Think about it this way: trying to run an insurance business today with yesterday's tools is like navigating rush hour traffic with a paper map. Everyone else has a live GPS, and you're stuck. That's the reality for insurers who haven't embraced change. Digital transformation in insurance isn't some fleeting tech trend; it's a deep, fundamental shift in how the entire industry works, driven by new customer demands and market realities.

Why Digital Transformation Is No Longer Optional

For decades, the insurance industry was built on a solid foundation of paper files, long processing delays, and in-person meetings. It worked for a long time, but that model is now creaking under the strain of modern expectations. Today's world moves at the speed of a click, and customers expect the same instant, effortless experience from their insurer that they get from Amazon or their bank.

This isn't just about launching a website or a basic app. A genuine digital overhaul involves completely rethinking the insurance business from the ground up. It means using technology to tear down old silos, automate tedious manual work, and deliver far more value to both the policyholder and the company itself.

The Forces Driving Change

To understand why this shift is happening so quickly, it helps to look at the pressures forcing insurers' hands. There are several key drivers, both from outside the industry and from within, that are making digital evolution a necessity.

Core Drivers Forcing Digital Change in Insurance

| Driving Force | What It Means for Insurers | Real-World Impact |

|---|---|---|

| Evolving Customer Expectations | Policyholders now expect 24/7 self-service options. They want to manage policies, get quotes, and file claims on their own terms, often from their phones. | A customer is more likely to choose an insurer with a highly-rated mobile app over one that requires phone calls during business hours. |

| Operational Inefficiencies | Outdated legacy systems are expensive to maintain, slow to update, and create frustrating bottlenecks. Manual underwriting and claims processing lead to delays and errors. | An underwriter spending hours manually inputting data could instead be analysing complex risks, but the old system holds them back. |

| New Competitive Threats | Agile insurtech startups are entering the market. Built on modern tech stacks, they offer slick, user-friendly products with lower overhead, directly challenging established giants. | A startup offering on-demand car insurance via an app can steal market share from a traditional carrier with a lengthy, paper-based application process. |

These forces create a perfect storm, pushing established companies to either adapt or risk being left behind.

