Let's get one thing straight from the jump: "full coverage" isn't an actual insurance product you can just buy off a menu. It’s more like a common nickname for a specific combination of coverages that, when put together, create a powerful financial shield for your car.

What Full Coverage Insurance Really Means

So, when someone in the insurance world says "full coverage," they're using industry slang. It’s a convenient way to describe a policy that includes not just the legally required stuff, but also protection for your own vehicle. You won't see "Full Coverage Policy" printed on your official documents.

Think of it like ordering a "combo meal" instead of just a sandwich. The sandwich alone is fine, but the combo gives you the fries and a drink, too—it’s a more complete package. In the same way, full coverage bundles together different insurance types to cover a much wider range of potential problems.

Core Components of a Full Coverage Policy

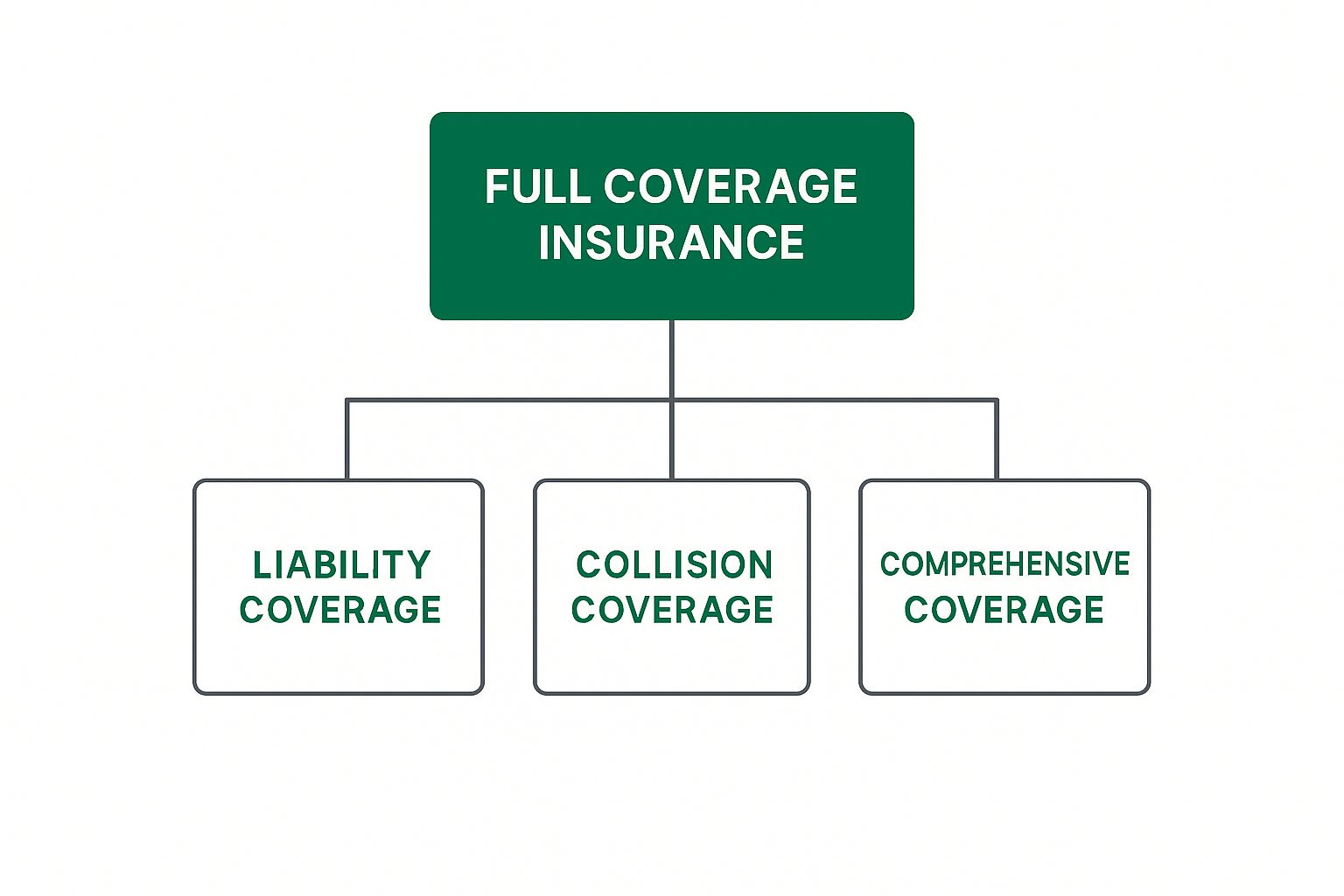

So what's actually in this bundle? It's built on three essential parts that work in tandem. This combination is what sets it apart from a bare-bones liability policy that only covers damage you cause to others.

Let's break down these three foundational pieces.

Core Components of a Full Coverage Policy

| Coverage Type | What It Covers |

|---|---|

| Liability Coverage | Pays for injuries and property damage you cause to other people in an at-fault accident. It doesn't cover your car or your own injuries. |

| Collision Coverage | Pays to repair or replace your own vehicle after a collision with another car or an object (like a pole or fence), regardless of who was at fault. |

| Comprehensive Coverage | Pays for damage to your own vehicle from non-collision events, such as theft, vandalism, fire, hail, floods, or hitting an animal. |

Essentially, liability protects others from you, while collision and comprehensive protect you from just about everything else.

Key Takeaway: Full coverage isn’t a single policy. It’s a trio of coverages—Liability, Collision, and Comprehensive—that provides financial protection for damage to others and to your own car from a whole host of incidents.

Why Lenders Insist On It

If you have a loan or lease on your vehicle, you can bet your lender or leasing company will require you to carry full coverage. The reason is simple: they own a piece of your car until it's paid off, and they need to protect their investment.

If your car gets totaled in a crash or stolen, they want to ensure the money is there to cover the outstanding loan balance. This requirement is so common that 73% of new car buyers carry a full coverage policy. They recognize it as a vital safety net for their new asset.

