Think of cyber liability insurance as your company's digital bodyguard. When a data breach, ransomware attack, or other cyber incident tries to land a knockout blow, this policy steps in to absorb the impact and keep your business on its feet. It's the critical safety net for any organization that handles sensitive data—which, let's face it, is just about everyone these days.

Why Cyber Liability Insurance Is No Longer Optional

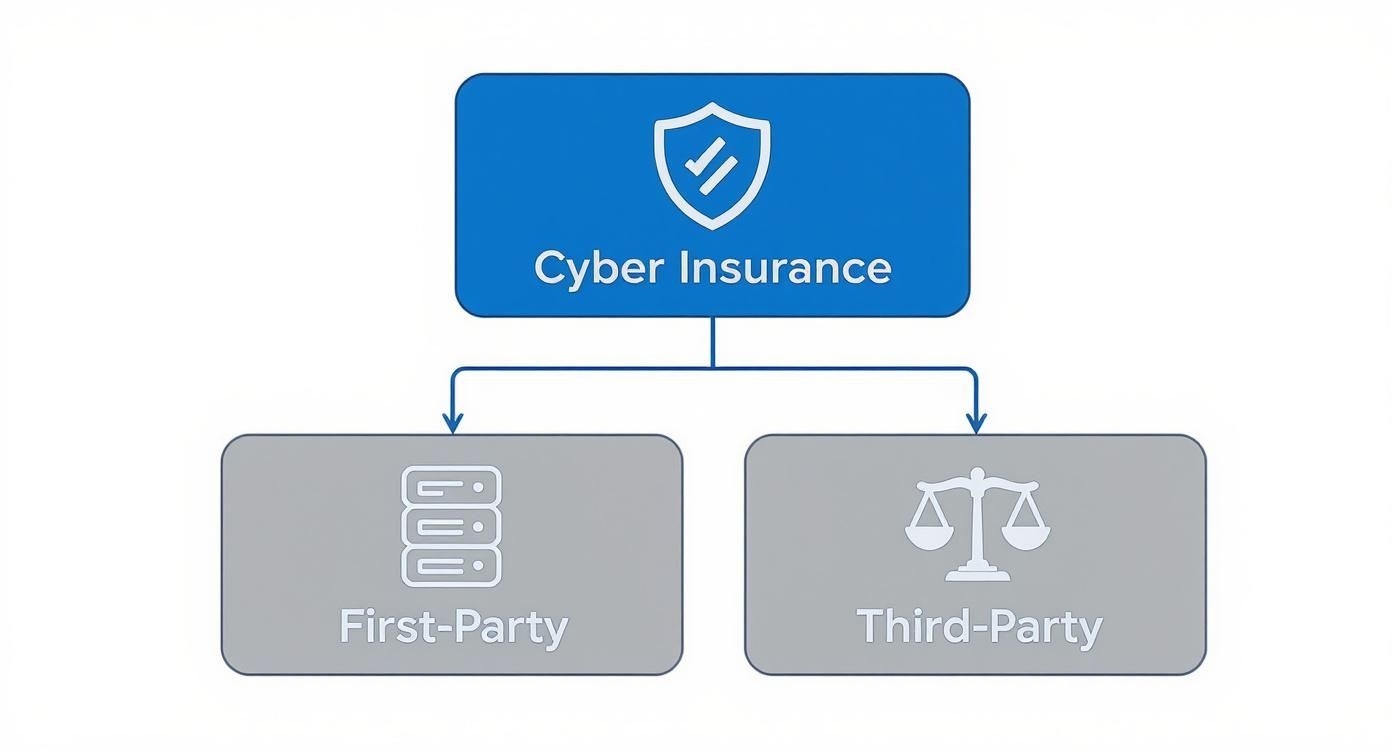

Cyber liability insurance is specifically designed to shield your business from the crippling financial and reputational fallout of a digital attack. It's not just one type of protection; it's a two-pronged defense.

