If you use a vehicle for your business, you need more than just standard car insurance. Commercial auto insurance is a specific type of policy built to cover the unique risks and liabilities that come with using vehicles for work. It's the professional-grade protection your business needs when its operations are on the move.

What Is Commercial Auto Insurance, Really?

Think of it this way: your personal car insurance is like a basic first-aid kit. It’s great for the minor scrapes you might get driving to the grocery store or a friend's house. But commercial auto insurance? That’s the fully equipped ambulance, ready to handle the complex, high-stakes emergencies that can happen when a vehicle is a core part of your business.

A personal policy is designed for commuting and personal errands. The second you start using a vehicle to transport goods, haul equipment, or drive clients, the entire risk profile changes. Your personal policy simply wasn't built for that.

In fact, most personal policies have specific exclusions for business use. If your employee gets into an accident while running a work errand in their own car, or if your company van is in a collision, your personal insurer will almost certainly deny the claim. That could leave your business on the hook for crippling lawsuits, medical bills, and repair costs.

A single at-fault accident in a work vehicle can trigger liability costs that could wipe out a small company's entire financial foundation. Commercial auto insurance acts as a critical firewall, protecting your business from that kind of catastrophic event.

It's More Than Just Coverage for a Vehicle

The key thing to understand about commercial auto insurance is that it protects your entire business, not just the truck or van. It’s a fundamental piece of your risk management strategy.

These policies are designed to handle the realities of business use, which often means higher liability limits, more miles on the road, and specific risks tied to your industry. Whether you're a solo contractor with one pickup truck, a local restaurant making deliveries, or a consulting firm with a team visiting clients, this coverage is non-negotiable.

The coverage can also get very specific. For instance, a resort or large facility using golf carts to move people and equipment would need something specialized like commercial golf cart insurance to be properly covered. It just goes to show how these policies are adapted for different business realities.

