It’s the question every homeowner with a crack in their wall dreads asking: is my foundation covered by my insurance?

The honest answer is… it depends. Homeowners insurance will only step in to cover foundation repairs if the damage was caused by a specific, sudden event that’s explicitly listed in your policy. These events are what we in the industry call "covered perils."

Think of it this way: a pipe suddenly bursting and washing out the soil under your home is a whole different ballgame than a hairline crack that’s been slowly creeping up your wall for a decade. One is an accident; the other is a process.

The All-Important Difference: Sudden vs. Gradual Damage

This is where most homeowners get tripped up. A standard policy is built to protect you from unexpected disasters, not from the predictable effects of time, settling soil, or deferred maintenance. This distinction is the number one reason so many foundation repair claims get denied right out of the gate.

The core principle is sudden and accidental damage. If a tornado rips through town and the sheer force of the wind cracks your foundation, that’s a classic covered peril. But if those same cracks show up because the soil under your house has been slowly expanding and contracting for years? That’s almost always excluded from a standard policy.

Foundation Damage Coverage at a Glance

To make this clearer, let's break down some common causes of foundation problems and see how an insurance company typically views them.

| Cause of Damage | Typically Covered? | Reasoning |

|---|---|---|

| Sudden Pipe Burst | Yes | The damage is sudden, accidental, and caused by a covered peril (water damage from plumbing). |

| Natural Settling & Shifting | No | This is considered normal wear and tear and a part of the home's natural aging process. |

| Earthquake or Flood | No (Standard Policy) | These events require separate, specific insurance policies (earthquake or flood insurance). |

| Poor Soil Compaction | No | This is usually seen as a construction defect or a pre-existing issue, not a sudden event. |

| Long-Term Water Seepage | No | Damage from poor drainage or clogged gutters is considered a maintenance issue. |

| Tree Root Intrusion | No | This is a slow, gradual process and often falls under homeowner maintenance responsibilities. |

| Tornado or Windstorm | Yes | Direct damage from a named storm or major wind event is a classic covered peril. |

| Fire or Explosion | Yes | These are sudden, catastrophic events that are standard covered perils in most policies. |

This table is a good starting point, but remember that the exact language in your specific policy is what truly matters.

Real-World Scenarios and How Coverage Applies

Let's put this into practice with a few examples:

-

Sudden Water Damage: A water heater in your basement lets go, flooding the area and eroding the soil beneath your slab, causing it to crack. This is a strong candidate for a covered claim.

-

Natural Settling: Your house is 25 years old and has developed those familiar stair-step cracks in the brick as it settles. This is viewed as routine wear and tear and won't be covered.

-

Poor Drainage: For years, your gutters have been overflowing, causing water to pool against the foundation. That slow, steady pressure eventually leads to water damage and cracks. Your insurer will almost certainly deny this, pointing to it as a preventable maintenance issue.

Think of your homeowners insurance as a shield against unforeseen accidents, not as a warranty against the natural aging of your house. It’s always the cause of the damage—not just the damage itself—that determines whether you have a valid claim.

Now, if the damage is from a covered peril like a fire, windstorm, or that burst pipe, your dwelling coverage is what kicks in. These limits often range from $100,000 to $500,000, which is typically more than enough for even extensive foundation work. But as we've seen, getting to that point depends entirely on what caused the problem in the first place.

Navigating these rules can be complex. For a broader look at how these policies are structured, our complete guide to homeowners insurance can help fill in the gaps.

Understanding What a Covered Peril Actually Is

Insurance policies can feel like they're written in another language, but one term is key to cracking the code: covered peril. This is the single most important concept to grasp when you're trying to figure out if your homeowners insurance will pay for foundation repair.

Think of your policy as a list of specific disasters it agrees to protect you from. A covered peril is simply one of those events on the list. It’s the "what" that caused the damage.

The crucial detail here is that these perils are almost always sudden and accidental. For example, imagine a violent windstorm tears a huge tree out of your yard, and the force of its roots rips through the ground, cracking your foundation. That’s a sudden event, directly caused by a listed peril (windstorm).

The Peril Defines the Payout

Now, consider the opposite scenario. If that same foundation develops cracks because the soil has been slowly and gradually settling over the last 20 years, that's a different story. That’s just considered normal wear and tear—a standard exclusion in virtually every policy. Insurance is built for unexpected accidents, not the predictable effects of aging.

Here are a few common examples of covered perils that could lead to a legitimate foundation damage claim:

- Fire or Explosion: The extreme heat or concussive force from a fire or explosion can easily compromise the structural integrity of your foundation.