Imagine your online store gets hit with ransomware. Your first-party coverage kicks in immediately, helping you pay for forensic experts to figure out what happened, cover the costs of notifying your customers, and even handle a potential ransom payment.

Now, what if angry customers sue you because their personal information was leaked? That's where third-party coverage comes in, handling the hefty legal defense fees, settlements, and potential regulatory fines.

This structure creates a comprehensive shield for your business.

- First-party coverage handles your direct losses: forensic investigations, notifying customers, credit monitoring services, and business interruption costs.

- Third-party coverage deals with your liability to others: legal defense, court judgments, and fines from regulators.

“A cyber incident is like a spark in dry brush—it starts small but can engulf your entire business before you know it.”

Most business owners are shocked by how fast the costs of a breach pile up. A single incident can easily lead to bills of $50,000 to $100,000 from forensic vendors alone, and that's before you even start talking about legal fees or lost revenue. The reputational hit is just as damaging; 73% of organizations that lost data also reported significant brand damage that hurt customer loyalty.

Who Needs This Protection?

The short answer? Everyone. From a solo consultant to a massive corporation, if you use technology, you're a target.

Let's look at a few examples:

- A one-person consulting firm stores sensitive client strategies on a laptop.

- A local retail chain processes thousands of credit card transactions every day.

- A large manufacturing plant depends on an interconnected network of machinery to keep production lines running.

While their vulnerabilities might look different on the surface, they all share a fundamental exposure to digital risk that could shut them down.

The demand for this protection is skyrocketing for a reason. The global cyber liability insurance market was valued at around $15.3 billion and is on track to hit $16.3 billion as businesses race to keep up with evolving threats. You can discover more insights about market growth from industry leaders.

The image below, taken from Wikipedia, breaks down the core components you'll find in most cyber insurance policies.

This gives you a great visual overview of how policies are structured, clearly splitting the coverage between direct losses (first-party) and liabilities to others (third-party). Understanding this distinction is key to managing your risk effectively.

Building a Resilient Defense

Getting a cyber liability policy is a crucial first step, but it's not the whole story. The smartest businesses pair their insurance with proactive security measures. Think of it like having both a great alarm system and strong locks on your doors.

By implementing controls like regular vulnerability scanning, ongoing employee training on phishing, and practicing your incident response plan, you create a much tougher defense. This dual approach means you not only have the financial backing to recover from an attack but also the strength to prevent many of them in the first place.

The key takeaway is simple: every business, no matter its size, needs cyber liability insurance. When you combine the right coverage with strong security habits and expert guidance from a partner like Wexford Insurance Solutions, you build a truly resilient operation.

What Your Cyber Policy Actually Covers

A cyber liability insurance policy can feel a bit overwhelming at first, but it really boils down to two core types of protection. I like to think of it like the aftermath of a car accident. One part of your insurance covers the cost to repair your car, and the other part covers the damage you caused to someone else's car and their potential injuries.

That same logic applies here. A single cyber incident creates a messy, expensive ripple effect. To handle it all, your policy is split into two distinct categories: First-Party and Third-Party coverage. Each is designed to tackle a different set of financial headaches that pop up after a breach.

This infographic breaks down that fundamental structure, showing how one policy provides a two-pronged defense against both your internal recovery costs and your external legal liabilities.

As you can see, a truly solid policy isn’t just about one type of protection. It’s a balanced strategy that shields your business from every financial angle of a cyber attack.

First-Party Coverage: Protecting Your Own Assets

Think of first-party coverage as your company's dedicated cyber emergency fund. It’s all about reimbursing you for the direct, out-of-pocket expenses your business faces in the immediate aftermath of an attack. When your network is down or your data is locked, this is the part of the policy that helps you get back up and running.

Let's say a hacker deploys ransomware and encrypts your entire server. The clock starts ticking, and the costs start mounting immediately. First-party coverage is built for exactly these kinds of urgent, internal crises.