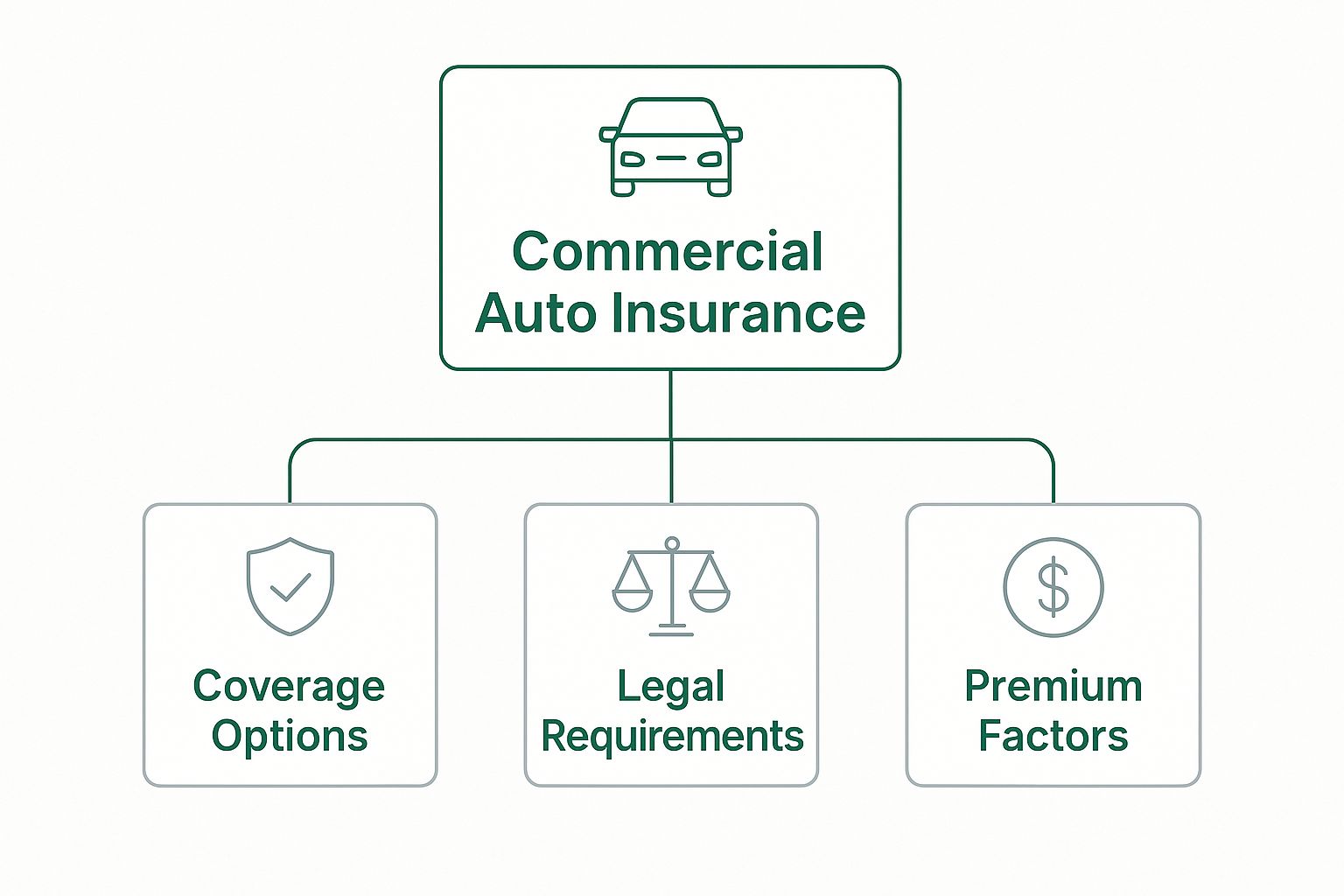

This image breaks down the core components that make up a commercial auto policy, showing how your specific coverage needs, legal requirements, and cost factors all fit together.

As you can see, a solid policy is a careful balance of what you need, what the law demands, and what you can afford.

The growing demand for this coverage tells its own story. The global commercial auto insurance market is expected to hit $276.25 billion by 2030. That’s not just an abstract number—it’s a clear indicator that smart businesses everywhere are making the protection of their vehicles a top priority.

Understanding Your Policy's Core Protections

Cracking open a commercial auto policy can feel like trying to decipher a legal document written in another language. It's packed with industry-specific terms and clauses that spell out exactly when you're covered—and, more importantly, when you’re not.

To really get a handle on commercial auto insurance, you have to break it down into its core components.

Think of it like a mechanic's toolkit. Each type of coverage is a specialized tool designed for a specific job. When something goes wrong on the road, having the right tools makes all the difference. Let's translate these essential protections into plain English so you know exactly what you're buying.

Liability Protection: The Foundation of Your Coverage

Liability coverage is the absolute bedrock of any commercial auto policy. It's the financial shield that protects your business if one of your drivers is at fault in an accident that injures someone or damages their property.

Without it, a single major accident could trigger lawsuits that drain your company’s bank accounts, seize its assets, and potentially shut your doors for good.

The average cost of a fatal vehicle crash is a staggering $1.7 million. That figure accounts for everything from medical bills and lost productivity to legal fees. This is why having robust liability protection isn't just a good idea—it's a fundamental tool for business survival.

This coverage is typically broken down into two main parts:

- Bodily Injury Liability: This pays for costs related to injuries or death that your driver causes to other people. It covers things like medical bills, hospital stays, lost wages, and legal settlements.

- Property Damage Liability: This handles the bill for repairing or replacing someone else's property your driver damages, whether it's their car, a fence, or even a storefront.

This protection is so critical that almost every state legally requires businesses to carry a minimum amount of liability insurance on all registered vehicles.

Physical Damage Coverage: Protecting Your Own Vehicles

While liability coverage deals with the damage you cause to others, physical damage coverage is all about protecting your own fleet. It’s what pays to repair or replace your trucks, vans, or cars when they get banged up. This coverage is usually split into two distinct categories for different kinds of incidents.

First up is Collision Coverage. This one is pretty straightforward. It pays for damage to your vehicle when it collides with another object—be it another car, a guardrail, or a telephone pole. It also covers damage if one of your vehicles flips over. If your delivery van hits a patch of ice and slides into a wall, collision coverage is what pays for the repairs.

