In the insurance world, the concept of risk and analytics is about a fundamental change in mindset—moving from looking in the rearview mirror to scanning the road ahead. It's the practice of using sophisticated data analysis, statistical models, and modern technology to see risks before they happen, price policies more accurately, and simply make smarter decisions. This isn't just about reviewing what went wrong in the past; it's about predicting what could happen next.

The New Reality of Insurance Risk and Analytics

Think about the difference between navigating a new city with a static paper map versus a live GPS. For years, insurers used their own version of a paper map—historical claim data and time-tested actuarial tables—to navigate the uncertain world of risk. This traditional approach worked, but it was always looking backward. Insurers would assess the damage after a hurricane, calculate losses after a car accident, and then adjust next year's premiums based on those past events.

Today, everything is different. The combination of risk and analytics gives insurers a dynamic, forward-looking GPS. It lets them see the "traffic jams" of risk forming on the horizon and reroute before they get stuck. This isn't just a small tweak; it’s a complete reimagining of how the insurance business works.

From Reactive Measures to Proactive Strategies

The heart of this change is the move from a reactive stance to a proactive strategy. Instead of just paying for losses after they occur, today's insurers use data to help prevent those losses or at least lessen their impact. This new way of thinking is built on a constant flow of data and powerful analytical tools.

The difference is stark:

- Traditional Approach: Depended on static, historical information to sort people into broad risk pools. Pricing was often based on general demographics and past loss trends for a whole group.

- Modern Approach: Taps into dynamic, real-time data from sources like telematics devices in cars, IoT sensors in buildings, satellite imagery, and even social media sentiment. This creates a much more detailed and individual picture of risk.

This shift allows insurers to move past one-size-fits-all policies. For instance, rather than charging every young male driver a high premium, an insurer can now use telematics data to offer a safe young driver a lower rate based on their actual, measured driving habits.

This strategic pivot comes from a simple truth: in our complex world, what happened yesterday is no longer a guaranteed predictor of what will happen tomorrow. The ability to analyze diverse, live data is now the foundation of any competitive insurance company.

Why This Shift Matters Now

The need for this change is being driven by a world full of new and complicated risks. Climate change is creating weather patterns we’ve never seen before, cyber threats appear and change in the blink of an eye, and global supply chains are more fragile than ever. Trying to navigate this new territory with old maps is a recipe for getting lost.

By embracing risk and analytics, insurers aren't just getting better at managing risk—they're finding new opportunities. They can design innovative products, provide a much better customer experience, and run their businesses more efficiently. This guide will explore this new reality, showing you how analytics is rebuilding the industry from the inside out, making insurance smarter, more responsive, and more valuable than ever.