It typically helps pay for things like:

- Incident Response: Hiring the high-priced digital forensics experts needed to figure out how the breach happened and what was stolen.

- Business Interruption: If an attack grinds your operations to a halt, this helps replace the income you’re losing while your systems are down.

- Data Recovery: This covers the cost of rebuilding your systems, restoring data from backups, or even recreating lost information from scratch.

- Cyber Extortion: If you're forced to deal with a ransomware demand, this can cover the costs of negotiation and even the payment itself.

A cyber incident isn't a single event but a long chain of expensive reactions. First-party coverage is what stops that chain reaction from bankrupting your business.

Without it, a company is stuck paying for all of this out of pocket—a devastating financial hit that many businesses, especially smaller ones, just can't absorb.

Third-Party Coverage: Shielding You From Lawsuits

While first-party coverage is busy managing your internal mess, third-party coverage steps in to handle the external fallout. This is your liability shield. It defends you when an incident at your company causes harm to others, whether they’re customers, partners, or even your own employees.

If a data breach exposes your customers' sensitive information, you're almost certainly going to face angry clients, regulatory investigations, and probably lawsuits. This is where third-party protection is absolutely critical.

This coverage usually includes:

- Legal Defense Costs: It pays for the attorneys and court fees when you get sued by people affected by the breach.

- Settlements and Judgments: If you lose a lawsuit or agree to a settlement, this helps cover those massive costs.

- Regulatory Fines: This can help pay the steep penalties from regulators like HIPAA or under GDPR if the breach violated compliance rules.

- Notification and Credit Monitoring: It covers the legally required—and expensive—process of notifying every affected individual and offering them credit monitoring services.

To really dig into what’s possible, you can learn more about what cyber insurance covers in detail in our comprehensive guide.

First-Party vs Third-Party Cyber Coverage

To make the distinction crystal clear, here’s a simple table comparing the two. Think of First-Party as "for me" and Third-Party as "for them."

| Coverage Type | What It Protects | Common Claim Scenarios |

|---|---|---|

| First-Party | Your business's direct financial losses and assets. | A ransomware attack locks your files, and you need to pay for experts and lost income. |

| Third-Party | Your liability to others harmed by the incident. | A data breach exposes client credit card numbers, and you're sued for negligence and fined by regulators for non-compliance. |

Both sides of the coin are essential. Having only one is like trying to protect a castle by only guarding the front gate while leaving the back wide open. You need a complete defense to be truly secure.

Understanding Policy Exclusions And Costs

Shopping for cyber liability coverage? It pays to dig into the fine print. A policy that skips flood coverage when you live near a river sounds absurd—but that’s exactly how an exclusion for a common risk can cripple your protection.

Insurance premiums aren’t pulled out of a hat. Underwriters treat your organization like a driver’s history. Strong security practices are rewarded with lower rates, while a shaky setup drives premiums up.

Common Policy Exclusions To Watch For

Exclusions are the lines your insurer won’t cross. Spotting them early prevents nasty surprises when you submit a claim.

- Acts of War: If a hack is tied to a nation-state or military operation, this exclusion often kicks in.

- Failure to Maintain Security Standards: Skipping vital patches or ignoring known vulnerabilities can void your claim.

- Pre-Existing Breaches: Any incident that began before your policy’s effective date is off the table.

- Bodily Injury Or Property Damage: Standard cyber plans focus on data loss. Physical injuries and tangible property fall under general liability.

An exclusion is a policy’s way of saying, “This specific risk is on you.” By recognizing these gaps, you can shore up defenses or seek add-ons.

Key Factors That Drive Your Premiums

Your final quote depends on a handful of core elements. Insurers dig deep into each to gauge how risky your business looks.

- Industry And Business Size: Sectors like healthcare and finance face steeper rates due to high-value data. Your annual revenue also signals potential loss magnitude.