Next is Comprehensive Coverage. I like to think of this as protection from almost everything else besides a collision. It covers damage from events that are largely out of your driver's control.

What does that include?

- Theft and vandalism

- Fire, hail, or flooding

- Falling objects, like a tree branch

- Hitting an animal, like a deer on a rural road

So, if your work truck is stolen from a job site overnight, comprehensive coverage is the tool that helps you replace it.

Essential Add-Ons for Complete Protection

A standard policy with liability and physical damage is a solid start, but today's business realities often demand more specialized protection. Several key endorsements, or add-ons, are designed to fill critical gaps that could otherwise leave your company dangerously exposed.

A must-have add-on is Uninsured/Underinsured Motorist (UM/UIM) Coverage. This steps in if your driver is hit by someone who has no insurance at all or not enough to cover the damages. It ensures you aren't stuck paying out-of-pocket for medical bills and vehicle repairs after an accident that wasn't even your fault.

Perhaps one of the most vital endorsements for any modern business is Hired and Non-Owned Auto (HNOA) Coverage. This addresses a massive blind spot: what happens when a vehicle your business doesn't own is being used for work?

HNOA is split into two functions:

- Hired Auto: Provides liability protection when your business rents, leases, or borrows a vehicle for a job.

- Non-Owned Auto: This is the big one. It covers your business's liability if an employee gets into an accident while using their personal vehicle for a work errand, like visiting a client or dropping something off at the post office.

With over 47% of small businesses regularly using employee-owned or rented vehicles, HNOA is no longer a niche add-on; it’s a mainstream necessity. Without it, your company is completely on the hook if an employee runs a "quick errand" in their own car and causes an accident. To see how this fits into the bigger picture, you can explore more about various commercial insurance types in our detailed guide.

Do You Actually Need Commercial Auto Insurance?

This is the million-dollar question for a lot of small business owners. When you hear "commercial vehicle," you probably picture a massive semi-truck or a fleet of branded construction pickups. The truth is, the need for commercial auto insurance pops up in far more common, everyday business activities.

The line between personal and business use can get incredibly blurry. It creates a dangerous gray area where entrepreneurs unknowingly gamble with their company's future. Trying to get by with a personal auto policy for work-related tasks is one of the biggest financial risks you can take. Just one accident during a work-related drive could get your claim denied, leaving your business on the hook for a potentially devastating lawsuit.

Everyday Scenarios That Demand Coverage

Let's look at a few real-world examples. Each of these business owners is using a vehicle in a way that almost certainly requires a commercial policy, even if it’s just a standard family car.

Think about Sarah, a talented florist. Every morning, she loads her personal minivan with gorgeous arrangements for weddings and events. Every single delivery she makes is a business activity. If she gets into a fender-bender on the way to a venue, her personal insurer could flat-out deny the claim because the van was being used for profit.

Now, let's consider David, a real estate agent. He spends his days chauffeuring clients around in his own sedan to look at properties. Transporting people as part of a professional service is a classic trigger for needing commercial coverage. An accident with a client in the car would create a messy liability situation that his personal policy was never built to handle.

Finally, meet Maria, an IT consultant. She uses her SUV to visit client offices, often carrying expensive servers and diagnostic gear in the back. Hauling specialized tools of the trade is a major red flag for personal insurers. Her vehicle is essential to her work, making it a core business asset that needs proper protection.

Identifying the Triggers in Your Business

These stories shine a light on the common triggers that separate personal driving from business operations. The key isn't just the vehicle itself, but how you're using it. If you answer "yes" to any of these questions, it's time to seriously look into commercial auto insurance.

- Do you transport goods or products? This could be a caterer delivering food, a contractor hauling lumber, or a local farm dropping off produce boxes.

- Do you carry specialized tools or equipment? Think plumbers, electricians, photographers, or mobile mechanics. The equipment itself might need separate coverage, but just transporting it is a business activity.

