When you buy professional liability insurance, one of the most important things to understand is the retroactive date. Think of it as the official starting line for your coverage.

This date sets a clear boundary. Any professional work you did before this date isn't covered by your current policy, even if a client files a claim for that old work today.

The Starting Line for Your Professional Protection

Imagine your insurance policy has a memory. The retroactive date is the very first day that memory begins. This is a core concept in "claims-made" policies, which are the standard for professionals like doctors, consultants, and architects—fields where a mistake made years ago could surface unexpectedly.

If a claim pops up from a project you completed after your retroactive date, your policy can step in to help. But if the claim is linked to an incident that happened even one day before that date, your current insurance won't cover it.

To help clear this up, let's break down what the retroactive date is and what it isn't.

Retroactive Date at a Glance

| Concept | What It Is | What It Is NOT |

|---|---|---|

| Coverage Start | The first date from which your professional services are covered. | The date your current policy period started (the effective date). |

| Claim Trigger | A hard cutoff; the wrongful act must occur on or after this date. | A guarantee of coverage for any claim made during the policy period. |

| Historical Scope | The key to providing "prior acts" coverage for your past work. | A replacement for a policy from a previous year. |

Basically, this single date is what separates a covered past mistake from an uncovered one.

Getting a handle on this concept is the first step in learning how to read an insurance policy and making sure your career is truly protected. It's especially critical for policies like Errors & Omissions (E&O), where it draws a clear line in the sand for when your coverage officially began.

How Claims-Made Policies Use a Retroactive Date

To really get a handle on the retroactive date, it helps to see how it fits into the two main types of professional liability policies. Think of an 'occurrence-based' policy as a lifetime photo album. It covers any incident that took place while your policy was active, even if the claim is filed years later.

A claims-made policy, on the other hand, is more like an album from a specific trip. It only covers claims that you actually file during the current policy period, and only for incidents that happened after a specific date—your retroactive date. This approach is standard in professions where a mistake made today might not surface for a long, long time.

