this evolution for a reason. The global insurance analytics market is on track to hit $32.92 billion by 2029, growing at a remarkable 18.4% annually. This isn't just hype; it's a direct response to intense market competition and customer demand for truly customized products. For a deeper dive into these numbers, check out this comprehensive market analysis.

The Rise of Usage-Based Insurance

The most well-known example of this trend in action is Usage-Based Insurance (UBI), which has completely reshaped auto coverage. It’s a simple, powerful idea: pay how you drive. Instead of relying solely on traditional metrics like your age and driving record, UBI uses telematics data to understand your actual habits on the road.

A small device in your car or a smartphone app gathers key information:

- Driving style: How often do you accelerate or brake sharply?

- Speed habits: Are you consistently following posted speed limits?

- Driving times: Do you frequently drive late at night when risks are higher?

- Total distance: What’s your annual mileage?

This data feeds into an analytics model that creates a personalized risk score. Safe, careful drivers see their premiums go down because their behavior proves they're less likely to file a claim. It’s a direct, tangible reward for responsible driving.

Usage-Based Insurance transforms pricing from a generalized estimate into a fair reflection of individual behavior. It empowers customers by giving them direct control over their insurance costs.

And this model isn't just for cars anymore. The same core principles are being applied across the industry, opening up exciting new avenues for personalization.

Expanding Personalization into Health and Home

This data-driven approach is quickly moving into other lines of insurance, thanks in large part to the explosion of connected devices we all use.

- Health Insurance: Wearable fitness trackers provide a stream of data on physical activity, heart rate, and sleep. Insurers can use this to offer wellness rewards or lower premiums to people who consistently meet step goals or maintain a healthy resting heart rate.

- Home Insurance: Smart home technology, like leak detectors, smoke alarms, and security systems, offers real-time monitoring. A homeowner who installs these devices is actively reducing their risk of fire, water damage, or theft, and their premiums can reflect that proactive investment.

- Valuable Items: Even highly specialized coverage gets a boost from better data. Insuring high-value assets requires a precise understanding of risk. For instance, a detailed jewelry appraisal for insurance provides the specific data needed to ensure the coverage perfectly matches the item's value and unique risk factors.

These dynamic pricing models, all fueled by real-time analytics, create a system that adjusts to a customer's life. This doesn't just deliver fairer costs; it helps insurers build more sustainable, profitable businesses by aligning their success with the well-being and safety of their customers.

Putting Your Data-Driven Strategy into Action

Shifting to a data-first model isn't something that happens overnight. It's a fundamental change, but the payoff is more than worth the effort. Think of it less like flipping a switch and more like building a new foundation, one solid piece at a time. A successful strategy really comes down to three things: modern technology, skilled people, and a company culture that genuinely trusts data.

The first practical step is often moving away from outdated legacy systems. Imagine your old data infrastructure is a library with books chaotically piled on the floor—finding anything is a slow, frustrating exercise. A modern data architecture, usually built in the cloud, is like a perfectly organized digital library with a powerful search engine. It puts critical insights right at the fingertips of everyone who needs them.

This modern foundation is essential for effective data analytics for insurance. It creates a single source of truth, making sure your underwriting, claims, and pricing teams are all on the same page, working from the same high-quality information.

Building Your Analytics Capability

Once you have the right technology in place, the focus turns to the people who will actually use it. This means bringing in new talent while also training your existing team. You’ll need data scientists and analysts who can dig into the numbers, build predictive models, and explain what it all means in clear business terms.

But it’s just as important to build data literacy across the entire company. Your underwriters and claims adjusters don’t need to become expert coders, but they do need to get comfortable using data to inform their everyday decisions.

A successful data analytics program isn't just about hiring a few experts. It's about empowering your entire workforce to think critically with data and move from relying on "gut feelings" to trusting "data-backed evidence."

This cultural shift is often the biggest hurdle. It takes strong leadership, consistent communication, and a real commitment to change that starts at the very top.

A Practical Roadmap for Implementation

Trying to overhaul the entire company at once is a recipe for disaster. It’s far smarter to start small, prove the value, and build momentum from there. A phased rollout minimizes risk and sets you up for long-term success.

Here’s a step-by-step framework to guide your journey:

-

Start with a Pilot Project: Pick one specific area where data analytics can deliver a quick, measurable win. A great example is analyzing historical data to fine-tune risk assessment for a particular line of business, like workers' compensation. Proving ROI here makes it much easier to get buy-in for bigger initiatives. For instance, understanding how factors like workers' comp experience mods affect your premium shows exactly how targeted analysis can lead to direct financial benefits.

-

Establish Strong Data Governance: Before you go big, you need clear rules of the road. Data governance is the framework that ensures your data is accurate, consistent, and secure. This means creating clear policies for who can access what, how quality is checked, and—most critically—how it's all used ethically.

-

Prioritize Ethical Considerations: Using customer data is a massive responsibility. Your strategy must include a rock-solid plan for protecting privacy and ensuring fairness. Transparency is everything—customers should understand how their data helps them, whether through better pricing or faster service. This builds trust, and in insurance, trust is the most valuable asset you have.