- Do your employees run errands for the business? If you send a team member to the bank or to pick up supplies in their own car, your business is exposed to the liability.

- Do you transport people? This covers everything from non-emergency medical transport and airport shuttles to a daycare using a van to pick up kids.

Getting a handle on the crucial differences between policy types is the first step to protecting your business. For a deeper look, our guide on https://wexfordis.com/2025/06/03/commercial-vs-personal-auto-insurance/ breaks down the specific coverage gaps you need to watch out for.

Ultimately, this isn't just about following insurance rules—it's about smart business strategy. When a vehicle is essential to how you make money, it needs a policy built for that purpose. We can even learn from larger operations, like those involved in transportation companies' sustainability efforts. While their scale is different, the principle is identical. Failing to get the right coverage is simply a bet against your own success.

Decoding Your Commercial Auto Insurance Costs

Ever wonder why one business gets a shockingly low quote for commercial auto insurance while a similar company down the street is quoted a sky-high premium? It’s not random. Think of insurers as risk detectives; they piece together clues about your business to figure out the likelihood you’ll file a claim.

The more you understand their process, the more control you have over your costs. Your premium is a direct reflection of how risky your operations seem to an underwriter. It’s why a long-haul trucking firm will always pay more than a local flower shop—its trucks are on the road constantly, covering huge distances and carrying heavy loads, which naturally bumps up the chances of a major accident.

Key Factors That Drive Your Premiums

A handful of core variables do most of the heavy lifting when it comes to calculating your premium. Insurers look at everything from the rigs you run to the people behind the wheel. Each piece of information helps them build a complete risk profile for your business.

Here are the big ones they look at:

- Vehicle Type and Use: This is a huge one. A heavy-duty dump truck that spends its days on construction sites is a completely different animal than a small sedan an accountant uses for occasional client meetings. The vehicle's size, weight, and job function are front and center.

- Driving Records (MVRs): The history of your drivers is everything. If your team has clean Motor Vehicle Records (MVRs), you’re in a great position. A crew with a history of speeding tickets, at-fault accidents, or other violations will send your rates soaring.

- Travel Radius and Location: Where you drive and how far you go matters. A business that sticks to a small, local area is a much lower risk than one with vehicles crossing state lines. Likewise, operating in a congested city with bumper-to-bumper traffic is going to cost more than driving in a quiet rural town.

Think of your premium as a reflection of your on-the-road footprint. The larger, heavier, and more frequent that footprint is, the higher the cost to insure it. Controlling that footprint through careful management is key to affordability.

The industry you're in also plays a massive role. A company hauling hazardous materials, for example, faces astronomical premiums because an accident could be catastrophic. That’s a world away from a business that’s just delivering office supplies.

The Broader Market and Its Impact

Even if your business is a model of safety, your rates can still be affected by things completely out of your control. The commercial auto market has been a tough place lately, with rates climbing for almost everyone. Widespread driver shortages, more severe accidents caused by distracted driving, and inflation driving up the cost of vehicle repairs have all created a perfect storm.

You can get a better sense of these external pressures by reading up on commercial auto insurance market trends. It helps explain why even companies with spotless records might see their premiums creep up.

Actionable Strategies to Lower Your Insurance Costs

While you can’t change the market, you have more power over your own premiums than you might think. Don't just accept the first quote you get. By proactively managing your risk, you can make your business a much more attractive customer to insurers.

Here’s how you can take control:

- Implement a Driver Safety Program: This is a game-changer. Formal training on defensive driving, strict rules against phone use, and regular safety meetings show you’re serious about preventing accidents.

- Leverage Telematics Devices: Installing GPS trackers or other systems that monitor speed, hard braking, and mileage gives insurers cold, hard data proving your fleet is operated safely. This often leads to significant discounts.

- Hire Drivers with Clean Records: Make checking MVRs a non-negotiable step in your hiring process. Nothing keeps premiums down like a team of safe, reliable drivers.

- Choose the Right Deductible: Your deductible is what you pay out-of-pocket on a claim before insurance pays the rest. Agreeing to a higher deductible will lower your premium. Just make sure it’s an amount your business can comfortably cover if something happens.

