Think of an insurance gap analysis as a comprehensive health check-up for your financial protection. It’s a systematic review designed to find the dangerous blind spots and shortfalls in your current insurance coverage. Essentially, you’re comparing the risks you actually face against the protection your policies provide, pinpointing exactly where you might be underinsured or, worse, completely uninsured.

Why Your Current Insurance Might Be a Leaky Ship

Imagine your financial life is a sturdy ship, built to carry you through life's unpredictable waters. Your insurance policies are the hull, designed to protect everything you value—your family, home, business, and income—from the inevitable storms.

An insurance gap analysis is like a detailed inspection of that hull. It’s a search for the hidden cracks, weak spots, and holes you never knew were there. Without this regular check-up, you could be sailing confidently into a hurricane, completely unaware that your protection is about to fail when you need it most.

This process isn't about just having insurance; it’s about having the right insurance. So many people and businesses operate under a false sense of security, assuming their standard policies have them covered. The reality is often painfully different. A basic homeowner's policy likely won't cover flood damage, and a standard business liability policy might leave you exposed to the massive costs of a data breach. These are the kinds of gaps that can sink you financially.

Moving from Assumption to Certainty

The whole point of a gap analysis is to stop guessing and start knowing. It's a fundamental risk management exercise, whether you're protecting your personal assets or a commercial enterprise. Instead of just hoping you're covered, you get a clear, documented picture of your true vulnerabilities. This knowledge empowers you to make smart, informed decisions and build a financial safety net that you can actually rely on.

An insurance gap analysis isn't just about buying more insurance; it's about buying the right insurance. It transforms your coverage from a collection of policies into a cohesive strategy designed to protect what matters most.

The Real-World Consequences of Gaps

Failing to spot these gaps can be devastating. A family could lose their home in a fire, only to find out their policy’s rebuilding limit was based on a property valuation from 10 years ago, leaving them with a crippling financial shortfall. A growing business could get hit with a lawsuit that blows past its liability limits, putting its entire future on the line.

Performing an insurance gap analysis is more critical than ever as risks continue to change. The modern world brings new challenges, from sophisticated cyber threats to increasingly frequent climate-related disasters—risks that older policies were never built to handle. Understanding the digital transformation in insurance highlights how new tools and data can help us identify these emerging threats. Ultimately, a proactive analysis gives you a clear roadmap to secure your future against both old and new dangers.

The Growing Global Protection Gap

To really grasp why an insurance gap analysis is so important for your business or family, you need to understand a massive global trend: the widening protection gap. This isn't just some dusty term from an insurance textbook. It's the very real, and growing, difference between the total economic cost of a disaster and what insurance actually pays out.

Imagine it like this: a major hurricane slams into a coastal region, causing $50 billion in total economic damage. But when the dust settles, insurance policies only cover $20 billion of that cost. The remaining $30 billion is the "gap." That money doesn't just vanish—it's a heavy burden that falls on families, business owners, and taxpayers who are left to pick up the pieces with their own savings, unmanageable debt, or through government relief programs.

This gap is getting wider every year because the risks we face are changing faster than insurance policies can keep up. There are two major forces stretching this gap, making a proactive review of your own coverage an absolute necessity.

Climate Change and Catastrophic Events

The most obvious driver here is the sheer increase in the frequency and intensity of climate-related disasters. What used to be "once-in-a-century" floods, wildfires, or storms are now becoming disturbingly regular events. They're causing more damage and pushing economic losses to staggering new heights.

This new reality has a direct impact on the insurance market. As the risk of massive payouts grows, insurers have to react, and that usually means:

- Higher Premiums: It simply costs more to insure something that's more likely to be destroyed.

- Stricter Underwriting: Insurers get a lot pickier about what and who they are willing to cover in high-risk areas.

- Market Exits: In the most extreme cases, insurance companies pull out of certain regions altogether, leaving property owners with virtually no options.

It's a vicious cycle. Just when people need coverage the most, it becomes the hardest to find and afford.

The protection gap represents a systemic risk to our financial stability. It highlights a fundamental disconnect between the escalating threats we face and the adequacy of our collective safety nets.

The Rise of Modern Risks

It’s not just Mother Nature, either. The very fabric of our modern world is weaving new kinds of threats. Risks that were barely a blip on the radar a decade ago are now front and center.