- Sudden Water Damage: A pipe bursts inside a wall, gushing gallons of water that wash away the soil supporting your foundation. This is a world away from a slow, dripping leak.

- Aircraft or Vehicles: A car loses control and smashes into the side of your house, causing immediate, direct damage to the foundation wall.

- Vandalism: It’s less common, but if someone intentionally damages your home in a way that affects the foundation, that would be considered a covered peril.

A covered peril is the specific, named cause of damage listed in your policy. If the cause isn't on the list—or is specifically excluded—the resulting damage won't be covered, no matter how severe.

Differentiating Between Water Perils

Water damage is one of the most confusing areas for homeowners. A sudden pipe burst is a covered peril, but gradual seepage from a leaky faucet is a maintenance problem you’re expected to handle. It all comes down to the source of the water. For instance, the process of fixing water leakage through your ceiling might reveal that the cause was a sudden plumbing failure (covered) rather than a slow roof leak that went unnoticed for months (likely not covered).

This is exactly why documenting everything is so important when you file a claim. You have to show that the damage was a direct result of a covered event, not a pre-existing or slow-moving issue.

And on a related note, for homeowners looking to make their insurance life a little easier, bundling home and auto insurance can often simplify things and even save you some money in the long run.

Why Most Foundation Repair Claims Get Denied

It’s one of the most frustrating moments for a homeowner. You spot a crack spreading across your foundation, file a claim thinking you’re protected, only to receive that dreaded denial letter. It happens all the time, and understanding why is the key to setting realistic expectations and navigating your options.

The hard truth is that standard homeowner's insurance is built to cover sudden, accidental disasters—not the slow, creeping problems that often plague foundations. Insurers look at your foundation a bit like the tires on your car. They’ll help if a sudden road hazard causes a blowout, but they won’t pay to replace them just because the tread has worn thin over thousands of miles.

The numbers paint a clear picture. Industry insiders estimate that a staggering 70% to 80% of all foundation insurance claims are denied. Why? Most often, the cause is chalked up to gradual damage or maintenance issues, which leaves homeowners on the hook for some of the most expensive repairs imaginable.

The Problem with Natural Processes

Many of the forces that wreak havoc on a foundation are natural, happen over a long time, and are almost always excluded from a standard policy. From an insurer's perspective, these are predictable events that fall under the umbrella of routine home maintenance and upkeep.

Here are the most common culprits for claim denials:

- Settling, Sinking, or Shifting: Every house settles over time. This slow, downward movement is a completely normal process that can cause cracks, but it's not a sudden event your policy is designed to cover.

- Expanding or Shrinking Soil: If you live in an area with clay soil, you know the drill. The soil swells with moisture and shrinks when it dries out. This constant push-and-pull exerts incredible force on your foundation, but it’s a gradual process, not an insurable accident.

- Wear and Tear: Nothing lasts forever, including concrete and steel. The slow breakdown of materials over decades is considered normal aging, not damage from a covered event.

- Faulty Construction: If your home's foundation had issues from day one due to poor workmanship or materials, any resulting problems are typically excluded. Insurance is meant to protect against future risks, not fix pre-existing defects.

Here's a simple way to think about it: If the damage happened in a matter of minutes or hours (like a pipe bursting and flooding the crawlspace), you might have a case. If it developed over months or years (like a wall slowly bowing from soil pressure), it's almost certainly not covered.

Major Events That Require Separate Policies

On top of gradual damage, the two biggest potential disasters for a foundation—floods and earthquakes—are also explicitly excluded from standard homeowner's policies. The risk of these events is so immense and geographically concentrated that they require their own specialized insurance.

- Flood Damage: This is a big one. Damage from rising rivers, coastal storm surges, or widespread surface water from heavy rain is not covered. For that, you absolutely need a separate flood insurance policy.

- Earth Movement: Any damage caused by earthquakes, tremors, or even landslides falls under this exclusion. To be protected, you must purchase a specific earthquake insurance policy.

It's crucial to understand the difference between "water damage" (from an internal source like a burst pipe) and "flood damage" (from an external, natural source). You can get a clearer picture of this by exploring the key differences between flood insurance and homeowners insurance. Knowing what's what can help you spot and close major gaps in your coverage before disaster strikes.

Bridging the Gaps in Your Homeowners Policy

Your standard homeowners policy is a great starting point, but it's far from a catch-all. It's more like a sturdy umbrella designed for a typical rainstorm—it’s not going to hold up in a hurricane. When it comes to something as critical as your home’s foundation, those coverage gaps can become a massive problem.

Thankfully, you can patch those holes. You can add specific coverages, known as endorsements, to your existing policy or purchase separate, specialized policies to build a much stronger financial safety net.