While the basic idea of full coverage is consistent, certain vehicles have unique needs, like special classic car insurance requirements. For the vast majority of drivers with a financed car, though, this three-part bundle is the gold standard for proper protection.

The Three Pillars of Full Coverage Insurance

So, you’ve heard the term "full coverage," but what does it actually mean? It’s not a single insurance product you can buy off the shelf. Instead, think of it as a bundle of different coverages that work together to create a strong financial safety net.

I often explain it to my clients like a three-legged stool. For it to be stable and support you when you need it most, you need all three legs: Liability, Collision, and Comprehensive. Each one protects you from a different kind of risk.

Let's break down what each of these pillars does for you. The image below gives you a great visual of how they combine to form a solid full coverage policy.

As you can see, Liability, Collision, and Comprehensive are the core building blocks. Without all three, your protection is incomplete.

Pillar 1: Liability Coverage

This is the one part of the trio that’s almost always required by law. Liability coverage is your financial defense if you're responsible for an accident. Its job is simple but absolutely critical: to pay for the injuries and property damage you cause to other people.

It’s important to realize this doesn't cover your own car or your own medical bills. It’s there to protect you from being sued and having your personal assets at risk.

Liability insurance is broken down into two main parts:

- Bodily Injury Liability (BI): This covers the medical bills, lost income, and even pain and suffering for the other driver and their passengers when you're at fault.

- Property Damage Liability (PD): This pays to fix or replace the other person's vehicle or any other property you might have damaged, whether it's a mailbox or a storefront.

Imagine you misjudge a turn and clip another car. Your liability coverage is what steps in to handle the other driver’s repair bills and any medical treatment they need, keeping you from having to pay those potentially massive costs yourself.

Pillar 2: Collision Coverage

While liability takes care of the other party, collision coverage is what protects your vehicle. This is the part of your policy that pays to repair or even replace your own car after it's been damaged in a crash with another vehicle or an object, like a pole or a guardrail.

The best part? It applies no matter who was at fault. So, whether you caused the accident or were the victim of a hit-and-run, collision coverage is there to get your car back on the road.