- Security Posture: Think of this as your cyber “driving record.” Robust controls—MFA, employee training, endpoint detection, incident response plans—all earn you points.

- Coverage Limits And Deductibles: Higher limits push premiums up. Choosing a larger deductible brings rates down—but means more out-of-pocket if you file.

To see how these numbers play out in real markets, refer to the table below.

Recent Premium Changes By Region

Below is a snapshot of the percentage decline in cyber insurance premiums across different markets.

| Region | Rate Change |

|---|---|

| North America | -6% |

| Europe | -8% |

| Asia Pacific | -5% |

| Latin America | -4% |

These figures underline a broader trend: as businesses tighten security, insurers can lower their rates with confidence.

Global rates slid by 6% in one quarter, and some areas saw even steeper drops. For a deeper dive into the latest market shifts, check out Cyber Insurance Market Trends. To understand what your business might pay, explore our guide on Understanding Cyber Liability Insurance Cost. Focusing on these elements gives you leverage to secure better terms.

How to Choose the Right Policy and Limits

Picking the right cyber liability insurance can feel like trying to solve a puzzle in the dark. The options seem endless, and the language is full of technical jargon that can make anyone’s head spin. But with a methodical approach, you can turn a confusing task into a clear-cut process that lands you the right protection for your business.

It’s tempting to shop for insurance based on price, but that’s a huge mistake. The real worth of a policy is buried in the details—the insuring agreements, the definitions, and, most importantly, the exclusions. A cheaper plan might have a loophole that leaves you completely exposed right when you need the coverage most.

Deconstruct the Policy Language

Before you can even begin to compare policies, you have to get a handle on what they’re actually saying. Think of it like learning the basic grammar of a new language. You have to look past the shiny summary page and get into the weeds of the full policy document.

Pay close attention to a few critical terms, as how they’re defined can dramatically change your coverage. Insurers often define these differently, which can create dangerous gaps in your protection.

Here are a few terms to put under the microscope:

- Retroactive Date: This is the starting line for your coverage. A policy with no retroactive date is the gold standard, as it can cover incidents that happened in the past but were only discovered today.

- Sublimits: Watch out for these. A policy might boast a $1 million overall limit but then quietly cap coverage for something like a ransomware payment at just $100,000. That fine print can leave you holding a massive bill.

- Definition of a "Claim": You want this to be as broad as possible. A good policy will define a claim to include not just lawsuits but also written demands and regulatory investigations, getting your legal defense team involved sooner.

- Choice of Counsel: Does the policy force you to use one of their pre-approved law firms, or do you have the flexibility to choose your own? In the middle of a high-stakes legal fight, this can make all the difference.

"The most expensive cyber policy is the one that doesn't pay out when you need it. Scrutinizing the details isn't just due diligence; it's fundamental to securing real protection."

Determine Your Ideal Coverage Limits

Okay, so you understand the jargon. Now for the million-dollar question: how much coverage do you actually need? This isn't about pulling a number out of thin air. It’s about making a calculated decision based on your unique risk profile. Buying too little coverage leaves you vulnerable, while buying too much is a waste of money.

A great starting point is to estimate your potential financial hit from a data breach. A simple way to do this is to figure out the cost per lost record. Industry studies often place the cost of a breach at hundreds of dollars for each compromised record, once you factor in things like customer notifications, credit monitoring, and potential fines. If your business holds 50,000 customer records, you can see how quickly the potential liability skyrockets.

When you're setting your limits, ask yourself these questions:

- Data Sensitivity: What kind of data are you storing? If it's highly sensitive information like medical records (PHI) or credit card details (PCI), the potential for massive regulatory fines and lawsuits is much higher, demanding beefier limits.

- Contractual Requirements: Do your clients or business partners require you to carry a certain amount of cyber insurance? Checking your contracts is a must—failing to meet these requirements could put you in breach.