How Core Analytics Methodologies Work

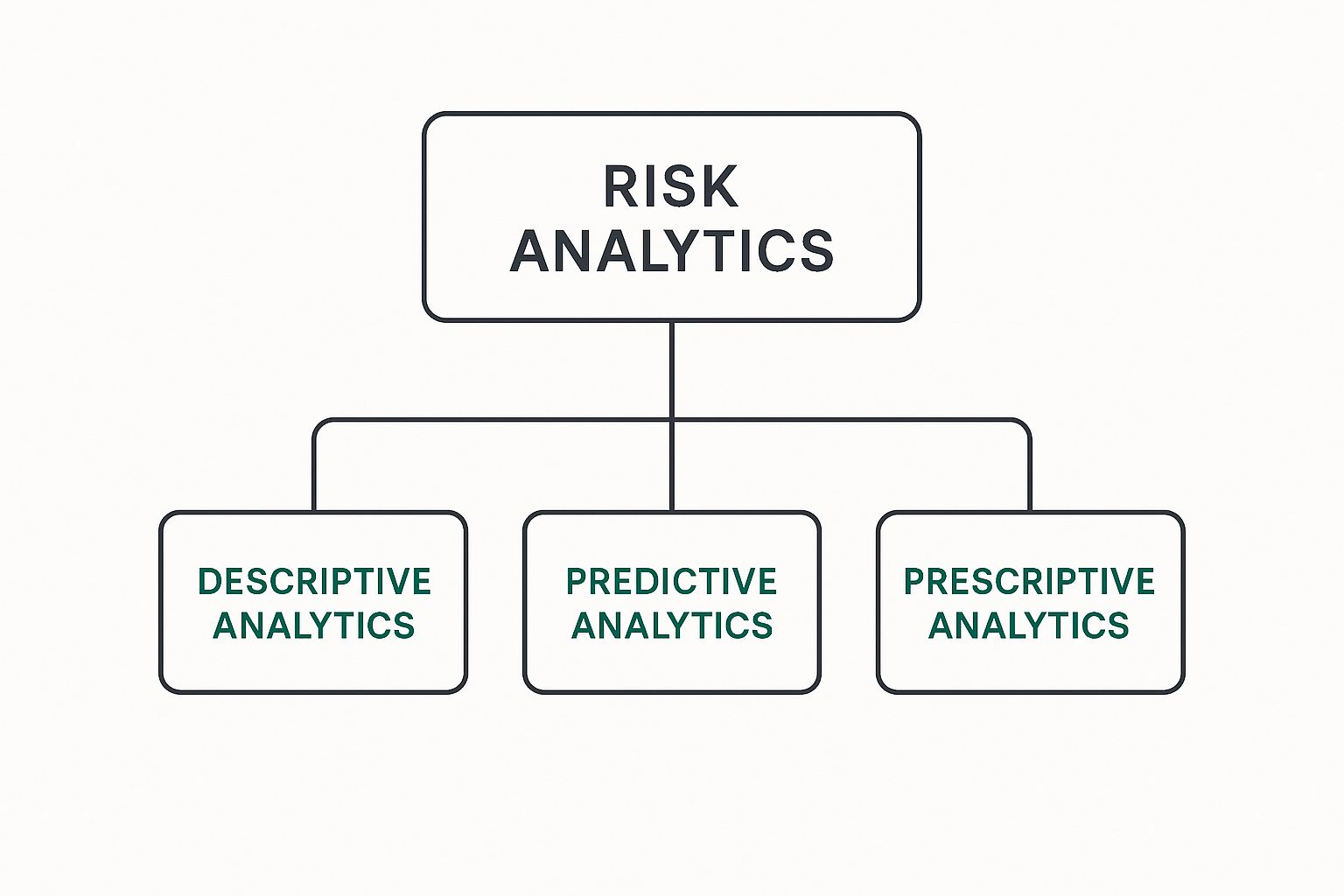

To really get a handle on risk and analytics, you need to peek under the hood at the core methods that drive modern insurance decisions. These aren't just abstract theories; they're practical tools that work together, each building on the last to paint a complete picture of risk. Think of them as three different, yet connected, ways of looking at your data.

This infographic breaks down this hierarchy perfectly, showing how we move from understanding the past to actively shaping the future.

As you can see, everything starts with a solid foundation of descriptive analytics, which then allows for the more powerful predictive and prescriptive insights.

Descriptive Analytics: The What

Descriptive analytics is the bedrock of all risk analysis. It’s all about answering a simple, fundamental question: “What has happened?” This involves digging into historical data to summarize it, spot patterns, and track key metrics.

Imagine a ship's captain poring over the logbooks from past voyages. Those logs reveal the fastest routes, where storms hit, and how much fuel was burned. It’s a crystal-clear, factual picture of past performance. It’s incredibly valuable, but it doesn't tell the captain what the weather will be like on the next trip.

In the insurance world, this looks like:

- Claims Reporting: Pulling up a dashboard showing the number of claims filed in Florida right after a major hurricane.

- Customer Segmentation: Figuring out which customer demographics have filed the most auto claims over the last five years.

- Performance Monitoring: Tracking the average time it takes to settle a workers' compensation claim, quarter by quarter.

This historical view is absolutely essential. It’s how you understand your business's performance and create the baseline for every other kind of risk and analytics.

Predictive Analytics: The Why and What Next

Predictive analytics takes things a step further. It asks, "Why did that happen, and what's likely to happen next?" It uses all that rich historical data from descriptive analytics and feeds it into statistical models and machine learning algorithms to forecast future events.