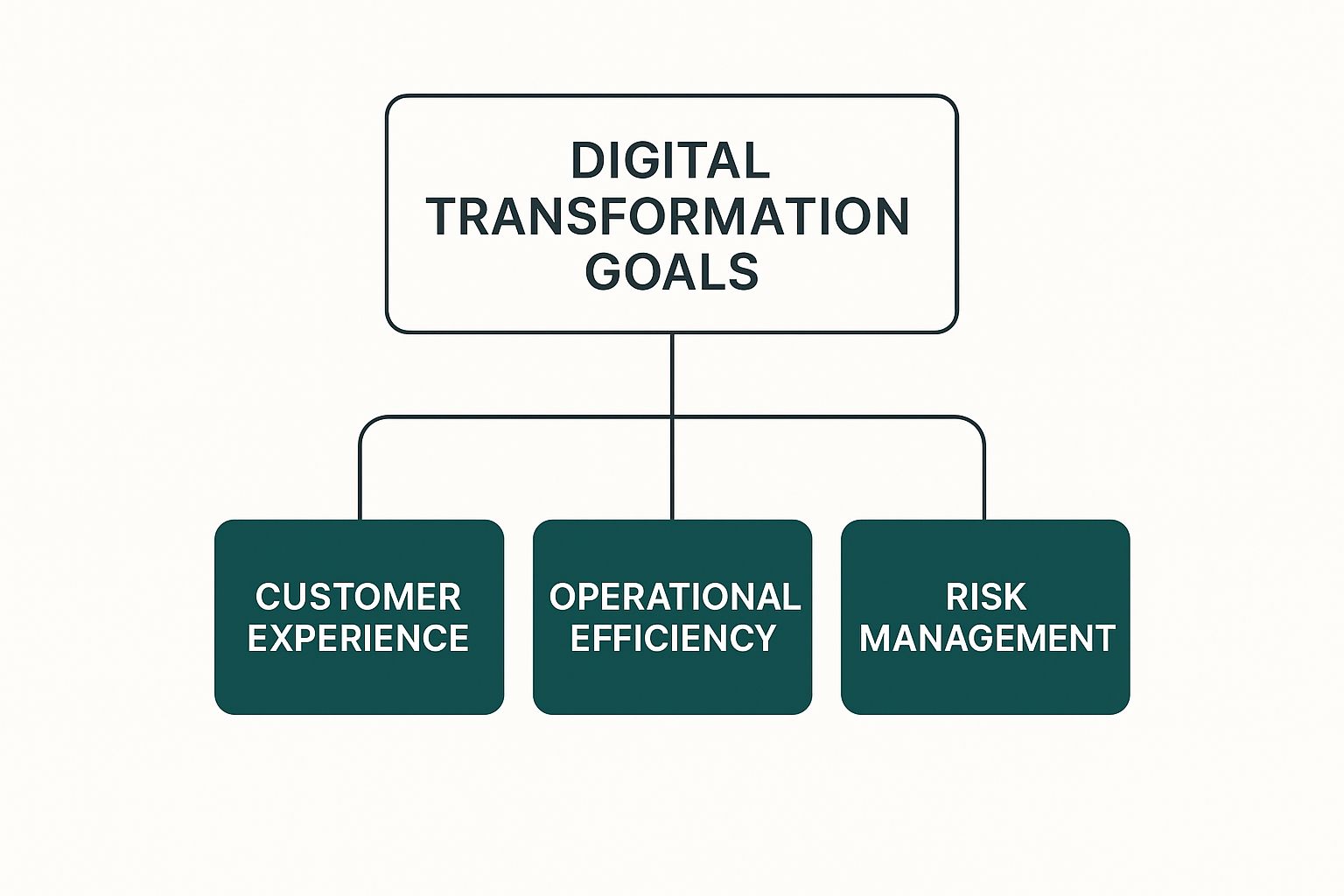

This infographic clearly breaks down the primary goals insurers are targeting as they navigate their own transformation journeys.

As you can see, the focus isn't just on one area. The most successful strategies are balanced, aiming to improve the customer experience, boost internal efficiency, and sharpen risk assessment all at once.

A Clear Shift In Industry Priorities

The push to modernize is happening everywhere. Recent reports show that a staggering 67% of insurance firms have hit the accelerator on their digital projects, actively moving away from the old, cumbersome systems.

This isn't a small-scale change. The digital insurance platform market is projected to reach an incredible $229 billion by 2029. That number alone shows the massive financial commitment and the sheer scale of this industry-wide evolution. You can find more details in various reports on digital insurance trends and statistics.

"The companies that are going to win are the ones that are going to deliver speed and an exceptional customer experience… When you speed things up, you give adjusters the tools to make better connections with your customers."

Ultimately, jumping into digital transformation is no longer a strategic "nice-to-have" for insurers—it’s a matter of survival. It's about building a leaner, smarter, and more customer-focused business that's ready for whatever comes next.

The Technologies Powering a Digital Insurance Future

Digital transformation in insurance isn't some abstract concept; it's being built on a foundation of specific, powerful technologies working together. These tools are the real engines of change, finally moving the industry from its paper-shuffling past toward a future of data-driven decisions. To really grasp what's happening, we need to look under the hood.

Think of it like building a modern car. You need an engine for raw power, a strong chassis for support, and an array of sensors to navigate the world. For an insurer, those roles are filled by Artificial Intelligence, Cloud Computing, and the Internet of Things (IoT). Each one is important, but their true power is unleashed when they work in sync.

It’s this combination that lets insurers automate soul-crushing manual tasks, understand risk with stunning precision, and, most importantly, create the kind of smooth customer experiences people now expect.

Let's break down these foundational technologies and see how they actually work in the real world.

Artificial Intelligence and Machine Learning

Artificial Intelligence (AI) and its key discipline, Machine Learning (ML), are the "brains" of the modern insurance operation. At their core, these systems are designed to sift through enormous amounts of data, spot patterns a human never could, and make predictions or decisions with little to no direct input. This is completely overhauling core functions that haven't changed in decades.

Take claims processing. It has always been a notoriously slow, hands-on affair. Now, AI can automate huge chunks of it. An AI can instantly scan a photo of a damaged car submitted with a claim, assess the damage against the policy details, and flag it for immediate payment or for an adjuster's review. This isn't just a minor improvement; it's been shown to slash processing costs by as much as 30%.

Beyond just speed, AI is an incredible fraud detector. By analyzing thousands of data points on a claim in real-time, its algorithms can pick up on subtle, suspicious patterns that even a seasoned adjuster might miss. This proactive defense saves the industry billions every year and helps keep premiums from climbing for everyone else.

Underwriting is another area being completely remade. Instead of relying on broad, often outdated demographic data, AI can build incredibly personalized risk profiles.