Key Endorsements for Foundation Protection

Think of endorsements as small but powerful upgrades. They bolt on to your main policy to cover specific risks that are normally excluded. While no insurance will ever pay for damage from simple old age or poor maintenance, a few key endorsements can be lifesavers for foundation-related issues.

One of the most crucial is Water Backup and Sump Pump Overflow coverage. Standard policies almost never cover damage from a backed-up sewer line or a failed sump pump. But if that water floods your basement and starts washing away the soil supporting your foundation, this small add-on can save you from a catastrophic out-of-pocket expense.

Here are a couple of smart additions to discuss with your agent:

- Water Backup Coverage: A must-have for any home with a basement. This covers damage when sewers or drains back up or your sump pump gives out.

- Service Line Coverage: This pays to repair underground pipes on your property, like your main water or sewer line. A leak in one of these can saturate the ground and compromise your foundation over time.

When You Need a Completely Separate Policy

Some risks are just too big for a simple endorsement. Catastrophic events like floods and earthquakes are always excluded from a standard homeowners policy. To get coverage, you have to buy a completely separate, specialized policy.

For homes in flood plains or earthquake-prone regions, these policies aren't just a nice-to-have—they're an absolute necessity. Don't wait until the storm is on the horizon or the ground starts shaking to think about coverage. By then, it’s too late.

If you're anywhere near a river, lake, or coastline, Flood Insurance is non-negotiable. And if your home is in an area with known seismic activity, Earthquake Insurance is the only thing that will protect your foundation from the immense damage caused by shifting ground.

These policies can feel like an extra cost, but they're a wise investment in your home's future. For more ideas on managing costs, check out our guide on how to lower home insurance premiums and see how you can fit comprehensive protection into your budget.

A Step-by-Step Guide to Filing Your Claim

That heart-sinking moment when you spot a crack in your foundation can be overwhelming. But what you do in the next few hours and days is what really counts. Taking a calm, methodical approach can be the difference between a paid claim and a denied one. Think of yourself as building a case—the more organized and detailed you are from the start, the stronger it will be.

Your very first job is to stop the damage from getting worse. If a burst pipe is flooding your basement, find that main water shut-off valve immediately. If a storm ripped a hole in your siding and water is getting in, get a tarp over it. This is called mitigating damages, and it's not just a good idea; your policy likely requires you to do it.