Let's go back to our captain. This is like using years of weather data combined with current atmospheric readings to generate a forecast. The forecast doesn't just state that a storm happened last year; it predicts a 70% chance of rain for tomorrow, giving the captain time to prepare.

Predictive models are fantastic at finding subtle connections in data that a person might easily miss. For instance, a model could discover that customers who bundle their home and auto policies and regularly log into the client portal are significantly less likely to shop around at renewal time.

This is a game-changer for insurers. It allows them to get a much deeper understanding of data analytics for insurance, shifting their posture from reactive to proactive. They can model potential losses from an upcoming storm or pinpoint which policyholders are most likely to let their coverage lapse.

Prescriptive Analytics: The What to Do

This is the most advanced stage, and it answers the most important question of all: “So, what should we do about it?” Prescriptive analytics doesn't just predict an outcome; it recommends specific, concrete actions to either achieve a goal or sidestep a future risk.

For our captain, this is the smart GPS. It doesn't just warn of the storm ahead; it automatically calculates and suggests a new, safer route to avoid it completely, factoring in the optimal speed and course corrections. It provides a clear, actionable plan.

This is where risk and analytics truly delivers its biggest punch. For example, if predictive models flag a commercial property as having a high fire risk because of its age and outdated electrical system, prescriptive analytics might recommend specific actions—like installing a new sprinkler system—to lower that risk, which in turn could justify a lower premium.

This proactive guidance is fueling massive industry growth. The risk analytics market jumped from $37.12 billion to $41.67 billion in just one year and is on track to hit $73 billion soon. This surge is driven by the demand for tools that don't just show problems but offer solutions. You can read the full research about this market growth to see just how much real-time data is shaping the industry.

The Technology Driving Modern Risk Analysis

The sophisticated analytics methods we've covered aren't just theory. They're powered by very real, practical technology that turns mountains of raw data into sharp, actionable insights. To truly get a handle on modern risk and analytics, you have to understand the tools that make it all happen. These aren't just industry buzzwords; they are the engines making proactive risk management a reality for insurers today.

At the heart of it all are artificial intelligence (AI) and machine learning (ML). The best way to think about them is as incredibly advanced pattern-recognition engines. They can sift through immense datasets and spot subtle connections that a human analyst could spend a lifetime trying to find—and still miss.

For example, an ML model can chew through thousands of past property claims. In doing so, it might uncover a previously unknown link between a specific type of roofing material, local weather patterns, and the proximity to certain tree species that, together, dramatically spike the odds of a claim. That's the kind of deep, granular insight that elevates risk analysis from educated guesswork to genuine data science.

Artificial Intelligence and Machine Learning in Action

AI and machine learning are the brains of the operation, constantly learning from new data to get smarter. They’re already running some of the most critical functions in the insurance world.

- Fraud Detection: AI algorithms are brilliant at spotting anomalies. They can instantly flag a claim that deviates from normal patterns—like multiple claims filed from the same address in a short time or claims with clashing descriptions—letting investigators focus their efforts where it matters most.

- Predictive Underwriting: ML models analyze an applicant’s complete data profile to forecast their future risk with surprising accuracy. This leads to premium pricing that is both fairer and more precise.

- Automated Claims Processing: Simple, low-risk claims can be handled from start to finish by an AI system. This means faster payouts and happier customers, while your human adjusters are freed up to tackle the more complex cases.

These systems are quickly becoming indispensable. The global market for risk and analytics was valued at USD 32.25 billion and is expected to hit USD 51.34 billion within five years, growing at a compound annual rate of 9.7%. Much of that growth is fueled by insurers adopting AI and ML to fight fraud and navigate tricky regulations. You can see the full market breakdown on marketsandmarkets.com.

The Power of Big Data Platforms

If AI is the brain, then Big Data is the library it studies—an enormous, ever-expanding collection of information. Insurers today aren't just looking at application forms and past claims. Big Data platforms pull in and make sense of information from a dizzying array of sources to paint a complete, real-time picture of risk.

Some of these sources include:

- Telematics Devices: In-car sensors that report on speed, braking habits, and mileage.