A Quick Word on Deductibles: When you make a collision claim, you’ll first have to pay your deductible. For example, if your deductible is $500 and the repairs cost $4,000, you pay the first $500 and the insurance company handles the remaining $3,500. A higher deductible usually means a lower premium, but it also means you'll have a higher out-of-pocket cost if you need to file a claim.

Pillar 3: Comprehensive Coverage

The final piece of the puzzle is comprehensive coverage. I like to call it the "life happens" coverage because it protects your car from just about everything else besides a collision.

Think of comprehensive as your shield against all the unpredictable, non-driving-related mishaps:

- Theft or vandalism

- Fire, floods, wind, and hail

- A tree branch falling on your roof

- Hitting a deer or other animal

- A cracked windshield or shattered glass

So, if a hailstorm leaves your car looking like a golf ball or you walk outside to find your car stolen, this is the coverage that makes you whole again. It handles the strange, unexpected events that are completely out of your control.

Understanding how these pillars stand on their own is key, but it's also helpful to know they can function differently depending on the policy type, like in the case of commercial vs. personal auto insurance.

Customizing Your Policy with Optional Coverages

While Liability, Collision, and Comprehensive coverages are the heavy hitters of your auto policy, they don't account for every risk you might face. Think of them like the standard features on a car—they get you from A to B safely, but the optional upgrades are what add true comfort and security. That’s exactly what optional insurance coverages do: they fill in the gaps for a truly comprehensive safety net.

These add-ons let you build a policy that fits your life, not the other way around. For some folks, they're essential for total peace of mind. For others, they might be less critical. The key is knowing what’s available so you can decide what makes sense for you.

Protecting Yourself From Irresponsible Drivers

One of the biggest frustrations on the road? Dealing with the fallout from drivers who don't carry enough—or any—insurance. It's a shocking but true statistic: roughly one in eight drivers on U.S. roads is uninsured. This is where a vital optional coverage steps in.

Uninsured/Underinsured Motorist (UM/UIM) Coverage acts as your financial shield when you're in an accident caused by someone with no insurance (uninsured) or too little insurance (underinsured) to pay for your damages. Without it, you could be stuck with the bill for your own medical care and car repairs, even when the accident wasn't your fault.

This coverage usually has two components:

- Uninsured Motorist Bodily Injury (UMBI): This helps pay the medical bills for you and your passengers if you're injured by an uninsured driver.

- Uninsured Motorist Property Damage (UMPD): This covers the repairs to your car if it's damaged by an uninsured driver.

Adding UM/UIM coverage is like having a specific backup plan for when other drivers don't follow the rules.

Covering Your Own Medical Bills Immediately

After an accident, waiting for insurance companies to decide who was at fault can be a slow, agonizing process—especially when medical bills are piling up. Fortunately, two coverages are designed to cut through the red tape and get you paid quickly, no matter who caused the crash.

Key Insight: Medical Payments and Personal Injury Protection are often called "first-dollar" coverages because they kick in immediately to cover your initial expenses. You don't have to wait for the at-fault party's insurance to pay out.

Medical Payments Coverage (MedPay) is pretty straightforward. It helps pay for medical or funeral expenses for you and your passengers after an accident, regardless of fault. This can cover things like your health insurance deductible, doctor visits, and hospital co-pays.

Personal Injury Protection (PIP) is a more expansive version of MedPay and is actually required in some states. On top of medical bills, PIP can also cover other costs that arise from your injuries, like lost wages if the accident leaves you unable to work or money to hire help for household chores you can no longer do.

Add-Ons for Everyday Convenience

Beyond major accidents, a few other optional coverages can save you from the smaller, but still significant, headaches of car ownership. These are the little upgrades that you'll be incredibly thankful for when you need them.

Consider these popular choices:

- Rental Reimbursement: If your car is laid up in the shop after a covered accident, this pays for a rental car. It’s a lifesaver that keeps your daily routine from grinding to a halt.

- Roadside Assistance: This coverage is your go-to for frustrating but common problems. It typically covers services like towing, jump-starting a dead battery, changing a flat tire, or even delivering gas if you run out.