Cybercrime is the perfect example. A single data breach can cripple a business, leading to millions in direct losses and reputational damage. Yet, many standard business policies offer absolutely no coverage for this kind of modern-day disaster.

A recent Bain & Company report paints a sobering picture, projecting that these protection gaps will only get worse across the board through 2030. Their analysis suggests that by then, only about a quarter to a third of all damages from natural catastrophes will be insured.

When you see this bigger picture, it becomes clear that being underinsured isn't just a simple oversight. It's a vulnerability in a world where risks are growing while the default safety net is shrinking. An insurance gap analysis is your tool to push back against these forces and make sure your financial defenses are built for the world we live in today—not the one that existed ten years ago.

How to Perform Your Own Insurance Gap Analysis

Thinking about an insurance gap analysis can feel a bit overwhelming, but it's really just a systematic way to check if your financial safety net has any holes. Think of it like this: you wouldn't head out on a long road trip without checking your spare tire. This process is the financial equivalent—making sure you’re truly prepared for bumps in the road.

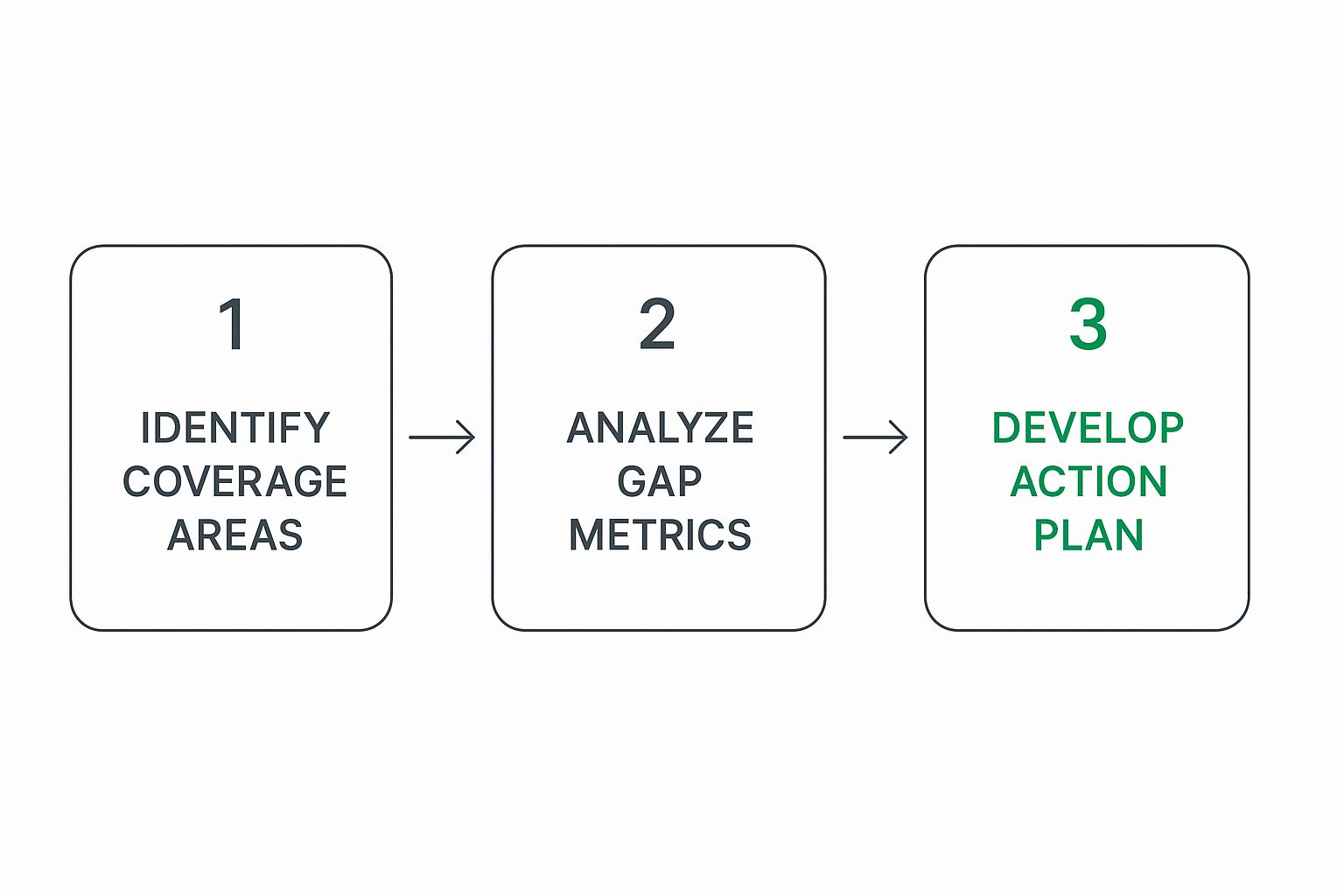

It’s all about methodically comparing what you need to protect with the protection you actually have. I'm going to walk you through a straightforward, four-step framework to do just that. Follow along, and you’ll go from feeling uncertain about your coverage to having a clear, actionable plan.

This infographic breaks down the workflow nicely, showing the journey from initial assessment to a final action plan.

As you can see, a good analysis isn't just a single event; it's a structured process. It starts with figuring out what you have and ends with a concrete strategy to close any gaps you find.

Step 1: Take Stock of Your Assets and Liabilities

You can't protect what you haven't measured. So, the very first thing to do is make a complete list of everything you own (your assets) and everything you owe (your liabilities). This exercise gives you a crystal-clear picture of your net worth and, more importantly, the total value you have at risk.

For an individual or a family, this list would typically include:

- Real Estate: Your primary home, any vacation properties, or rental units.

- Vehicles: All your cars, boats, motorcycles, or RVs.

- Personal Belongings: Think furniture, high-end electronics, jewelry, art, and other collectibles.

- Financial Assets: This covers savings and checking accounts, investments, and retirement funds.

For a business owner, the inventory gets a bit more involved:

- Physical Assets: The building itself, all equipment and machinery, inventory, and any company vehicles.

- Financial Assets: This means cash on hand and your accounts receivable.

- Intangible Assets: Don't forget things like intellectual property, your brand's reputation, and critical customer data.