- IoT Sensors: Smart home and building devices that can detect a water leak or fire hazard before it becomes a catastrophe.

- Satellite Imagery: High-resolution photos used to assess property risks like wildfire or flood exposure.

- Social Media and News Feeds: Publicly available data that can give early warnings about emerging risks or widespread events.

This fusion of diverse data turns risk analysis from a static, outdated snapshot into a live, streaming video. It provides the crucial context needed for genuinely accurate predictions.

Cloud Computing: The Great Equalizer

Not too long ago, the sheer computing power required for this kind of analysis was a luxury reserved for the biggest global insurance corporations. Running Big Data platforms and AI models demanded massive, costly data centers built on-site. This was a huge barrier for small and mid-sized agencies.

Cloud computing changed all of that. It gives any insurer on-demand access to world-class computing infrastructure without the crippling upfront investment. This has been a game-changer, leveling the playing field and allowing insurers of all sizes to tap into the same powerful tools.

By moving to the cloud, an insurer can scale its resources up or down in an instant, only paying for what it actually uses. That kind of agility is essential for staying competitive. To see how these technologies fit into the broader landscape, you can learn more about overarching insurance industry technology trends in our detailed guide. Together, AI, Big Data, and the cloud have become the trio that defines modern insurance.

Of course. Here is the rewritten section, designed to sound like it was written by an experienced human expert.

Practical Applications Across the Insurance Industry

Let’s move beyond the theory. The real magic happens when these powerful analytics tools are put to work in the day-to-day operations of an insurance company. It’s one thing to talk about models and algorithms, but it's another to see them actively reshaping core functions—transforming them from educated guesswork into data-driven precision.

https://www.youtube.com/embed/PmXS5ir3Snc

This isn’t about just one department getting a new piece of software. Risk analytics is being woven into the very fabric of underwriting, claims, and even customer service. The results? Tangible business outcomes and a much better experience for policyholders.

Hyper-Personalized Underwriting and Pricing

The old way of doing things—lumping customers into broad, generic risk pools—is on its way out. It was a blunt instrument. Today, analytics lets us get far more granular, creating underwriting that’s as unique as the person or asset being insured. This leads to a much fairer system where your premium actually reflects your specific risk, not just your zip code.

Take property insurance, for example. Insurers are now blending high-resolution satellite imagery with real-time weather feeds and historical wildfire data. An analytics model can look at a single home and assess its unique wildfire exposure based on things like:

- The type of vegetation surrounding the property.

- The slope of the land it’s built on.

- Its exact distance from known high-risk fire zones.

This detailed view gives underwriters a massive advantage. They can proactively warn homeowners of immediate danger, giving them time to react. A homeowner who has diligently cleared brush and created a defensible space around their house can be rewarded with a lower premium—because the data proves they are a lower risk. It also means insurers can price policies with confidence, rather than issuing blanket denials for entire regions.

We're seeing the same shift in auto insurance, thanks to telematics. Instead of just relying on age and driving records, insurers can use data from a smartphone app or a small device in the car. They analyze actual driving behaviors—like speed, how hard someone brakes, and the times of day they’re on the road—to offer usage-based insurance (UBI). It’s simple: if you drive safely, you pay less. The cost is directly tied to your actions.

Smarter and Faster Claims Processing

Let's be honest: the claims process has always been a major headache for everyone involved. It was slow, buried in paperwork, and often frustrating. Analytics is completely overhauling this experience by automating the straightforward stuff and freeing up human experts to handle the complex cases.

When a claim comes in, an AI-powered system can review it instantly. It checks the claim details against the policy, historical data, and even external sources like weather reports or police records.

A legitimate, clear-cut claim can be fast-tracked for immediate approval and payment, sometimes in a matter of minutes. This is a game-changer for customer satisfaction, especially during a stressful time, and it drastically cuts down on administrative costs.

At the same time, these systems are incredibly good at spotting red flags that might point to fraud. A model could flag a claim if the described damage doesn't match the event (e.g., severe flood damage reported on a sunny day) or if the claimant has a history of suspicious filings. These flagged claims are then sent directly to specialized human investigators for a closer look.