By carefully choosing the right add-ons, you can elevate your policy from a standard "full coverage" package to one that's truly built for your car, your budget, and your life.

Breaking Down the Cost of Full Coverage

So, you understand what full coverage is and how it protects you. That’s one piece of the puzzle. The other, of course, is what it's going to cost you. There's no single, one-size-fits-all price tag for a full coverage policy. Instead, the final premium you pay is a carefully calculated number based on a whole host of factors—some you can control, and some you can't.

Think of it this way: an insurance company is trying to figure out how much risk you represent. The higher the perceived risk, the higher your premium will be. Let's get into the specifics of what they're looking at.

Key Factors That Shape Your Premium

Every insurance carrier has its own unique recipe for calculating rates, but they all start with a similar set of ingredients. These are the core data points they use to build your personal risk profile.

Here are the biggest factors that will directly influence your quote:

- Your Driving Record: This is the big one. If you have a history of at-fault accidents, a collection of speeding tickets, or a DUI on your record, insurers will see you as more likely to file a claim in the future. That means a higher premium.

- The Vehicle You Drive: The car itself matters—a lot. A brand-new luxury SUV or a high-performance sports car with expensive, specialized parts is going to cost far more to insure than a sensible, older sedan. It all comes down to the potential cost of repairs or replacement.

- Your Location: Where you park your car at night has a surprisingly large impact on your rates. Insurers use local statistics on theft, vandalism, and accident frequency. If you live in a dense urban area with a high rate of claims, you'll likely pay more than someone in a quiet, rural zip code.

- Your Credit History (in most states): This might seem unrelated, but many insurers use a credit-based insurance score to predict the likelihood of future claims. Statistics show that people with higher credit scores tend to file fewer claims, which often earns them lower rates.

These elements are combined to create a risk profile that's unique to you. The same principles apply to businesses, too, though you can dive deeper into that on our page explaining business auto insurance costs.

Taking Control of Your Insurance Costs

While you can’t change your driving history overnight or move to a new zip code just for cheaper insurance, you absolutely have control over two of the most powerful levers that determine your premium: your deductibles and your coverage limits.

A deductible is simply the amount you agree to pay out-of-pocket for a claim before your insurance company steps in.

Choosing a higher deductible is a straightforward trade-off. It lowers your monthly premium because you're agreeing to take on more of the initial financial risk yourself. For example, bumping your collision deductible from $500 to $1,000 could significantly reduce what you pay each month.

Similarly, your coverage limits—the maximum amount your policy will pay for a claim—also play a big role. Opting for higher liability limits gives you much better financial protection if something serious happens, but it will also nudge your premium upward. The goal is to find that sweet spot between what you can afford monthly and what you could realistically cover out-of-pocket if you had to file a claim.

The good news is that your personal details aren't the only thing at play; broader market conditions also have an effect. For instance, the average monthly premium for full coverage in major U.S. markets hovered around $150–$200 as of early 2025. This figure, pulled from the 2025 Insurance Market Report from Gallagher, reflects how healthy competition among insurers can help keep rates in check. It’s a good reminder that while your profile is key, industry dynamics are also working behind the scenes.

Deciding If Full Coverage Is Right for You

Choosing the right amount of car insurance often feels like a balancing act. On one hand, you want ironclad financial protection. On the other, you have to work within a monthly budget. The big question is: is full coverage a smart investment for you, or is it an unnecessary expense you could cut?

There's no single right answer. It all comes down to your unique situation—your car, your finances, and frankly, how much risk you’re comfortable taking on yourself. Let’s walk through the key scenarios to help you make a confident, clear-headed decision.

When Full Coverage Is Non-Negotiable

For a lot of drivers, the decision is already made for them. In certain situations, carrying a full coverage policy—meaning one that includes both Collision and Comprehensive—isn't a choice, it's a requirement. This isn't about state law; it’s about protecting a lender's financial stake in your vehicle.

You will almost certainly be required to have full coverage if you:

- Have a Car Loan: When you finance a vehicle, the bank or credit union technically owns it until you’ve paid off the loan. To protect their investment, they’ll require you to keep it fully insured against damage or theft.