- Business Interruption Exposure: If a cyber attack brought your operations to a grinding halt, how long could you stay afloat? You need to know your daily revenue and fixed costs to accurately estimate the financial damage of being offline.

Thinking through these areas is critical. To get a truly structured look at your vulnerabilities, performing a detailed insurance gap analysis is the best way to see where your current coverage falls short. By aligning your policy limits with your real-world risks, you ensure you're not guessing about your protection. That's the foundation of smart risk management.

Navigating the Claims Process Like a Pro

When the alarm bells sound on your security systems, every second feels like a countdown. A calm, step-by-step response can switch you from scrambling to in control.

Your cyber liability insurance isn’t just a policy—it’s a playbook full of actionable moves. From the moment you file a claim, you gain instant access to breach attorneys, forensic analysts, and PR experts who know how to steady the ship.

The First Critical Steps After an Incident

Once you suspect something’s wrong, the clock starts ticking. These opening moves set the tone for your claim and recovery.

- Report the incident immediately. Policies come with strict notification windows and missing one can void coverage.

- Engage approved vendors. Insurers preselect forensic firms and legal counsel for a reason. Straying off list = risk of a denied claim.

- Document everything. Every log entry, timestamp, and email may become key evidence.

"A cyber claim is a collaborative effort, not a solo mission. Your insurer, legal team, and forensic experts form a triangle of trust designed to navigate the crisis efficiently and minimize the damage."

Proactive Strategies Make All the Difference

The best response doesn’t begin during a breach—it starts long before. Practicing your plan until it feels instinctive can turn panic into precision.

- Incident Response Plan (IRP): A dynamic guide that outlines roles, contacts, and procedures.

- Tabletop exercises: Simulated scenarios where leadership walks through the IRP, spots weak points, and refines tactics.

These steps pay off handsomely:

- Faster Response: Defined roles eliminate guesswork at critical moments.

- Stronger Claim: A documented and tested plan shows your insurer you take risk seriously.

- Reduced Panic: Familiar routines keep teams focused when tension is high.

Take the first step today by exploring our in-depth data breach response plan. With a solid foundation in place, your cyber liability policy becomes not just a financial backstop but a finely tuned recovery machine.

Putting Cyber Insurance to the Test: Real-World Scenarios

Policy language can feel a bit abstract. The real "aha!" moment comes when you see how cyber insurance actually works during a crisis. Let's walk through a couple of real-world scenarios to show how the right coverage can be the one thing that stands between a manageable incident and a complete disaster.

These aren't just hypotheticals; they're based on the kinds of threats businesses face every single day. Seeing how the different parts of a policy kick in—from first-party recovery to third-party liability—makes it much easier to understand why this coverage is so critical.

Case Study 1: The Client Data Breach

Picture a mid-sized accounting firm, the kind of place that built its reputation on trust and confidentiality. They walk in on a Monday to discover their network has been breached. A hacker didn't just get in; they got out with sensitive financial records for dozens of high-profile clients and are threatening to leak everything if a ransom isn't paid.

Chaos erupts. Clients are calling, panicked and angry. The firm’s reputation, built painstakingly over decades, is suddenly on the line. This is a classic third-party liability nightmare—the primary damage has been done to others, and now the legal and financial fallout is coming for the firm.

This is exactly when their cyber liability insurance policy proves its worth.

- Legal Defense: The policy’s third-party coverage immediately kicks in, paying to hire a top-tier law firm specializing in data breaches. This team starts managing the legal storm and responding to lawsuits from affected clients.

- Regulatory Fines: When government regulators investigate and levy a $250,000 fine for compliance failures, the policy covers it.

- Settlement Costs: To prevent long, public, and reputation-destroying court battles, the firm agrees to settle with the hardest-hit clients. The insurance policy covers the $1.2 million in settlement payments.

Without that policy, the legal fees and settlements alone would have likely bankrupted the firm. The coverage didn't just pay the bills; it gave them access to the expert crisis team they needed to survive.

