Picture this: a fire sweeps through your older commercial property. It’s a nightmare, but you have insurance, so you start the claims process expecting to be made whole. Then the city inspector shows up and delivers a bombshell. Because of new building codes, the undamaged portion of your building can’t be saved. It has to be torn down, too.

Suddenly, you’re on the hook for costs your standard policy was never designed to cover. It’s a financially devastating scenario, and unfortunately, it’s an all-too-common reality for property owners.

The Costly Gap Hiding in Your Property Insurance

Most people assume that if their building is damaged, their insurance policy will pay to put things back exactly as they were. This belief overlooks a critical and incredibly expensive detail: local building codes, zoning laws, and city ordinances are constantly changing. This gap between what your policy covers and what the city demands can leave you with a massive, unexpected bill.

This is precisely where ordinance or law coverage steps in. Think of it as a crucial endorsement that covers the extra costs of demolition and construction forced on you by modern building regulations after you’ve had a claim.

Why Standard Policies Fall Short

Your basic property insurance policy has a straightforward job: it pays to repair or replace the damaged part of your building using similar materials and quality. What it absolutely does not cover are the external legal mandates that can skyrocket your rebuilding expenses.

Let’s walk through a real-world example. A fire damages 55% of your commercial building, which was originally constructed back in the 1980s. Your policy pays to fix the fire damage, no problem. But then the local municipality enforces its rule:

Any building that sustains more than 50% damage must be completely demolished and rebuilt to meet modern standards for electrical, plumbing, accessibility (like ADA compliance), and energy efficiency.

Without ordinance or law coverage, you’re left paying out-of-pocket for two huge expenses:

- The cost to demolish the perfectly fine, undamaged 45% of your building.

- The increased cost to rebuild the entire structure to today's much stricter—and far more expensive—building codes.

This isn't some rare, fringe scenario; it’s standard practice in cities and towns all across the country. The financial shortfall can easily stretch into the tens, or even hundreds, of thousands of dollars. It can turn what should be a manageable insurance claim into a potential financial catastrophe.

The first step is figuring out if you have this exposure. A detailed insurance gap analysis is the best way to uncover whether your current policy leaves you vulnerable to this often-overlooked risk. This vital coverage bridges that gap, acting as a financial safety net to protect your investment from the costly mandates of local law.

Breaking Down The Three Pillars Of Protection

Ordinance or Law coverage isn't just one big, vague safety net. It’s better to think of it as a specialized toolkit with three distinct parts, each designed to solve a very specific—and very expensive—problem that pops up when local building codes and your insurance policy don't see eye to eye.