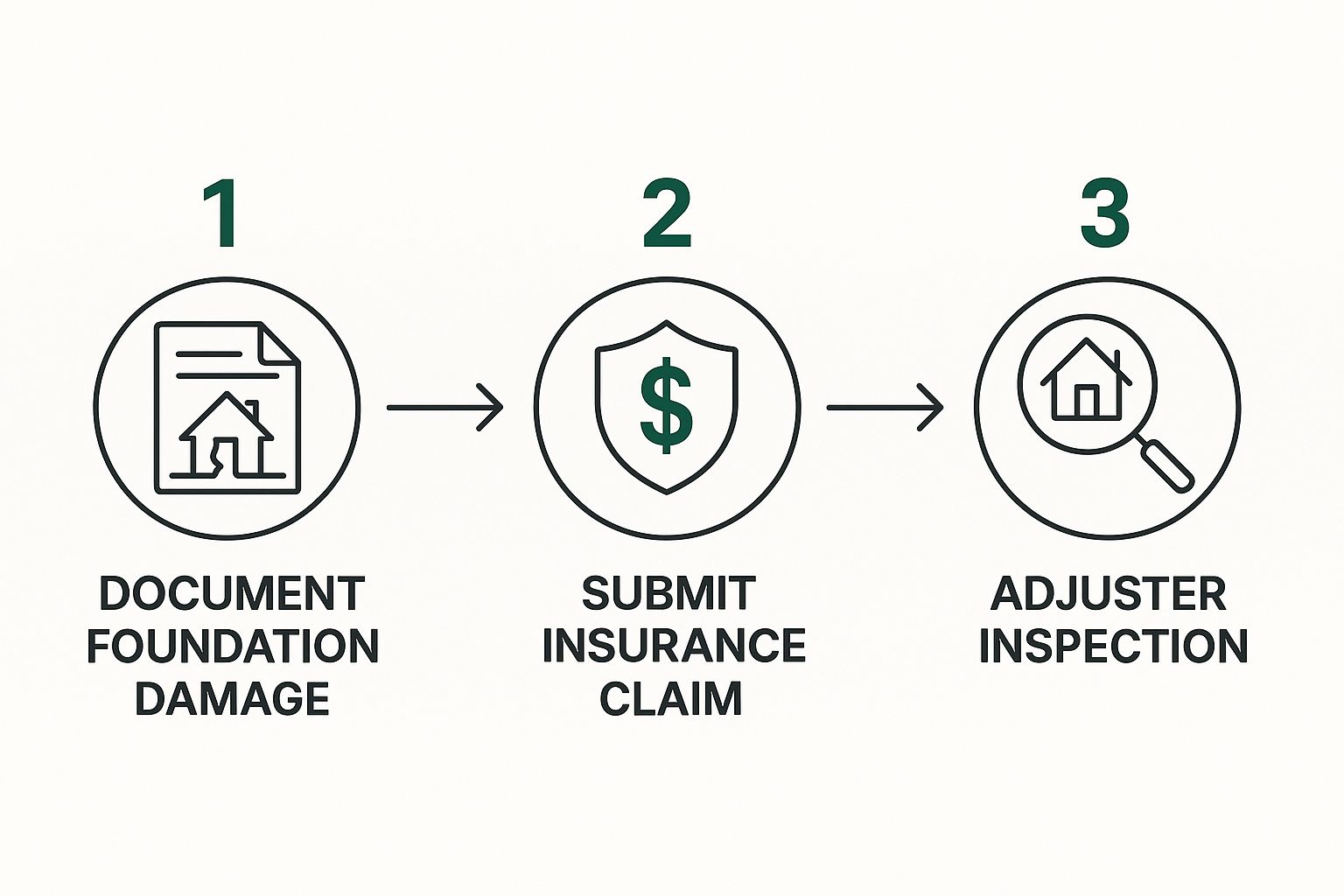

Document Everything Immediately

Once you’ve stopped the immediate bleeding, it’s time to put on your detective hat. Before you clean up or move a single thing, document every last detail of the damage. This evidence is the bedrock of your entire claim.

- Go crazy with photos: Use your smartphone and take dozens of pictures. Get up close to show the details of the cracks, then take wide shots to show the full context of the room or wall. No photo is a bad photo here.

- Shoot some video: A slow video walkthrough can be even more compelling. As you record, talk about what you're seeing. This narrative can be incredibly helpful later.

- Dig up your paperwork: Do you have receipts from a recent plumbing job? A report from your home inspection when you bought the house? Gather any document that might be relevant.

This visual shows how these crucial first steps flow, from your initial documentation all the way to the adjuster's visit.

Following this order helps ensure you’ve built a solid case before your insurance company even gets involved.

Get an Independent Expert Opinion

Here’s a pro tip: Before you even dial your insurance company's number, think about hiring an independent structural engineer. Yes, it’s an out-of-pocket expense, but their unbiased, professional report can be the most powerful weapon in your arsenal. An engineer’s sole job is to determine the cause of the damage—the one critical fact your entire claim will pivot on.

An adjuster works for the insurance company. A structural engineer works for you. Their assessment provides objective proof that connects the damage to a specific, covered event, which is exactly what you need to prove your case.

With your own documentation and an expert’s report in hand, you're ready to make the call. For a deep dive into what happens next, check out our full walkthrough on the https://wexfordis.com/2025/05/26/homeowner-insurance-claim-process/.

Navigating the Claim and Adjuster Visit

Once you file the claim, the insurer will assign an adjuster to your case. They will schedule a time to come out and inspect the damage personally. Make sure you are there for that visit. Have your folder of photos, videos, and the engineer’s report ready to go.

Answer the adjuster’s questions honestly, but don't guess or speculate about what you think caused the damage. Stick to the facts you know and point them to your engineer's findings. The adjuster will create their own report, which they'll use to recommend whether your claim gets approved or denied.

For more general advice on handling the entire ordeal, this guide to navigating property insurance claims is a fantastic resource. And if your claim is denied? Don't give up. You have the right to appeal, and all the evidence you’ve so carefully gathered will be your best friend in challenging that decision.

Managing Repair Costs and Preventing Future Damage

Whether your insurance claim gets a green light or you’re paying out-of-pocket, your focus now shifts to two things: managing the repair bill and stopping this from ever happening again. Let’s be honest—foundation work has a reputation for being expensive, and for good reason.

A simple crack might only set you back a few hundred dollars. But if you’re looking at serious solutions like underpinning or installing piers, the costs can quickly climb into the tens of thousands. Seeing those numbers really drives home the value of getting ahead of problems before they start.