The Future of Insurance Analytics

As impressive as today's tools are, we're really just scratching the surface of what data analytics for insurance can do. The next wave of innovation is already taking shape, and it points toward an industry that's far more proactive, automated, and genuinely woven into customers' lives. We're moving beyond simply predicting what might happen to actively influencing better outcomes for everyone.

A huge part of this shift is the emergence of Generative AI. You can think of it as a creative collaborator for data scientists. In situations where real-world data is limited or protected by strict privacy rules, Generative AI can step in to create high-quality synthetic data. This gives insurers a much richer and more varied dataset to train their models on, all without ever touching sensitive customer information.

Beyond the data, this technology is also poised to handle sophisticated customer conversations. We're talking about moving past basic chatbots to systems that can offer detailed, empathetic advice through text or voice. This not only builds a stronger customer connection but also frees up human agents to focus on the most complex and urgent cases.

The Dawn of Proactive Intervention

The next big jump is from prediction to prevention. This is where prescriptive analytics comes in, and it's a genuine game-changer. It doesn't just flag a potential risk; it suggests the best course of action to take right now.

Let's say a weather model forecasts a severe hailstorm is going to pound a specific neighborhood in the next three hours. Prescriptive analytics would kick off a chain of events automatically:

- It sends personalized alerts to policyholders directly in the storm's path, urging them to get their cars under cover.

- It advises the insurer to pre-position claims adjusters near the high-impact zone to accelerate response times.

- It might even provide contact details for pre-approved auto glass repair shops to make recovery faster.

This changes the entire dynamic. The insurer becomes a true partner in preventing risk, not just a financial safety net after something goes wrong. It’s all about getting ahead of the problem before the damage is done.

The Power of Smart Contracts and Automation

Another exciting development is happening where the Internet of Things (IoT) and blockchain technology meet. This powerful combination makes "smart contracts" possible—agreements that execute themselves automatically when certain conditions are met because the terms are written directly into the code.

A smart contract automatically triggers a predefined action—like a claims payment—once a specific, verifiable event occurs. This removes manual intervention, dramatically increasing speed and trust.

Take flight delay insurance, for example. A smart contract could be connected to a secure, real-time flight data feed. If the data confirms your flight is delayed by more than two hours, the contract executes on its own and instantly sends the payout to your account. You don't have to file a claim, send in proof, or wait for someone to process it.

This is the future: a completely seamless and transparent experience that builds incredible customer loyalty and shows just how effortless insurance can be.

Frequently Asked Questions

It's natural to have questions as the insurance world embraces new technology. How does it all work? What does it mean for my business or my policy? Let's break down some of the most common questions about data analytics in insurance with straightforward, practical answers.

What Is the First Step to Implement Data Analytics?

The best advice I can give is to start small. Don't try to boil the ocean by overhauling the entire company at once. The most successful firms I've seen begin with a focused pilot project in a single, high-impact area.

For instance, you might decide to analyze historical claims data to fine-tune pricing for just one product line, like commercial auto insurance. This gives your team a manageable sandbox to learn in, iron out the kinks, and, most importantly, show a real return on investment. A successful pilot creates the momentum you need to get buy-in for bigger, more ambitious projects down the road.

The goal isn't immediate perfection, but measurable progress. A small, early win is the most powerful catalyst for driving a larger, data-focused cultural shift within the company.

How Does Data Analytics Directly Benefit Me as a Customer?

The biggest win for customers is fairer, more personalized pricing. In the old days, you were bucketed into a broad category based on a few simple data points. Now, your premium can actually reflect your individual behavior. If you're a safe driver, usage-based insurance programs can track your habits and reward you with a lower rate—it’s that simple.

Beyond just the price, data analytics makes the entire insurance experience smoother and faster. For customers, this translates to:

- Faster Claims Payouts: Automated systems can review, approve, and pay out simple claims in a matter of hours, not weeks. When you've had a loss, getting funds quickly makes a huge difference.

- Proactive Alerts: Insurers can now use data to spot risks ahead of time. Imagine getting a text alert that a hailstorm is heading for your neighborhood, giving you time to move your car to safety.

- Better Service: When routine tasks are automated, it frees up insurance professionals to focus on what humans do best: providing thoughtful advice on your more complex needs.

What Are the Biggest Challenges Insurers Face?

One of the toughest hurdles is definitely data governance and quality. Most insurers are working with data pulled from dozens of different systems, some of which are decades old. Just getting all that information to be clean, consistent, and secure is a massive technical undertaking. You can't run a meaningful analysis on bad data.

Another challenge is more cultural than technical. It involves shifting from a mindset of "gut instinct" and traditional underwriting to one that trusts data-driven insights. This means training people, getting them comfortable with new tools, and building a culture that values data literacy. Lastly, navigating the ethics of using customer data is a tightrope walk. It demands absolute transparency with policyholders and strict compliance with all privacy regulations.

At Wexford Insurance Solutions, we blend deep industry expertise with the right technology to protect what matters most to you. Our approach ensures you get competitive, accurate coverage without sacrificing personal service. Discover how our data-informed strategies can benefit you.

Cyber Security Risk Management | Essential Strategies & TipsDigital Transformation in Insurance Explained

Cyber Security Risk Management | Essential Strategies & TipsDigital Transformation in Insurance Explained