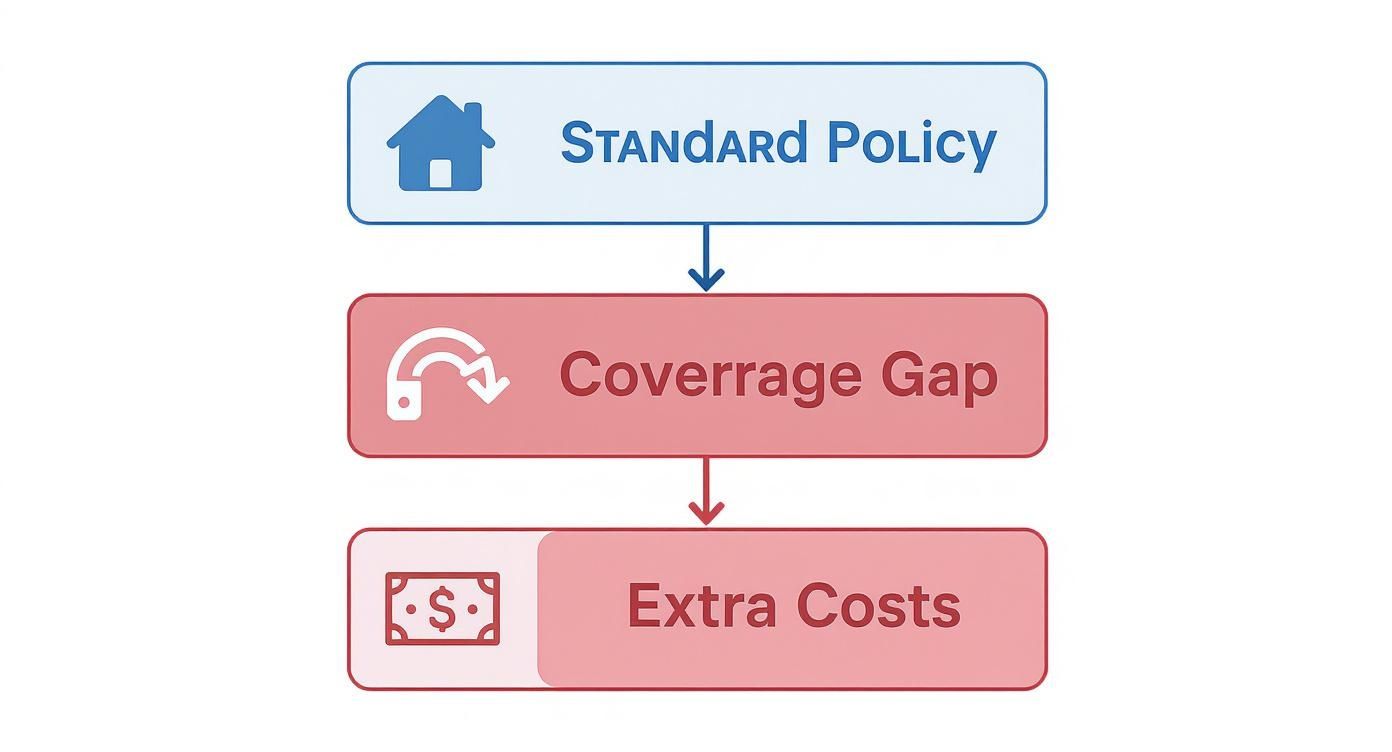

To really get why your standard policy often comes up short, have a look at this flowchart. It shows just how quickly a coverage gap can appear, leaving a property owner with a mountain of unexpected costs.

As you can see, relying on a standard policy alone is a risky bet. When building codes force you to do more than just simple repairs, you're left exposed. Each pillar of Ordinance or Law coverage is built to fill a specific piece of that gap.

Coverage A: Loss to the Undamaged Portion

This is, without a doubt, the most crucial and misunderstood part of the coverage. Let's say a fire rips through your building. Your standard policy will pay to fix the burned parts, no problem. But what happens when the local building inspector shows up and tells you the undamaged part has to come down, too?

It’s a surprisingly common scenario. Imagine a fire destroys 60% of your property. The other 40% is untouched. But a local ordinance states that if more than 50% of a structure is damaged, the entire thing must be demolished. Suddenly, you're being forced to lose 40% of a perfectly good building, and your standard policy won't pay a dime for that loss.

That’s where Coverage A steps in. It’s designed specifically to cover the value of the undamaged portion of your building that you're now legally required to tear down. It’s your defense against a partial disaster turning into a total financial loss.

Coverage B: Demolition Cost

Following that same fire example, now you’re legally on the hook to demolish the remaining 40% of your building. Who pays for that? Demolition is expensive work, involving heavy machinery and lots of labor, and it's an expense standard policies almost always exclude.

Coverage B is the answer. This part of the policy provides the cash needed to tear down and haul away the debris from that undamaged section. Without it, you'd be paying for the entire demolition job out of pocket, right after you've already suffered a major loss.

Coverage C: Increased Cost of Construction

This is the final piece of the puzzle. It deals with the extra costs of rebuilding your property to meet today's building codes, which are almost certainly stricter than when your property was first built. Codes are always evolving—requiring better materials, modern electrical and plumbing, and new safety features like fire sprinklers or hurricane-resistant windows.

Increased Cost of Construction coverage pays for the expensive gap between rebuilding your property as it was and rebuilding it how the law demands it be built now. It specifically covers the extra expenses you run into when complying with updated architectural zoning requirements or building codes.

This coverage works alongside your policy's replacement cost coverage, but it is not the same thing. Your main policy limit helps rebuild the structure, but Coverage C gives you the extra funds needed to satisfy modern legal standards without having to drain your own savings.