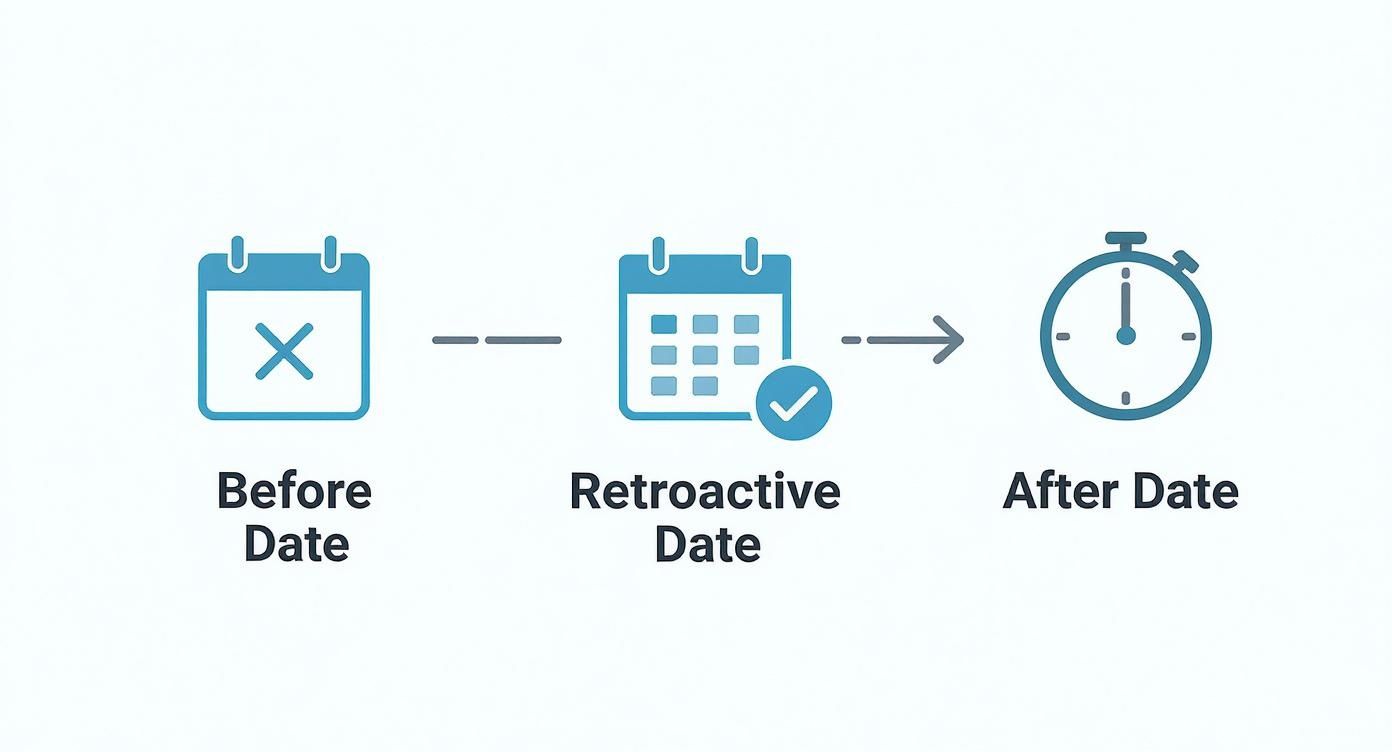

This timeline gives you a great visual of how a retroactive date acts as a clear "start line" for your coverage.

As the graphic shows, any professional work you did before that retroactive date is simply not covered by this policy. It draws a firm boundary around what the insurer is responsible for.

The Problem Claims-Made Policies Solve

So, why even have this structure? Insurers created it to solve a very specific problem: preventing someone from buying a new policy only after they have a gut feeling that a past mistake is about to turn into a lawsuit.

In insurance circles, this is often called the "burning building" problem. You can't buy fire insurance for a house that's already on fire. The retroactive date ensures policies cover unforeseen future claims, not known past errors that are just waiting to blow up.

This principle is what keeps professional liability insurance available and affordable. It allows insurers to manage their risk by not taking on responsibility for an unknown history of potential claims.

This concept becomes especially critical when you stop working. If you retire or switch careers and let your policy lapse, you instantly lose coverage for all your past work. The only way to protect yourself is by securing an extension, which you can learn more about by exploring what is tail coverage insurance. This special endorsement extends your reporting period, making sure your retroactive date continues to shield you long after you’ve stopped paying for your regular policy.

Protecting Your Retroactive Date: Why It Matters

Think of your retroactive date as the starting line for your professional liability protection. It's a critical asset, usually set to the day your very first claims-made policy kicked in. Your goal is to carry that exact date with you for your entire career.

The secret to keeping that date intact is continuity. Simple as that. Maintaining an unbroken chain of insurance coverage is the most important thing you can do to protect your past work. A single lapse, even a short one, can be disastrous, wiping out years of protection and leaving you exposed.

Why Continuous Coverage is Everything

When it's time to switch insurance carriers, your new provider will almost always agree to keep your original retroactive date. But there's a catch: you can't have any gaps in coverage. This smooth handoff is what keeps your professional history fully insured.

Let your policy expire, though, and it's a different story. A new insurer will likely set your retroactive date to the start date of the new policy. This creates a massive blind spot, leaving every bit of work you did before that new date completely uninsured. Insurers extend the courtesy of matching your date to win your business, but that offer disappears the moment you have a lapse.

The Golden Rule of Retroactive Dates: Never, ever let your claims-made policy lapse. The potential financial hit from an old project coming back to haunt you far outweighs whatever you might save by skipping a premium payment.

This is especially crucial when you're changing jobs or hanging your own shingle. Before your old policy's term is up, you need to have your new coverage locked and loaded. Sometimes, getting an insurance binder can act as a temporary bridge, giving you official proof of coverage while the full policy is being issued.

At the end of the day, protecting your retroactive date is about protecting your past. If you make continuous coverage a priority, you ensure that a mistake made years ago doesn't turn into a financial nightmare today.

Real-World Scenarios: The Retroactive Date in Action

Let's move beyond the jargon and see how the retroactive date plays out in the real world. Abstract definitions are one thing, but seeing the financial impact this single date can have on a professional's career really brings the concept home.

These stories show the razor-thin line between a protected professional history and a dangerously exposed one. It all comes down to how that date is managed.

The Protected Consultant

Meet Sarah, a management consultant who has been on top of her professional liability insurance for 10 years. Her retroactive date is set to the very first day she opened her practice, and she’s made sure to never let her coverage lapse, even when she switched insurance carriers.

One day, a lawsuit lands on her desk. A former client claims her strategic advice from four years ago led to a massive financial downturn for their company.