While you're at it, list out all your liabilities—mortgages, auto loans, student loans, and business debts. This complete financial snapshot is the foundation for everything that comes next.

Step 2: Identify and Assess Your Potential Risks

Okay, now you have a clear view of what needs protecting. The next move is to brainstorm all the things that could possibly go wrong and threaten those assets. You need to think broadly here, covering both the common stuff and the less-obvious risks that are unique to your life or business.

Some risks are pretty universal, but many depend entirely on where you live, your lifestyle, or how you run your business. A coastal business in Florida, for instance, faces a significant hurricane risk. A tech startup in Silicon Valley? Their biggest threat might be a massive data breach.

A risk isn't just an event; it's an event with a financial consequence. The goal is to connect potential threats directly to the assets they could impact, estimating the potential financial damage.

Start making a list of these potential perils. It might include:

- Natural Disasters: Floods, earthquakes, wildfires, hurricanes, and tornadoes.

- Property Damage: The classic threats like fire, theft, and vandalism.

- Liability Lawsuits: Someone slipping and falling on your property or a lawsuit filed against your business.

- Business-Specific Risks: Professional errors, data breaches, or major supply chain disruptions.

- Personal Risks: An unexpected death, a disability that prevents you from working, or a long-term illness that drains your savings.

Step 3: Review Your Existing Insurance Policies

It’s time to pull out the paperwork. Gather every single policy document you have—home, auto, life, health, disability, and any policies for your business. The mission here is to understand exactly what is covered and, just as importantly, what isn't.

Don't just glance at the policy names on the declaration pages. You need to dig into the fine print. Specifically, look for:

- Coverage Limits: What’s the absolute maximum the policy will pay for a covered loss? For example, is your $500,000 home only insured up to $400,000? That’s a major gap.

- Deductibles: How much money do you have to pay out of your own pocket before the insurance company starts paying?

- Exclusions: This is critical. What specific events or situations are explicitly not covered? This is where some of the nastiest surprises hide. For instance, most standard homeowners policies do not cover damage from floods or earthquakes.

- Endorsements or Riders: Do you have any special add-ons to your policy? These might provide extra coverage for things like valuable jewelry or business equipment you keep at home.

This detailed review is where the gaps will really start to jump out at you. You might realize your liability coverage is dangerously low for your net worth or that your business interruption insurance has a long waiting period that could sink you.