Taking these steps transforms you from a passive insurance buyer into an active risk manager. For a more detailed breakdown, you can learn more about how to manage your business auto insurance cost in our comprehensive guide. This proactive approach doesn't just save you money—it helps you build a safer, stronger business.

Navigating the Claims Process After an Accident

An accident is jarring, to say the least. The last thing you need is a complicated, drawn-out claims process on top of it all. When something unexpected happens, knowing exactly what to do can make all the difference—protecting your driver, your assets, and your business.

Think of the claims process less like a confrontation and more like a structured conversation with your insurance company. Your job is to clearly and accurately explain what happened. Their job is to investigate and cover the losses according to the policy you've paid for.

Immediate Steps to Take at the Scene

The first few moments after an accident are absolutely critical. What your driver does right then and there can have a huge impact on how a future claim plays out. Training your team on these steps isn't just a good idea; it's essential risk management.

A calm, methodical approach is everything. Safety first, always. Documentation second.

- Ensure Everyone's Safety: The first priority is to check for injuries. Call 911 immediately if anyone is hurt and to get the police on their way. A police report is an indispensable piece of evidence for your claim.

- Move to a Safe Location: If the vehicles are still drivable and are creating a hazard, move them to the shoulder or a safe spot off the road. Flip on the hazard lights.

- Exchange Information Calmly: Get the essential details from the other driver. It’s crucial to instruct your drivers not to admit fault or even apologize, as that can be misinterpreted. Stick strictly to the facts.

The information gathered at the scene becomes the bedrock of your claim.

Gathering and Documenting Crucial Evidence

Solid documentation is your best friend when filing a claim. Make sure your drivers know to use their smartphones to capture every possible detail while the scene is still fresh.

This evidence is what the claims adjuster will use to reconstruct exactly what happened.

- Take Photos and Videos: Get shots of the damage to all vehicles from every angle. Pan out and capture the entire scene, including any skid marks, nearby road signs, and even the weather conditions.

- Collect Contact Information: Get the full names, phone numbers, addresses, and insurance policy details for all drivers involved. If there are any witnesses, get their contact info, too.

- Note the Details: Jot down the time, date, and specific location of the accident. Be sure to get the name and badge number of the responding police officer.

This information is pure gold, especially since memories of a stressful event can fade and change quickly.

Your goal is to create a detailed, objective record of the event. The more high-quality information you provide your insurer, the smoother and faster the claims process will be. An organized file prevents delays and disputes.

Reporting the Claim and Working with an Adjuster

Once everyone is safe and the scene is documented, it's time to call your insurance company. Report the claim as soon as you possibly can, even if the damage looks minor at first glance. Waiting too long can sometimes put your coverage at risk.

After you file, your case will be handed over to a claims adjuster. This person becomes your main point of contact. Their job is to investigate the accident, determine who was at fault, and calculate the cost of the damages.

Give them all the documentation you collected and cooperate fully with their investigation. They’ll review the police report, talk to witnesses, and look at the photos to make their final determination. Keeping good records and maintaining open communication is the surest path to a fair and timely settlement, which gets your vehicle—and your business—back on the road that much faster. It also helps to understand how long the insurance claim process can take to set realistic expectations from the start.

Thinking Beyond a Policy to Protect Your Business

It’s easy to look at your commercial auto insurance premium and see it as just another line item on the expense report. That's a huge mistake. A well-built policy isn't just an expense; it's a critical safety net for your entire business. It goes far beyond paying to fix a dented bumper—it acts as a financial firewall against the kind of catastrophic events that can shut a company down for good.

This isn't just about compliance. It’s a strategic investment that protects your hard-earned assets from crippling lawsuits, helps you get back on your feet after a major accident, and even bolsters your professional reputation. When potential clients and partners see you’re properly insured, it sends a powerful message of stability and responsibility.

A comprehensive policy is often the only thing standing between a manageable setback and a complete business shutdown. It’s the framework that allows your company to absorb a major shock—like a multi-vehicle pile-up—and keep moving forward.