"By analyzing customer data, insurers can identify patterns and trends to personalize their offerings and improve customer satisfaction. They can also use predictive analytics to assess risk more accurately, enabling them to price policies more competitively and reduce fraud."

This leads to pricing that is not only more accurate but also more fair, shifting from a one-size-fits-all approach to a policy that truly reflects an individual's unique situation.

The Internet of Things (IoT)

If AI is the brain, the Internet of Things (IoT) provides the eyes and ears. IoT is simply the network of physical devices—from smart smoke detectors in a home to telematics sensors in a fleet of trucks—that are connected to the internet, constantly gathering and sharing data. This creates a live feedback loop between the insurer and the real-world risks they cover.

The most familiar example is usage-based insurance (UBI) for personal auto policies. A small telematics device in a car can track:

- Driving Habits: Monitoring things like hard braking, rapid acceleration, and speed helps reward safe drivers with lower premiums.

- Mileage: Enables pay-as-you-go policies, which are perfect for people who don't drive very often.

- Location Data: GPS tracking can trigger immediate assistance after a crash is detected.

Suddenly, insurance becomes less of a reactive product you only use after a disaster and more of a proactive partnership. In commercial lines, the applications are just as powerful. IoT sensors on a construction site can monitor for unsafe conditions, while sensors in a refrigerated truck can ensure a sensitive shipment stays at the perfect temperature, preventing spoilage and a costly claim.

Cloud Computing

Cloud computing is the foundational "chassis" that holds everything else together. It provides the flexible, on-demand computing power and data storage required to run sophisticated AI models and handle the firehose of data streaming in from IoT devices. Without the cloud, the kind of digital progress we're seeing today would be out of reach for all but the largest carriers.

Before the cloud, insurers were shackled to rigid, on-premise legacy systems that were a nightmare to maintain and update. The cloud gives them agility. They can scale their computing resources up or down as business demands, roll out new digital products in weeks instead of years, and collaborate more effectively. Harnessing data analytics for insurance becomes infinitely easier when your information is centralized and accessible from anywhere. This flexibility is non-negotiable for keeping up with nimble insurtech startups and fast-changing customer expectations.

Crafting the Modern Insurance Customer Journey

The real power of all this new technology becomes crystal clear when you trace a single customer's path, from their first curious click all the way to a paid claim. For decades, that journey was a minefield of friction, frustration, and stacks of paper. Now, we're finally able to reshape it into a smooth, intuitive experience that builds genuine loyalty.

Think about the old way. A potential customer sees a generic billboard, calls an office during business hours, gets put on hold, and then spends days slogging through forms just to get a price. The modern approach completely flips this on its head. The journey now starts with smart, proactive outreach.

From Cold Calls to Smart Connections

Instead of casting a wide, impersonal net, insurers are now using data to find the right customer with the right product at exactly the right time. Predictive models can analyze behaviors and life events—like a home purchase or a business expansion—to flag people who are probably in the market for a new policy.

This opens the door to truly personal marketing. A new homeowner might see a targeted ad on social media for a policy that speaks directly to the risks in their neighborhood. A business owner might get an email with a quote for commercial auto insurance just as they’re adding vehicles to their fleet. It’s a fundamental shift from interrupting people to being genuinely relevant.

This precision doesn't just boost conversion rates; it starts the entire relationship on the right foot. Customers feel understood from the very first touchpoint, which replaces the annoyance of a cold call with the relief of finding a timely solution.

Ditching Paperwork for Instant Policies

Once a customer is interested, that mountain of paperwork has been bulldozed and replaced by a sleek digital on-ramp. Those clunky, multi-page applications are giving way to clean online forms and mobile apps.

Here’s a look at how the modern application process unfolds:

- Smart Forms: Applications automatically fill in what's already known and use logic to skip irrelevant questions, slashing the time it takes to get through them.

- Instant Quoting: Instead of waiting days for an underwriter to dig through a file, algorithms can assess risk and generate an accurate quote in minutes—sometimes even seconds.

- Digital Issuance: The moment a quote is accepted, the policy can be issued, signed for electronically, and delivered straight to the customer’s digital wallet.

This kind of speed is a massive competitive advantage. A process that used to take a week can now be finished in the time it takes to grab a coffee.

The number of consumers willing to buy a policy without ever speaking to a person has shot up, growing by over 110% in just a few years. This sends a clear message: people want fast, self-service options.