Estimated Foundation Repair Costs by Method

To give you a clearer picture of what you might be facing, we've broken down some of the most common repair methods and their typical costs. Keep in mind that these are just estimates; your specific situation, location, and the extent of the damage will all play a role in the final price.

| Repair Method | Typical Cost Range | Best For |

|---|---|---|

| Epoxy/Polyurethane Injection | $600 – $1,500 per crack | Sealing non-structural, hairline cracks in concrete walls. |

| Carbon Fiber Straps | $4,000 – $10,000 | Reinforcing bowing or buckling basement walls from inward pressure. |

| Helical Piers (Underpinning) | $15,000 – $30,000+ | Stabilizing foundations on unstable soil; often used for lighter structures. |

| Push Piers (Underpinning) | $12,000 – $40,000+ | Lifting and stabilizing settled foundations, especially for heavier homes. |

| Mudjacking/Slabjacking | $3,000 – $15,000 | Lifting and leveling sunken concrete slabs, like driveways or patios. |

These figures show that an ounce of prevention is truly worth a pound of cure. Taking proactive steps now is the best way to avoid these significant expenses down the road.

Proactive Home Maintenance for Foundation Health

When it comes to your foundation, prevention is always cheaper than a cure. The vast majority of foundation issues can be traced back to a single culprit: water. How you manage moisture around your home is the single most important factor in protecting its structural integrity.

One of the best things you can do is implement effective backyard drainage solutions that guide water safely away from your home's base. This alone can prevent the soil from becoming overly saturated, which is what creates the immense pressure that cracks and shifts foundations.

Here are a few essential maintenance tasks you should put on your regular to-do list:

- Clean Your Gutters Regularly: Clogged gutters and downspouts are a recipe for disaster. Keep them clear so rainwater is channeled far from your foundation where it belongs.

- Maintain Proper Grading: The ground around your home should slope away from the foundation. If it slopes inward, you’re basically inviting water to pool against your walls.

- Watch Your Landscaping: Be mindful of where you plant large trees. Aggressive root systems can grow into your foundation over time, causing serious damage.

- Monitor for Leaks: Periodically check your basement, crawl space, and plumbing for any signs of moisture or musty smells. Catching a small leak early can save you from a major headache later.

Think of your home's foundation like your own health. Regular check-ups and preventative care are far more effective and less expensive than waiting for an emergency.

By integrating these simple habits, you dramatically lower the odds of ever needing to find out if homeowners insurance covers foundation repair. A little bit of maintenance goes a very long way in protecting your home and your peace of mind.

Frequently Asked Questions About Foundation Repair and Insurance

Even when you know the basics of "covered perils," the real world gets messy. Let's walk through some of the questions I hear all the time from homeowners trying to figure out where their insurance policy stands on foundation problems.

Are Those Small Foundation Cracks Covered?

This is a classic question, and the answer almost always circles back to one thing: what caused the crack? Those tiny, hairline cracks that show up over time are usually from the house settling naturally. Insurance companies see this as regular home maintenance, so it's not covered.

But what if a bunch of new, bigger cracks show up right after a pipe bursts under your home? Now we're talking. If you can directly link the damage to a covered event, you have a strong case for a claim. This is where getting a report from an independent structural engineer becomes so important—it’s your best evidence for proving the cause.

What if My Foundation Claim Gets Denied?

Getting a denial letter feels like hitting a brick wall, but it doesn't have to be the end of the story. Your first step is to get the denial in writing so you can see their exact reason for saying no. If you've got solid proof that they're wrong—like that engineer's report we just talked about—you can file an appeal.

Don't just accept the first "no" as the final answer. A thorough, well-documented appeal backed by professional reports can absolutely get an initial denial overturned.

If your appeal doesn't go through, bringing in a public adjuster who can fight on your behalf is a solid next step.

Does My Location Change My Insurance Needs?

Yes, a thousand times yes. Where you live is one of the biggest factors in what kind of foundation coverage you really need.

- Earthquake-Prone Areas: Living in a state like California? A separate earthquake policy isn't just a good idea; it's practically a necessity.

- Coastal or Low-Lying Regions: If you're anywhere near the coast or in a floodplain, standard policies won't touch flood damage. You'll need a dedicated flood insurance policy to be protected.

- Areas with Expansive Clay Soil: In states like Texas, where the soil swells and shrinks dramatically, you have to pay extra close attention to your policy's wording on soil movement. It's often excluded, so you need to know exactly what you're up against.

Trying to make sense of your policy's fine print can feel overwhelming. At Wexford Insurance Solutions, our job is to help you spot these kinds of coverage gaps and find the right protection for your home's specific situation. Contact us today for a personalized review of your insurance needs.

General Liability Insurance for Sole Proprietors | Protect Your BusinessWhat Is an Insurance Binder Explained Simply

General Liability Insurance for Sole Proprietors | Protect Your BusinessWhat Is an Insurance Binder Explained Simply