Because Sarah maintained continuous coverage, her retroactive date has her back. The alleged mistake happened long after her policy's "start line." Her insurance company steps in, handling the hefty legal defense costs and the eventual settlement. Her business is saved from what could have been a catastrophic financial hit.

The Exposed Developer

Now, let's look at Mark, a freelance software developer. He hit a slow period and decided to cut costs by letting his claims-made policy lapse for just three months. When he landed a new gig, he bought a new policy, but this time his retroactive date was reset to the start date of the new coverage.

Six months later, a client from a project he finished before the coverage gap sues him. They claim a critical coding error he made a year ago has just caused a major data breach.

Mark is in serious trouble. Since the error happened before his new retroactive date, his current insurer denies the claim, leaving him to face the lawsuit completely on his own. Protecting your retroactive date is everything; an improper denial could even lead to a bad faith insurance claim. Mark's situation is a tough lesson, and if you ever face a similar denial, knowing how to dispute an insurance claim is your crucial next move.

Why the Retroactive Date Is a Game-Changer in High-Risk Fields

In professions like medicine, law, or technology, the fallout from a single mistake can take years to become apparent. This is where the retroactive date steps in. It’s far more than just a technical detail on your policy; it’s your primary defense against this "long-tail risk"—the often huge gap between when an error happens and when a claim is actually filed.

Think about a tech company that suffers a data breach today. The root cause might be a security flaw that was overlooked years ago. Without a retroactive date establishing a clear starting point for coverage, insurers would be flying blind, trying to price policies without knowing what historical risks they were taking on.

Taming a Wild Market

Claims-made policies really took off after the professional liability crisis of the 1980s, especially in the U.S., as insurers scrambled to get a handle on their exposure. It was a strategic shift to manage risk, and it worked. Today, an estimated 70-80% of claims-made policies feature a retroactive date to draw a firm line in the sand.

This structure is what allows insurance carriers to offer stable, predictable pricing. By defining the exact period of past work they're covering, they can focus on protecting you from future unknowns instead of hidden liabilities from years ago. This is a core principle of modern errors and omissions insurance, making sure coverage stays both available and affordable for professionals who need it most.

The retroactive date is the insurer's safeguard against buying a past full of unknown problems. It makes sure everyone—both you and the insurance company—is crystal clear on what's covered, eliminating nasty surprises down the line.

Answering Your Questions About Retroactive Dates

When you're digging into the fine print of a professional liability policy, a few key questions always seem to pop up. Let's tackle some of the most common ones about the retroactive date to help you get a handle on your coverage.

Think of this as a quick-reference guide for real-world scenarios you might encounter.

Can I Get a Policy Without a Retroactive Date?

Yes, you can. This is what’s known in the industry as "full prior acts" coverage. It’s designed to cover you for any work you’ve done in the past, no matter how long ago, as long as you had no idea a claim might be coming when you bought the policy.

But here's the catch: these policies are hard to come by and cost a lot more. Insurers typically only offer them to professionals with a long, unbroken, and claim-free insurance history. For most people, it's more of an exception than a standard option.

What if My Policy Has the Wrong Retroactive Date?

If you spot an incorrect retroactive date, you need to contact your insurance broker or provider right away. This isn't a minor clerical error; it’s a critical mistake that could leave huge chunks of your professional history exposed and uninsured.

To fix it, you'll need to show proof of your continuous past coverage. The easiest way is to provide the declarations pages from your previous policies. Don't delay—the sooner you act, the faster you can close that dangerous gap in your professional protection.

An incorrect date isn't just a typo; it's a fundamental flaw in your professional safety net. Always double-check this date on every new policy and renewal document you receive to confirm your past work is still covered.

How Does Tail Coverage Connect to My Retroactive Date?

Tail coverage (officially called an Extended Reporting Period or ERP) is an optional feature you can buy when you're ending a claims-made policy. It gives you extra time to report claims that come up in the future for work you did while you were covered.

Essentially, it keeps your retroactive date active even after your policy has ended. This is crucial for anyone retiring, switching careers, or closing down their business, ensuring you're not left unprotected from a claim that surfaces years down the road.

At Wexford Insurance Solutions, our job is to make complex topics like retroactive dates simple, ensuring your professional liability coverage is solid and complete. Contact us today for a policy review.

What Is the Average Homeowner Insurance Cost Today

What Is the Average Homeowner Insurance Cost Today How to negotiate insurance settlement: Win your claim

How to negotiate insurance settlement: Win your claim