Empowering Customers with 24/7 Control

After the policy is in force, the relationship deepens through self-service portals and AI-powered chatbots. Managing a policy used to be a chore that involved phone calls and waiting for mail. Now, it's a simple, on-demand task. Customers can log in anytime to:

- View policy documents

- Make a payment

- Update their coverage

- Add a new car or property

AI chatbots handle common questions around the clock, which frees up human agents to focus on the more complex, high-value conversations where their expertise really shines. This blend of automation and human insight creates an experience where customers feel both in control and well-supported.

Reimagining the Claims Experience

The claims process is the ultimate moment of truth. A slow, confusing experience can destroy years of loyalty in an instant. A fast, empathetic one can lock in a customer for life. New technology is completely overhauling this critical touchpoint, pushing it closer to a "touchless" model.

The new claims journey often starts with the customer snapping a few photos or a video of the damage with their smartphone. AI then gets to work, analyzing the images to assess the loss, checking it against the policy, and—for simple claims—approving the payment in minutes. One insurtech startup famously processed and paid a claim in a world-record three seconds.

This automation not only provides near-instant peace of mind for the customer but also dramatically cuts the administrative load and cost for the insurer. By making every step, from discovery to claim, feel effortless and transparent, this transformation turns insurance from a necessary product into an exceptional service.

Building Your Digital Transformation Roadmap

Jumping into a digital transformation without a clear plan is a recipe for disaster. It’s like buying a pile of expensive sailing equipment with no map, no compass, and no idea where you’re headed. A well-thought-out roadmap is that map. It gives you direction, ensuring every dollar spent and every process changed moves you closer to where you want to be.

The journey begins with a vision—one that everyone from the C-suite to the newest agent can get behind. This isn't about spouting tech jargon. It’s about painting a vivid picture of the future. For instance, instead of a dry goal like "implement an AI claims system," a truly motivating vision is: "We will settle 70% of simple claims in under an hour, giving our customers immediate peace of mind." See the difference? That's a business outcome that gets people excited and secures the buy-in you absolutely need.

Prioritizing for Maximum Impact

With a clear vision locked in, the next step is figuring out where to start. It’s easy to get overwhelmed and try to do everything at once, but that just leads to stretched resources and mediocre results. The secret is to find a few "quick wins" to build momentum.

Think of it like this: map all your potential projects based on their business impact and how hard they are to pull off. Start with the projects that promise high impact for low effort.

Here are a few examples of great starting points:

- Launch a customer self-service portal for things like making payments or downloading policy documents. It’s a simple move that cuts down on your team's admin work and gives customers the convenience they expect.

- Automate the First Notice of Loss (FNOL) process. A basic web form or a simple chatbot can handle the initial intake, freeing up your experienced claims handlers for more complex work.

- Bring in a digital signature tool like DocuSign or Adobe Acrobat Sign. This single change can eliminate the huge bottleneck of printing, signing, and scanning.

Nailing these initial projects proves the value of the transformation early on, making it much easier to get support for the bigger, more ambitious goals down the line, like a full core system replacement.

The Build vs. Buy vs. Partner Decision

Sooner or later, you'll face a critical question for every new capability you need: should we build it ourselves, buy it off the shelf, or partner with someone who already has it? There’s no single right answer here. The best path depends entirely on the specific initiative, your budget, your team's skills, and your long-term strategy.

The smartest strategies I've seen almost always use a mix of all three. For example, an insurer might buy a proven claims management system but partner with an insurtech startup to launch a really innovative usage-based insurance product.

Let's break down the choices.

| Approach | When It Makes Sense | Key Considerations |

|---|---|---|

| Build | For your "secret sauce"—the proprietary processes that give you a real competitive edge. Or when no existing software does what you need. | This route demands serious in-house tech talent, a lot of time, and deep pockets. But you get total control. |

| Buy | For standard business functions like HR or accounting. Anytime a proven, reliable solution is already on the market. | You can get up and running much faster and for less money upfront. The trade-off is less customization. |

| Partner | To get your hands on specialized tech quickly or break into a new market. A great way to innovate without the heavy cost of R&D. | This lets you tap into the speed and creativity of startups, but you have to choose your partners wisely and manage the relationship well. |

Making the wrong call here can be costly, leading to wasted resources or blown opportunities. For example, building a generic customer portal from scratch in-house is almost always a poor use of time and money when so many excellent "buy" options are available.

Ultimately, a great roadmap isn't set in stone. It has to be a living document, ready to adapt as the market shifts and new technologies pop up. That flexibility, combined with a sharp vision and smart priorities, turns the daunting challenge of digital transformation in insurance into a manageable, and even exciting, journey. A well-executed plan not only readies your business for what's next but also strengthens its ability to withstand disruption—a vital concept we explore further in our guide to business continuity insurance.