Step 4: Pinpoint and Prioritize the Gaps

This is where it all comes together. Compare your list of assets and risks (from steps 1 and 2) with what your insurance actually covers (from step 3). This direct comparison will reveal your insurance gaps—the specific areas where your potential financial losses are greater than your protection.

Write down each gap you find. Be specific. For example: "Gap: Potential flood damage to home. Current homeowners policy has a flood exclusion. Financial exposure: $350,000."

Once you have a list, it’s time to prioritize. Not all gaps carry the same weight. A gap that could lead to financial ruin (like having way too little liability coverage) is far more urgent to fix than one that would just be an inconvenience. Rank them based on:

- Severity: How devastating would the financial impact be if this event happened?

- Likelihood: What’s the real-world probability of this risk occurring?

This prioritized list is now your action plan. It tells you exactly what to talk about when you meet with an insurance professional. The insights from this process are incredibly valuable, and for those who want to go even deeper, using data analytics for insurance can help refine this kind of risk assessment to an even greater degree.

Discovering Your Hidden Insurance Gaps

Here’s an uncomfortable truth about insurance: many people who believe they're fully covered are actually living with a false—and dangerous—sense of security. Costly gaps often hide in the fine print of standard policies, just waiting for a crisis to expose them. An insurance gap analysis is how you turn on the lights and see exactly where your financial safety net is weak.

These gaps aren't rare; they're incredibly common. They exist because "off-the-shelf" insurance is built for a generic customer, not for your specific life, assets, and risks. Let's dig into some of the most frequent and financially damaging gaps that catch both individuals and businesses completely by surprise.

Common Gaps in Personal Insurance

For individuals and families, the biggest holes in coverage usually involve major catastrophes and liability risks that blow right past standard policy limits. The difference between what you think is covered and what your policy will actually pay out can be devastating.

Homeowners insurance is a classic example. A standard policy offers great protection against fire or theft, but it almost always excludes coverage for floods and earthquakes. If you live in a flood-prone area without a separate flood policy, you're just one heavy storm away from potential financial ruin.

Liability is another major blind spot. Sure, your auto or home policy includes liability protection, but are the limits high enough? Let’s say your net worth is $1 million, but your auto policy’s liability limit is only $300,000. That leaves a $700,000 gap. A serious at-fault accident could expose your savings, investments, and even future earnings to a lawsuit.

The most dangerous insurance gap is the one you don't know exists. It's the risk you assumed was covered but wasn't, creating a direct and often unmanageable path to financial hardship.

Consider these other frequently overlooked personal gaps:

- Valuable Items: Standard policies put very low limits on things like jewelry, art, and high-end electronics. A $5,000 engagement ring might only be covered for $1,500 unless you add a special rider or endorsement.

- Rebuilding Costs: Many homes are insured for their market value, not their true rebuilding cost. After a total loss, the expense of demolition, debris removal, and rebuilding to current code can be much higher, leaving a huge shortfall.

Critical Gaps for Modern Businesses

For businesses, the risk landscape has changed dramatically, and insurance policies have struggled to keep up. The gaps here often relate to modern, non-physical threats that can be just as destructive as a fire.

The most glaring example today is cyber liability. A standard general liability policy will not cover the staggering costs of a data breach, which can include forensic investigations, customer notifications, credit monitoring, regulatory fines, and legal defense. For a small or mid-sized business, a single cyber incident can be an extinction-level event.

Another is professional liability, often called errors and omissions (E&O) insurance. If your business provides advice or a professional service—like a consultant, accountant, or architect—you can be sued by a client for a mistake that cost them money. A standard policy won't touch this.

Finally, one of the most misunderstood coverages is business interruption insurance. Many businesses have it, but they don't realize its limits. A basic policy might not cover shutdowns caused by a cyberattack or a supply chain failure unless specifically endorsed. To truly grasp how to protect your revenue, it's worth exploring the details of business continuity insurance.

To make this crystal clear, let's look at a few examples of standard policies versus what's often needed to be truly protected.