This dual approach—fast-tracking the simple, investigating the suspicious—is a win-win. It boosts efficiency, stops fraudulent payouts, and builds trust by paying legitimate claims quickly. Allocating resources this precisely is also a cornerstone of a smart business strategy. You can dive deeper into this by conducting a detailed insurance gap analysis to pinpoint where your own processes could be strengthened.

To see how this works across the board, let's look at a few examples.

Risk Analytics Applications Across Insurance Functions

This table illustrates how different risk analytics methodologies are applied to core functions within an insurance company to achieve specific business outcomes.

| Insurance Function | Analytics Application | Primary Business Benefit |

|---|---|---|

| Underwriting | Predictive models analyze applicant data to forecast future loss potential. | More accurate pricing, reduced adverse selection, and improved profitability. |

| Claims | Anomaly detection algorithms screen incoming claims for fraudulent patterns. | Lower fraud losses, faster processing for legitimate claims, and reduced overhead. |

| Marketing | Customer segmentation models identify high-value or at-risk policyholders. | Increased customer retention, effective cross-selling, and higher ROI on campaigns. |

| Product Development | Market trend analysis identifies emerging risks and coverage gaps. | Creation of relevant new products that meet evolving customer needs. |

| Capital Management | Catastrophe modeling (CAT) simulates the financial impact of large-scale events. | Better-informed reinsurance decisions and enhanced solvency protection. |

As you can see, analytics isn't just one tool; it's a versatile toolkit that can be applied to virtually every part of the insurance lifecycle.

Enhancing Customer Experience and Retention

At the end of the day, insurance is a relationship business. The ultimate goal is to keep customers happy and loyal. Here, risk and analytics provides the insights needed to anticipate customer needs and make every interaction feel personal and relevant.

Predictive models can now identify policyholders who are at a high risk of leaving at renewal time. By looking at signals like recent life events (buying a home, having a child), past customer service calls, or even how often they log into the company portal, an insurer gets an early warning.

This allows them to be proactive. Instead of waiting for the customer to shop around, they can reach out with a personalized offer, a courtesy coverage review, or a simple check-in call. It's about demonstrating value and strengthening that relationship before it's ever at risk.

The Strategic Benefits of Adopting Risk Analytics

Making a big investment in a new operational model is never a small decision. For any insurer thinking about this, the "why" behind embracing risk and analytics boils down to a powerful chain of advantages that ripple through the entire business. We're talking about more than just a little efficiency boost; it's about building a smarter, more resilient, and ultimately more profitable company from the inside out.

This isn't just about tweaking old processes. It’s about unlocking capabilities that legacy systems and gut-feel methods simply can't deliver. The best part? These benefits are all connected, each one making the others stronger and creating a powerful competitive edge.

Let's dive into what those specific advantages look like in the real world.

Gaining Precision in Decision-Making

At its heart, risk and analytics is about swapping out broad assumptions for hard data. This shift leads directly to smarter, more profitable decisions everywhere, but it truly shines in the make-or-break areas of underwriting and pricing.

Think about pricing a complex commercial liability policy. The old way meant leaning on generalized industry data and broad risk categories, which often left a lot of room for error. Now, with advanced analytics, an underwriter can model a specific company’s risk profile with incredible detail. The result is pricing that truly reflects the actual exposure, dramatically cutting the odds of a surprise catastrophic loss down the road.

This is a complete game-changer. Instead of just hoping the premiums coming in will be enough to cover claims going out, insurers can set prices with a high degree of confidence, directly fueling a healthier bottom line.

Achieving Superior Operational Efficiency

Another massive strategic win is automating the repetitive, high-volume tasks that clog up the works. Doing so doesn't just cut operational costs—it frees up your most valuable resource: your people. This is especially clear when you look at the claims process.

For example, a huge part of claims verification can be automated. An analytics system can instantly check a new claim against the policy details, external data like weather reports, and known fraud patterns. Simple, legitimate claims get paid out in hours, not weeks. This lets your experienced adjusters pour their energy into the complex, nuanced cases where human judgment is irreplaceable.