To help bring these concepts together, here's a simple breakdown of how the three parts work:

The Three Pillars of Ordinance or Law Coverage

| Coverage Component | What It Covers | Simple Example |

|---|---|---|

| A: Undamaged Portion | The value of the part of your building that wasn't damaged but must be torn down due to a local law. | A fire damages 60% of your building. A law says anything over 50% damaged must be fully demolished. This covers the loss of the "good" 40%. |

| B: Demolition Cost | The cost to actually tear down and remove the debris from that undamaged portion of the building. | You need to hire a crew and equipment to demolish that remaining 40% of the building. This coverage pays their bill. |

| C: Increased Cost of Construction | The extra cost to rebuild your property to meet current, more expensive building codes. | The new building code requires a sprinkler system that your old building didn't have. This pays for the sprinkler installation. |

Together, these three coverages create a comprehensive shield. They ensure that a single disaster doesn't snowball into a financial catastrophe because of the expensive and complex demands of local laws.

Real-World Scenarios: Where This Coverage Truly Matters

It's one thing to talk about insurance in the abstract, but the real "aha!" moment comes when you see how Ordinance or Law coverage plays out in real life. These aren't wild, once-in-a-lifetime events; they are surprisingly common situations that can financially cripple a property owner who isn't prepared.

Let’s walk through three different scenarios that paint a clear picture of why this coverage is less of a simple add-on and more of a critical financial shield.

In each of these stories, without this specific protection, the property owner would have been left with a massive bill that their standard insurance policy would flat-out refuse to cover.

Example 1: The Historic Downtown Commercial Building

Picture this: you own a beautiful, century-old brick building in a charming historic downtown area. A fierce storm causes a city water main to burst, flooding your ground floor and damaging about 40% of the structure, including parts of the foundation. Your standard property policy kicks in to cover the water damage repair. Great. But that's just the beginning.

When the city inspector comes out, they flag a new ordinance passed just a few years ago. The law states that any historic building undergoing major repairs must upgrade its entire electrical and plumbing systems to meet modern codes—think fire safety and water conservation.

Suddenly, a manageable repair job has ballooned into a full-scale renovation. You're now on the hook for tearing out perfectly functional wiring and pipes in the undamaged 60% of your building. This is a huge, unexpected cost that your standard policy won't touch.

This is a classic ordinance or law claim. The initial covered loss—the flood—triggered a much larger, legally mandated project. Without the right coverage, you’d be paying for that entire electrical and plumbing overhaul straight out of your own pocket.

Here’s how the three parts of Ordinance or Law coverage would save you:

- Coverage C (Increased Cost of Construction) pays for the expensive new electrical and plumbing systems required by the updated code.

- Coverage B (Demolition Cost) covers the cost of tearing out the old, outdated systems from the untouched parts of the building.

- Coverage A (Loss to the Undamaged Portion) reimburses you for the value of the old but perfectly good wiring and pipes you were forced to destroy.

Example 2: The Multi-Family Apartment Complex

Next, let's look at a three-story apartment complex built in the 1980s. A small kitchen fire breaks out in one unit. It's contained quickly, but the fire department’s response brings the whole building under the microscope of the local fire marshal.

During the inspection, the marshal points to a recent city ordinance: all multi-family buildings over two stories must have a modern, hardwired sprinkler system. Your building was grandfathered in when the law passed, but the fire has changed everything. Now, you’re required to comply.

Your property policy will pay to fix the fire damage in that one apartment, but it will not pay the $150,000+ it costs to retrofit the other 23 apartments and common areas with sprinklers. That mandatory upgrade is now your problem. It's a perfect example of how a relatively minor incident can trigger a financially devastating code-enforcement issue. This is especially tricky when it involves roofs; you can get a sense of the complexities by reading about how to handle a hail damage roof insurance claim.

Example 3: The Coastal Family Home

Finally, imagine a family home on the coast that’s been passed down through generations. A hurricane rolls through. While the house itself stands strong, the storm surge inundates the first floor, causing damage equal to about 45% of the home's total value. The damage is bad, but it seems fixable.

Here’s the catch. Since the last big storm, new building regulations have been put in place for the flood zone. The new rule says that any home in the area sustaining damage over 25% of its value must be elevated to the new Base Flood Elevation (BFE). In practical terms, this means the entire house has to be physically lifted onto 12-foot concrete pilings.