Standard vs. Comprehensive Coverage Examples

| Risk Area | Standard Policy Coverage (And Its Limits) | Coverage Needed to Close the Gap |

|---|---|---|

| Natural Disasters | Homeowners insurance typically covers fire and wind but excludes floods, earthquakes, and landslides. | A separate, dedicated Flood Insurance or Earthquake Insurance policy. |

| High-Value Assets | A standard policy has low sub-limits on personal property like jewelry (e.g., $1,500) or fine art. | A Personal Article Floater or Scheduled Personal Property Endorsement to cover items for their appraised value. |

| Major Liability | Auto/Home policies have liability limits (e.g., $300,000 or $500,000) that may not cover your total net worth. | A Personal Umbrella Policy to add an extra $1 million or more in liability protection over your existing policies. |

| Cyber Attacks | General Liability policies do not cover data breach costs, ransomware payments, or digital forensic services. | A standalone Cyber Liability Insurance policy designed for modern digital risks. |

| Professional Mistakes | General Liability covers bodily injury or property damage, but not financial loss from professional advice or services. | Errors & Omissions (E&O) Insurance to protect against claims of negligence or mistakes in professional work. |

This practical review of common gaps proves that a proactive insurance gap analysis isn't just a paper-shuffling exercise. It's an essential strategic process for turning abstract risks into tangible scenarios you can actually prepare for, ensuring your financial foundation is strong enough to handle whatever comes your way.

Why Global Events Impact Your Insurance Needs

Your insurance coverage doesn't exist in a vacuum. It lives in a world that's constantly in flux, and major global events—especially those tied to our climate and economy—can have a very real impact on your policies, your premiums, and even your ability to get coverage at all. Grasping this connection is a huge part of why a regular insurance gap analysis has shifted from a good idea to an absolute necessity.

The days of "set it and forget it" insurance are long gone. The comprehensive, affordable policy you locked in a few years ago might not be enough—or even available—in today's market. This new reality demands a more hands-on approach, where you're constantly adapting your protection to a world of ever-changing risks.

The Ripple Effect of Climate Catastrophes

Perhaps the biggest driver of change in the insurance world is the escalating severity of climate-related disasters. We’re all seeing it: more frequent and intense wildfires, floods, hurricanes, and storms. These events have a direct, bottom-line impact on insurance carriers. As their potential for enormous payouts skyrockets, they have no choice but to make big adjustments to stay afloat.

For consumers and businesses, this usually plays out in a few predictable ways:

- Rising Premiums: It’s simple economics. When the risk of a claim goes up, so does the cost to insure against it.

- Tighter Underwriting Rules: Insurers get a lot pickier about who and what they'll cover, particularly in areas they now consider high-risk.

- Market Withdrawals: In the most extreme situations, companies might pull out of a region entirely, leaving property owners scrambling for any available option.

This creates a painful paradox: the need for solid protection is greatest right when it becomes the most expensive and hardest to find.

A Stark Global Reality

This isn't a problem confined to one city or state; it's a worldwide issue with staggering financial implications. The gap between economic losses from natural disasters and what’s actually insured is massive. According to the 2025 EY Global Insurance Outlook, total economic losses from these events hit about $2.35 trillion between 2014 and 2023. Here’s the shocking part: only $944 billion of that was insured. That leaves an enormous protection gap of $1.4 trillion, meaning 60% of all losses were uninsured. You can dig into the numbers yourself in the full insurance outlook report on EY.com.

The connection is crystal clear: large-scale global events directly shrink the margin of error in your financial plan. A small coverage gap that seemed trivial five years ago could now be the very thing that leads to a catastrophic financial failure.

This reality is precisely why a modern insurance gap analysis must look beyond your four walls. For instance, if you run a service-based business, you might not worry about floods or supply chains. But what if a client claims your advice caused them a major financial loss? This is where a professional liability policy becomes your lifeline, a topic we cover in our guide on what is errors and omissions insurance.

These evolving, large-scale risks are the reason a periodic, in-depth review of your insurance is no longer just good practice—it's a core component of smart financial stewardship.

From Analysis to Action

An analysis is just a document until you do something with it. After all the hard work of mapping out your risks and finding where your coverage falls short, this is the most important step: turning those insights into real-world protection. Think of it as your roadmap for building a financial fortress.

The first move is to talk to a pro. Take your prioritized list of gaps to an independent insurance agent. This isn't your typical sales call; it's a strategic meeting. Armed with your analysis, you can skip the generic pitches and get right down to business, focusing on solutions that fit your specific situation. You're no longer just a customer—you're an informed buyer ready to have a serious conversation about raising liability limits or finally adding that flood policy you now know you need.