Real-World Examples of Digital Insurance Success

Theory is one thing, but seeing digital transformation in action is where the real lessons are learned. Let's move past the buzzwords and look at how real companies are using these tools to get ahead. These examples show what’s possible when an insurer truly commits to a modern, digital-first approach.

One of the best-known disruptors in personal lines is Lemonade. They didn't just adapt to the digital world—they were born in it. Lemonade built its entire business from the ground up on artificial intelligence and a slick mobile experience, completely resetting customer expectations.

Their challenge was breaking into a crowded market full of established giants. Their solution? Ditch the brokers and the paperwork. Their AI chatbot, Maya, can generate a quote in 90 seconds and bind a policy just a few minutes later. For a generation that lives on their phones, that kind of speed isn't a perk; it's the standard.

The story everyone talks about is Lemonade's claims AI, Jim, who famously reviewed, approved, and paid out a claim for a stolen coat in a stunning three seconds. This wasn't just a publicity stunt; it was a powerful statement about how automation can deliver an incredible customer experience when it matters most.

From Reactive to Proactive in Commercial Lines

These ideas aren't just for personal insurance. In the commercial world, leading carriers are using technology to flip the script—moving from just paying for losses after they happen to actively helping clients prevent them in the first place. It turns the insurer-client relationship into a genuine partnership.

Think about a massive construction project, a place humming with potential risks. One top commercial insurer now outfits these sites with a network of Internet of Things (IoT) sensors. These small devices are constantly on the lookout for trouble, monitoring things like:

- Water leaks that could cause catastrophic damage.

- Unsafe temperature changes in sensitive areas.

- Someone entering a restricted zone after hours.

This firehose of real-time data lets the insurer give the construction manager a heads-up before a small issue becomes a massive claim. The result is a safer worksite, fewer expensive claims, and a much stronger client relationship built on proactive risk management. This strategy is also crucial for preventing operational shutdowns, which directly relates to understanding the business interruption insurance cost and its immense value. It's a win-win that lowers the total cost of risk for everyone.

Digital Technology Impact on Personal vs Commercial Insurance

These case studies reveal a clear pattern for success. It's not about just buying new software; it’s about using technology to solve specific problems and create real, measurable value. The table below gives a snapshot of how these technologies are applied differently—but just as effectively—across the personal and commercial sectors.

| Technology | How It's Used in Personal Lines | How It's Used in Commercial Lines |

|---|---|---|

| Artificial Intelligence | Powers instant quoting, mobile claims processing, and 24/7 customer service chatbots. | Analyzes vast datasets to identify fraud patterns, price complex risks, and predict supply chain disruptions. |

| IoT & Telematics | Enables usage-based auto insurance by tracking driving behavior for personalized premiums. | Uses sensors on equipment and job sites to monitor conditions and prevent accidents and property damage. |

At the end of the day, both Lemonade and the forward-thinking commercial carrier succeeded because they shared a common goal: using technology to build a faster, smarter, and more valuable experience for their customers.

How to Overcome Common Transformation Hurdles

The journey toward a digitally savvy insurance company is never a straight shot. It's more like a winding road, often dotted with roadblocks that can drain your budget, slow down progress, and leave your teams feeling defeated. The secret isn't avoiding every obstacle—it's knowing what they are ahead of time so you can navigate them skillfully.

Frankly, just getting started is a massive challenge. A staggering 73% of enterprises admit they haven't seen any real business value from their transformation efforts. This usually happens when the project is viewed as an IT-only task instead of what it truly is: a fundamental shift in how the business operates.

Integrating the New with the Old

For any insurer with a few decades under its belt, the biggest technical monster in the room is almost always the legacy systems. We're talking about those rigid, often decades-old core platforms that hold the keys to the kingdom: all your policy and customer data. Trying to connect modern, flexible tools to these systems can feel like trying to sync a new smartwatch with a 1980s brick phone.

This integration work is delicate. One wrong move could disrupt daily operations, corrupt vital data, or send project costs spiraling. That's why a thoughtful, phased approach beats a risky "rip and replace" strategy every time.

- Make APIs Your Best Friend: Think of Application Programming Interfaces (APIs) as universal translators. They create bridges that allow your shiny new digital tools to talk to your old systems without having to perform major surgery on the core platform.