This blend of speed and focused expertise is a potent one-two punch. It drives down administrative costs while making the customer experience worlds better—a leaner, more effective operation all around.

This push for operational excellence is a major reason the global risk analytics market is exploding. Projections show it growing from around USD 39.0 billion to an estimated USD 116.3 billion within the decade. As you can discover more insights about this market growth on imarcgroup.com, it's a clear sign of the incredible value insurers are finding.

Securing a Lasting Competitive Advantage

Maybe the most powerful benefit of all is the ability to consistently outmaneuver the competition. Insurers who truly master risk and analytics can innovate faster, confidently step into new markets, and create products that others simply can't replicate.

Take the rise of on-demand or parametric insurance. These policies—which pay out automatically when a specific trigger occurs, like an earthquake hitting a certain magnitude—are only feasible with sophisticated data feeds and real-time analytical muscle. Old-school systems just weren't built for that kind of agility.

This ability creates a self-reinforcing cycle of growth. Launching innovative products attracts new types of customers. The data from those new policies is then fed back into your analytics models, making them even smarter and widening your competitive lead. This is a core theme in the broader digital transformation in insurance, where technology becomes the engine for market leadership.

Common Questions About Insurance Risk Analytics

As insurers start digging into the world of risk and analytics, a lot of practical questions naturally pop up. Moving from theory to practice can feel like a huge jump, but it doesn't have to be. Let's tackle some of the most common concerns to help clear a path for anyone ready to embrace a more data-informed strategy.

Many leaders, especially at smaller or mid-sized firms, get hung up on the idea that analytics requires a massive, bank-breaking investment. While a full-scale overhaul can be expensive, the smart play is often to start small. The trick is to pick one specific, high-impact business problem and solve it first.

For example, instead of trying to reinvent your entire claims process overnight, you could focus on a single, measurable issue, like flagging potential soft fraud in auto-glass claims. This kind of targeted project lets you prove the value of analytics with a manageable scope and budget. With so many cloud-based tools and pay-as-you-go software options available today, powerful analytics are more accessible than ever, no huge capital investment required.

What Are the Biggest Hurdles to Adoption?

You might think technology is the biggest roadblock, but it’s almost never the case. The real challenges are almost always about people and processes. A successful analytics program is about more than just software—it demands a cultural shift where data isn't just collected, but is actually trusted and used to guide decisions from the top down.

The main obstacles usually boil down to these four things:

- Data Silos: Critical information is often locked away in different departmental systems that don't talk to each other. Getting that data to flow freely is the essential first step.

- Legacy Systems: Old, rigid technology can make it a real headache to plug in modern analytical tools.

- Skills Gap: You might not have people in-house with the right expertise to build, manage, and interpret complex data models.

- Resistance to Change: Let's be honest, people get comfortable with the way things have always been done. Employees might be hesitant to trust and adopt new workflows driven by data they don't fully understand yet.

Getting past these hurdles takes strong leadership, clear communication about the "why," and a real investment in training your team. It's also worth remembering that the risk of strategic management without good data is far greater than the challenges of adopting it. You can take a closer look at navigating the risk of strategic management to see how analytics directly counters these high-level threats.

How Analytics Helps With Compliance

The regulatory environment is a moving target, and just keeping up can feel like a full-time job. This is where modern risk and analytics becomes a game-changer, giving you the tools to stay ahead of the curve. Analytics platforms can run in the background, continuously checking transactions and operations against regulatory rules and automatically flagging anything that looks suspicious for a human to review.

This process creates an automated, fully auditable trail that proves your due diligence to regulators. When new regulations come down the pike, you can simply update the models to ensure you remain compliant. It turns a reactive, stressful chore into a proactive strength.

This forward-looking approach does more than just help you avoid costly fines; it builds a foundation of trust with both regulators and your clients. It shifts compliance from being a necessary evil to a genuine strategic advantage that reinforces the integrity of your entire operation.

At Wexford Insurance Solutions, we bring together deep industry experience and powerful analytics to help our clients manage risk with confidence. Whether you're looking to protect your family or your business, we deliver clear insights and solid coverage. Contact us today to see how we can help you build a more secure future.