Prioritizing Your Next Steps

You've got a clear picture of your weak spots. Now, what do you tackle first? Especially if you're on a budget, you can't fix everything at once. Not all gaps carry the same weight, so you need a smart way to decide.

Here’s a simple framework to guide your thinking:

- Tackle the Biggest Threats First: Start with the gaps that could completely derail your financial life. A major liability lawsuit or losing your home to an uninsured disaster are the kinds of risks that need to be at the very top of your list.

- Consider the Odds: Next, look at how likely an event is. If your business is in an area with a high crime rate, beefing up your theft and vandalism coverage makes a lot of sense. Similarly, a property in a known flood plain absolutely needs a dedicated flood policy.

- Weigh the Cost vs. the Risk: Compare the price of the new insurance premium against the potential financial ruin of leaving that gap exposed. More often than not, you'll find that the cost of crucial protection is a small price to pay for genuine peace of mind.

The real goal here is to systematically eliminate the risks that could cause the most catastrophic financial damage. Your analysis gives you the clarity to make these tough calls logically, not emotionally.

How Technology Helps Close the Gaps

Luckily, you don’t have to do this with outdated tools. The insurance world is catching up, and new technology is making it much easier to find coverage that fits like a glove. Insurers are getting better at using data to design specialized products, moving away from the old one-size-fits-all approach.

What's driving this? Powerful new efficiencies. A report from Bain highlights that AI-powered tools could boost revenue growth by 10-15% and slash operating expenses by up to 30% for insurers. For you, the consumer, this is great news. It means more affordable and highly specific products are becoming available to patch those exact gaps you've identified. You can see more on these emerging insurance industry technology trends and what they mean for your wallet.

At the end of the day, an insurance gap analysis isn't a one-and-done project. It’s a living part of your financial toolkit. It empowers you to stay ahead of risk, ensuring that as your life and business evolve, your protection keeps up.

Frequently Asked Questions

Let's dig into some of the most common questions people have about insurance gap analysis. Getting these answers can give you the confidence to move forward and make sure you're properly protected.

How Often Should I Perform an Insurance Gap Analysis?

While there isn't a single magic number, a great rule of thumb is to review everything thoroughly at least every 1-2 years. Think of it as a regular financial health check-up.

More importantly, you should immediately conduct an insurance gap analysis any time you experience a major life or business change. These are the moments when your risk profile shifts dramatically.

Key triggers include:

- Getting married or divorced

- Buying a new home or another valuable asset

- Starting a business or seeing a major growth spurt

- Welcoming a new child into the family

Your insurance coverage shouldn't be a "set it and forget it" item. It needs to evolve right alongside your life.

Can I Do a Gap Analysis Myself or Do I Need a Professional?

You can—and should—absolutely start the process on your own. Walking through the steps of inventorying what you own, thinking through potential risks, and reviewing your current policies is an incredibly empowering exercise. It makes you a much smarter, more engaged insurance buyer.

That said, when it comes to closing those gaps with the right insurance products, bringing in an expert is a very smart move. An experienced, independent agent has access to a wide range of carriers and can spot nuances in policy language that are easy for a layperson to miss.

A self-analysis helps you identify the problems, while a professional helps you implement the best solutions. The combination of your personal knowledge and their industry expertise leads to the strongest possible outcome.

Is an Insurance Gap Analysis Only for Businesses?

Not in the slightest. While it's a cornerstone of risk management for any company, an insurance gap analysis is just as vital for individuals and families. The financial fallout from being underinsured can be absolutely devastating on a personal level.

For a family, the analysis might reveal critical shortfalls in life insurance after having a child, or a lack of disability coverage that could threaten your entire financial future. At the end of the day, this process is all about protecting what you've worked so hard to build.

An insurance gap analysis provides the clarity you need to build a financial safety net that truly protects you. At Wexford Insurance Solutions, our experts use this detailed process to go beyond one-size-fits-all policies, creating personalized coverage that matches your unique risks. Secure your future by scheduling a comprehensive review with our team today at https://www.wexfordis.com.

9 Insurance Industry Technology Trends Shaping 2025Create a Business Income Worksheet for Better Financial Planning

9 Insurance Industry Technology Trends Shaping 2025Create a Business Income Worksheet for Better Financial Planning