- Decouple Your Data: Start a gradual process of moving data from those old mainframes into a more modern, cloud-based data warehouse. This unlocks its power for real-time analytics without breaking the systems that run your day-to-day business.

- Focus on the Customer First: You can deliver value quickly by building modern, customer-facing apps—like a new portal or mobile app—that simply pull data from the old systems. This buys you time and goodwill while you plan the deeper backend overhaul.

Managing Security and Internal Resistance

The more data you collect from telematics, smart home devices, and online interactions, the bigger the target on your back becomes. Every new digital touchpoint is another potential door for bad actors. A rock-solid, comprehensive security plan isn't just a good idea; it's non-negotiable.

"Leaders who fail to manage this change will struggle with digital transformation. To reap the benefits of a digital overhaul, leaders must clearly communicate the degree of change and retire old processes. Merely implementing new technology is not enough."

This gets to the heart of the matter: the human element is just as critical as the technology. Internal resistance can quietly sink the most brilliant strategy. Employees might worry that their roles will be automated away or feel completely overwhelmed by new workflows. The only way to counter this is with proactive change management. You have to build a culture where technology is seen as a helpful partner, not a threat. For a deeper look at protecting your digital assets, check out our guide on effective cyber security risk management.

Avoiding Pitfalls and Proving Value

Finally, two huge hurdles can stop a project in its tracks: the siren song of trendy tech and a failure to show results. "Shiny object syndrome"—chasing the latest technology without a clear business case—is a fast way to burn through cash with nothing to show for it. Every dollar you invest must be tied to a specific, measurable goal, like cutting claims cycle time or boosting customer retention.

This brings us to the challenge of proving Return on Investment (ROI). Transformation is a marathon, not a sprint, but leadership needs to see mile markers along the way to keep funding the race.

Strategies for Success:

- Go for Quick Wins: Start by tackling a few high-impact, low-effort projects. This builds momentum and proves the concept to skeptics.

- Set Clear Metrics: Before you write a single line of code, define your Key Performance Indicators (KPIs). Track things like cost per claim, policy issuance time, and Net Promoter Score.

- Communicate Constantly: Share updates, data, and small victories with the entire company. Keeping everyone in the loop is essential for maintaining support for the long-term vision.

Frequently Asked Questions About Digital Insurance

Diving into the world of digital transformation in insurance can feel overwhelming, and it's natural to have questions. Let's clear up some of the most common ones with straightforward, practical answers.

What Is the Best First Step for an Insurer to Begin a Digital Transformation?

Honestly, the best first step has nothing to do with technology. It’s about people and process. Before you even think about software, you need to pinpoint your biggest headache. Is your claims process painfully slow? Do customers abandon your online quote form out of frustration?

Get specific. Define a clear, measurable goal, like aiming to "reduce claims processing time by 40%" or "boost online quote completions by 50%." Once you have that clear vision, you need strong leadership backing to champion the project and secure the resources to make it happen.

How Does This Transformation Change the Role of an Insurance Agent?

It doesn't replace the agent; it supercharges them. Think of it as taking all the tedious, repetitive administrative work off their plate. By automating things like data entry and paperwork, you free up your agents to focus on what they do best.

This shift allows agents to invest their time in what really matters: building genuine client relationships, offering expert advice on complex risks, and delivering standout service. Digital tools give them better data and sharper insights, elevating their role from a simple go-between to a truly trusted risk advisor.

Is Digital Transformation Only for Large Insurance Carriers?

Not at all. That’s a common myth. In fact, smaller and mid-sized insurers often have an advantage—they can move much faster and adapt more nimbly than their massive, slow-moving competitors. Success isn't about the size of your budget; it’s about the clarity of your strategy.

Modern cloud-based platforms and smart partnerships with insurtechs give smaller firms access to incredible digital tools without a huge upfront investment. For smaller players, including specialized consultants who need the right protection, digital tools are a powerful way to compete. You can learn more about finding the right consultants insurance coverage to see how specific needs are addressed. For these insurers, going digital is the key to standing out with superior service and winning in niche markets.

At Wexford Insurance Solutions, we bring together smart technology and personal service to make your insurance experience simpler and clearer. With our 24/7 client portal and intelligent claims advocacy, we're dedicated to providing clarity and peace of mind. To see how our digital-first approach can work for you, visit us at https://www.wexfordis.com.

Data Analytics for Insurance Explained9 Insurance Industry Technology Trends Shaping 2025

Data Analytics for Insurance Explained9 Insurance Industry Technology Trends Shaping 2025