- Lease Your Vehicle: It’s the same story with a lease. The leasing company owns the car, and your lease agreement will state that you must carry collision and comprehensive coverage for the entire term.

In these cases, dropping full coverage is a breach of contract. The lender could even buy an expensive policy for you and tack the cost onto your loan payments. It’s a requirement you can't sidestep.

The Strategic Choice for Full Coverage

Even if you own your car outright with no lender involved, choosing full coverage can still be an incredibly wise financial move. The decision really boils down to one simple question:

If your car was totaled tomorrow, could you afford to replace it without facing a major financial crisis?

Think of full coverage as a tool to protect the value of your asset. You’re essentially transferring the risk of a huge financial hit from your shoulders to the insurance company.

Consider these factors:

- Your Car's Value: Is your car new or just a few years old? A bad accident could erase thousands of dollars in value in an instant. Full coverage protects that investment.

- Your Savings: Do you have enough cash set aside to buy a replacement vehicle or handle a multi-thousand-dollar repair bill? If the answer is no, full coverage is your safety net.

- Your Peace of Mind: How much is worry-free driving worth to you? Just knowing you’re covered for theft, a collision, or a freak hailstorm can be worth the premium alone. This is especially true for businesses, which have to manage risk across all operations. Exploring the details of commercial insurance in New York highlights just how crucial this kind of risk management is on a larger scale.

Full Coverage Decision Guide

To make things even clearer, use this quick guide. Find the situation that best matches yours to see a recommendation.

| Your Situation | Is Full Coverage Recommended? | Primary Reason |

|---|---|---|

| You are financing or leasing a vehicle. | Yes, it's almost always required. | Your lender or leasing company needs to protect their financial investment in the car. |

| Your car is new or worth more than $5,000. | Strongly Recommended. | The cost to repair or replace your vehicle would be a significant financial burden. |

| You don't have enough savings to replace your car. | Strongly Recommended. | Full coverage acts as a critical financial safety net against unexpected, high costs. |

| Your car is old, has a low value, and you have savings. | Probably Not. | The annual premium may cost more than the car is worth, offering poor value. |

| You want maximum peace of mind on the road. | Recommended. | The emotional and financial security can be well worth the additional premium. |

This table is a starting point, but it helps frame the decision around what matters most: protecting your finances and assets.

Knowing When to Consider Dropping It

As your car gets older and its value drops, the math behind keeping full coverage starts to shift. Eventually, you’ll reach a point where the cost of the insurance may be more than the potential payout.

A handy rule of thumb is the “10% Rule.” Here’s how it works:

- Find your car’s current Actual Cash Value (ACV). You can get a solid estimate from sites like Kelley Blue Book or Edmunds.

- Figure out your annual premium for only the collision and comprehensive parts of your policy.

- Compare the two figures.

If your annual premium for these coverages is more than 10% of your car's value, it might be time to think about dropping them. For instance, if your car is worth $4,000 and you're paying $500 a year for collision and comprehensive, that’s 12.5% of its value. At that stage, you’re paying a lot to protect a low-value asset. You might be better off banking that premium money for future repairs or a down payment on your next car.

Finding the Best Value on Your Policy

https://www.youtube.com/embed/frSZGLaXTUM

Alright, so you've decided full coverage is the right move. The next challenge is finding a great policy that doesn't break the bank. Getting the best value isn't just about chasing the lowest price tag; it's about locking in solid protection at a cost that makes sense for you.

Your most powerful tool here is simple: comparison shopping.

You should never, ever take the first quote you're given. Every insurance company has its own secret sauce for calculating risk, meaning the price for the exact same coverage can swing wildly from one carrier to the next. By gathering quotes from at least three to five different insurers, you get a real sense of the market and can negotiate from a position of strength.

Tapping into Common Discounts

Insurance companies have a ton of discounts available, but here’s the catch—they rarely apply them automatically. You usually have to ask. Before you start calling for quotes, have a list of potential discounts ready so you don’t leave any money on the table.