Case Study 2: The Supply Chain Shutdown

Now, let’s look at a different kind of company—a fast-growing tech startup. Their entire operation depends on a critical piece of third-party software. One day, a sophisticated cyber attack doesn't target the startup but instead takes down their software vendor. Instantly, the startup’s platform goes dark. They're dead in the water, completely unable to help their customers.

This isn't a data breach, but it's just as devastating. Every hour they're offline means more lost revenue and more customers heading for the exit. This is where first-party coverage, specifically for business interruption, becomes the hero.

The startup’s cyber policy had a strong business interruption clause that was triggered almost immediately.

A business can survive a data leak, but it cannot survive without revenue. Business interruption coverage is the financial lifeline that keeps you afloat when a cyber event shuts you down.

The policy paid out the startup’s lost net profits for the 10 days their platform was down, preventing a total cash flow crisis. It also covered the extra expenses they racked up getting a temporary solution online to keep their customers from leaving.

For a deeper dive into how different policies respond to various attacks, check out our collection of cyber insurance claims examples. It’s worth noting that ransomware is a massive driver here, accounting for about 60% of the value of large cyber claims in a recent period. You can discover more insights about cyber risk trends at Allianz.com to get a clearer picture of the threats on the horizon.

Frequently Asked Questions

When it comes to cyber liability insurance, it's natural to have questions. This isn't your standard business policy, after all. Let's break down some of the most common things we hear from clients trying to get a handle on it.

What Does Cyber Insurance Actually Do?

Think of it like a financial and operational lifeline after a digital disaster. If your business gets hit by a ransomware attack or a data breach, this policy kicks in to cover the often staggering costs.

It’s not just about a single payout. It provides the funds for forensic experts to figure out what happened, legal teams to navigate the fallout, and even PR firms to manage your reputation. The goal is to help you recover and get back to business without going bankrupt in the process.

First-Party vs. Third-Party Coverage

This is probably the most important distinction to understand, and it's simpler than it sounds.

- First-party coverage is for your direct financial hits. This covers the immediate costs you face, like paying for data restoration, covering lost income while your systems are down (business interruption), or even paying a ransom demand. It’s all about fixing your own house.

- Third-party coverage protects you when other people come after you for damages. If a client's data was stolen from your servers and they sue you, this part of the policy covers your legal defense, settlements, and potential regulatory fines. It’s about the damage that spills over to others.

What Are the Biggest Factors Influencing My Premium?

Insurance carriers are essentially betting on your digital security, so they look at a few key things to set your price. Your industry is a big one; a healthcare provider with sensitive patient records faces different risks than a small construction company.

They'll also look at your annual revenue and the sheer number of sensitive records you handle. But the real game-changer is your security posture. Do you use multi-factor authentication? Do you train your employees on phishing? Having strong, documented security controls is the single best way to lower your premium.

What Should I Do Immediately After a Breach?

The first few hours are absolutely critical. If you even suspect a breach, here are the first three things you must do:

- Call your insurer—immediately. Your policy will have a specific timeframe for reporting a claim. Don't wait.

- Contact the breach coach or legal counsel listed in your policy. The biggest mistake businesses make is hiring their own IT firm or lawyer. Your policy requires you to use their approved experts.

- Don't touch anything. It's tempting to reboot servers or delete suspicious files, but that can destroy the digital evidence investigators need. Isolate the affected systems if you can, but don't try to "clean up."

Navigating these complexities is where having an expert in your corner makes all the difference. Wexford Insurance Solutions doesn't just sell policies; we help you build a cyber defense plan that truly fits your risk profile, ensuring you have the right protection when it matters most.

You can start the conversation and get a personalized quote today at https://www.wexfordis.com.

what is loss control in insurance: cut risks, save moneyDecoding General Liability Insurance Cost

what is loss control in insurance: cut risks, save moneyDecoding General Liability Insurance Cost