This protective layer has never been more important. Even as global insurance pricing eases in some areas, the commercial auto market is still feeling the heat. Sky-high repair costs and "social inflation" around claims are driving significant rate increases. Insurers are digging deep into their data to navigate this tough environment, which is something Marsh has highlighted in their market insights.

Integrating Insurance into Your Overall Risk Strategy

Real protection comes from a layered defense, not just a single piece of paper. When you combine a strong insurance policy with proactive, on-the-ground safety measures, you create a powerful system to prevent losses, control your premiums, and protect your bottom line.

Think of it like securing a building. Your insurance policy is the alarm system that alerts you after a break-in, but solid locks and security cameras can stop the thief from getting inside in the first place.

Here’s how to build a stronger defense for your business:

- Implement a Driver Safety Program: This is your front line. Formal training, clear rules of the road, and consistent enforcement are proven to reduce accidents.

- Utilize Physical Security: Technology can be a game-changer. For example, installing modern vehicle immobilisers can be a powerful deterrent against theft, adding another layer of security for your valuable assets.

- Adopt Comprehensive Liability Coverage: Your auto policy is a vital piece of a much larger puzzle. To be truly protected, you need to see how it fits with other coverages. For instance, understanding how management liability coverage protects your company's leaders is crucial for a complete risk management plan.

By connecting these dots, you stop treating commercial auto insurance as a mandatory cost and start using it as a cornerstone of your long-term business strategy.

Common Questions About Commercial Auto Insurance

Even after you get the basics down, you're bound to have more questions as you start shopping for a policy. It’s completely normal. Let’s walk through a few of the most common issues we help business owners sort out every day.

Getting these details right is the key to making sure your policy truly has your back when you need it most.

Does This Policy Cover Tools Inside My Vehicle?

This is a big one, especially for tradespeople. If someone breaks into your work van and steals your equipment, is it covered? Unfortunately, the answer is almost always no.

Your commercial auto policy is built to protect the vehicle itself—things like collision damage or liability if you cause an accident. It wasn't designed to cover the valuable cargo you carry inside. Think of it this way: the policy covers the truck, not what's in the truck.

To get that protection, you’ll need a different kind of coverage called Inland Marine insurance. It sounds a little strange, but it’s specifically designed to protect tools, equipment, and other property while it’s on the move.

What Is Hired and Non-Owned Auto Coverage?

This is easily one of the most overlooked—and most important—add-ons to a commercial auto policy. It’s all about protecting your business when an accident involves a vehicle you use for work but don't actually own.

Here's how it breaks down:

- Hired Auto Coverage: This kicks in when you rent, lease, or borrow a vehicle for a job. Say you need a bigger truck for a one-day project and you rent one—this coverage protects your business if one of your drivers gets into an accident with it.

- Non-Owned Auto Coverage: This is for situations where an employee uses their own car for a work errand. If your team member is driving their personal sedan to meet a client or run to the bank for the business and causes a wreck, this protects your company from being sued.

Without this coverage, you’re on the hook for any accidents that happen in a vehicle that isn’t on your policy but is being used for your business. Considering over 47% of small businesses have employees using their own cars for work, this is a must-have.

Can I List My Work Truck on My Personal Policy?

Trying to save a few bucks by putting your work truck on your personal auto insurance is one of the biggest gambles you can take as a business owner. Personal policies are simply not built for commercial risks, and nearly all of them include what’s called a "business use exclusion."

What does that mean? If you get into an accident while doing anything for work—even just driving between job sites—your insurance company will likely deny the claim on the spot. You'd be left holding the bag for every dollar of damage, medical bills, and any lawsuits that follow. It's a risk that could easily put you out of business.

Commercial auto insurance has a lot of moving parts, but you don't have to figure it all out on your own. The experts at Wexford Insurance Solutions are here to help you build a policy that fits your business perfectly, giving you peace of mind on the road. Contact us today for a personalized consultation.

How Long Does the Insurance Claim Process Take? Find Out NowHome and Auto Insurance Comparison Guide

How Long Does the Insurance Claim Process Take? Find Out NowHome and Auto Insurance Comparison Guide