Here are some of the most common ones to ask about:

- Multi-Policy Bundles: This is often the biggest and easiest discount to get. If you have homeowners or renters insurance, ask about bundling it with your auto policy.

- Safe Driver Programs: A clean driving record makes you a much lower risk to insure, and most companies will reward you for it. Don't forget to ask about telematics programs, too—these use a simple smartphone app to monitor your safe driving habits for even more savings.

- Good Student Rates: If a young driver on your policy keeps a “B” average or higher, you could see a nice drop in your premium.

- Loyalty Rewards: Sticking with the same insurer for a few years can sometimes earn you a discount. Just make sure you weigh that loyalty reward against what you could save by switching to a competitor.

Digging into all the available discounts is a crucial step. For drivers in certain states, local knowledge can unlock even more savings. For instance, our guide to finding affordable car insurance in Florida dives into tips specific to the Sunshine State market.

Adjusting Deductibles and Limits

Beyond discounts, you have direct control over your premium by tweaking your deductibles and coverage limits. It's like a seesaw: a higher deductible (the amount you pay out-of-pocket on a claim) will directly lower your monthly premium.

Pro Tip: A good rule of thumb is to choose the highest deductible you could comfortably pay tomorrow without causing a financial crisis. Just bumping your deductible from $500 to $1,000 can create significant savings over the course of a year.

Of course, this is a balancing act between saving money now and being prepared for a potential claim later. It’s all about finding that sweet spot where you feel protected without overpaying for it. By managing these moving parts, you can craft a policy that delivers real value and, more importantly, peace of mind.

Common Questions About Full Coverage Insurance

Even after we've broken down all the pieces, a few questions about full coverage seem to pop up time and time again. Let's tackle these common points of confusion head-on so you have a crystal-clear picture of how this policy works in the real world.

Is Full Coverage Insurance Required by Law?

This is easily one of the most frequent questions we hear, and the answer is a straightforward no. No state in the U.S. legally mandates that you carry something called "full coverage." State laws are only concerned with minimum liability insurance—the coverage that pays for damage you cause to other people and their property.

However, the requirement often comes from another place entirely. If you have a loan or a lease on your car, your lender will almost certainly require you to carry both Collision and Comprehensive. Why? They need to protect their financial stake in your vehicle until you've paid it off.

So, while it's not a state law, it's very often a contractual obligation you agreed to when you financed the car.

Does Full Coverage Mean Everything Is Covered?

The name "full coverage" is a bit of a misnomer, and frankly, it can be misleading. It doesn't mean your policy is an invincible shield that covers every single thing that could possibly go wrong. It’s simply an industry term for a specific bundle of protections.

For instance, a standard full coverage policy won't cover:

- Normal Wear and Tear: Things like worn-out tires or aging brake pads are considered routine maintenance, not damage you can file a claim for.

- Mechanical Breakdowns: If your engine seizes or the transmission fails, that’s not something your auto insurance is designed to handle.

- Personal Belongings: Let's say a thief smashes your window and steals your laptop. The window is covered by your auto policy, but the laptop itself falls under your homeowners or renters insurance.

This idea of bundling liability with physical damage protection has become a global standard, driven by what consumers need to feel financially secure. You can actually read more about these trends and consumer demands in the 2025 insurance market report. Understanding these lines in the sand is crucial for managing expectations and seeing where you might need other policies, like those detailed in our guide to homeowners insurance.

Will My Policy Pay for a Rental Car?

Here's another classic pitfall. A standard full coverage package does not automatically include a rental car while yours is being repaired after an accident.

To get your rental car expenses covered, you have to specifically add rental reimbursement coverage to your policy. It's an optional add-on, but it's usually inexpensive and offers huge value by keeping you on the road without racking up big out-of-pocket costs.

The takeaway here is simple: never assume something is included. Always check your policy declarations page or chat with your agent to be sure about what optional coverages you have.

Figuring out the ins and outs of insurance can feel complicated, but you don't have to go it alone. The experts at Wexford Insurance Solutions are here to give you clear, straight answers and help you build a policy that truly protects what matters most. Visit us online to get started with a personalized quote today!