Your standard homeowner's policy will cover the water damage repairs, but it specifically excludes the astronomical cost of jacking up the house and building a new foundation. Without Ordinance or Law coverage, your family would face an impossible choice: come up with six figures to elevate the home, or walk away from the property. This coverage is the only thing designed to fund a massive, legally required project like this.

How to Read the Fine Print on Your Policy

Figuring out if you have ordinance or law coverage—and how much—means you have to do a little digging. It's almost never listed on the front page of your policy, and what’s often included by default is just enough to create a false sense of security.

Most standard property policies, both for homes and businesses, toss in a small, pre-packaged amount of this coverage. Think of it as a token gesture. It’s often just 10% of your main building limit and usually only applies to the increased cost of construction (Coverage C). For an older building in a town with tough building codes, that's a drop in the bucket.

To get the real-deal protection you actually need, you have to add a specific endorsement to your policy. An endorsement is simply an add-on that modifies your base coverage. For commercial properties, the gold standard is the ISO CP 04 05 Ordinance or Law Coverage form. This lets you buy separate, dedicated limits for all three pillars of protection, which is exactly what you want.

Locating Your Current Coverage

The first step is to grab your policy and flip to the declarations page. You're looking for a line item that specifically says "Ordinance or Law." If you don't see it listed as a separate endorsement with its own limits, your coverage is probably that tiny, default amount buried deep in the policy's fine print.

If you do find it, you need to look closer at the details:

- Is there one limit or three? A single, combined limit is a red flag. It means all three coverages (A, B, and C) have to share the same pot of money, and it can run out fast.

- What are the limits? Are they a flat dollar amount or just a percentage of your total building coverage?

- Are any parts missing? Some basic endorsements only cover the increased cost to rebuild, leaving you holding the bag for demolition and the loss of the undamaged part of your building.

Getting answers to these questions is the first step toward closing what could be a massive financial gap. For a deeper dive into decoding your documents, check out our complete guide on how to read an insurance policy.

Why Sub-Limits Matter Greatly

When you add a proper ordinance or law endorsement, you’ll set individual limits for each part of the coverage. This is where people often make a critical mistake—they underfund one or more of the pillars, not realizing how the costs can stack up.

Let's say your building is insured for $1 million. A well-structured endorsement might look like this:

- Coverage A (Undamaged Portion): $1 million (you always want this to match your building limit)

- Coverage B (Demolition Cost): $150,000

- Coverage C (Increased Construction): $250,000

Now, imagine a fire tears through and destroys 60% of your building. A local ordinance could easily trigger a total loss, forcing you to tear down the remaining 40%. In this case, Coverage A would pay you for the value of that "undamaged" portion ($400,000). Coverage B would cover the demolition bill, and Coverage C would help pay for the mandatory code upgrades during the rebuild. Without properly funded, separate limits, one huge demolition bill could wipe out the money you needed for everything else.

An underfunded sub-limit is nearly as dangerous as having no coverage at all. It provides a false sense of security while leaving you exposed to significant out-of-pocket costs when you need the protection most.

The insurance world is always shifting to keep up with new risks, from climate events to new construction regulations. According to the Baker McKenzie global disputes forecast, businesses in developed countries like Canada (44%) and the UK (35%) are bracing for more disputes tied to changing regulations. This just goes to show how quickly the rules can change, making it more critical than ever to understand exactly what your policy does—and doesn't—cover.

Common Myths That Can Cost You Thousands

It's easy to get bad information about ordinance or law coverage. Unfortunately, a lot of what people think they know is flat-out wrong, and these misconceptions can leave you with a devastating financial blind spot after a disaster.

Let's walk through some of the most dangerous myths I hear from clients. Getting these straight is the first step to making sure you're actually protected.

Myth 1: My Property Is New, So I'm Safe

This is probably the most common and costly mistake a property owner can make. The thinking goes, "My building was built recently, so it must be up to code." And on the day the certificate of occupancy was issued, that was true. But it’s not true forever.

Building codes are constantly changing. They get updated to reflect new safety research, stronger materials, and evolving weather risks. A building constructed just five years ago might not meet today's much stricter standards for things like hurricane-rated windows, electrical systems, or fire suppression.

So, if you have a partial loss—say, a fire damages 40% of your building—the city could legally require you to rebuild that section to today's far more expensive standards. Without the right coverage, that cost is all on you.

Myth 2: My Standard Policy Already Covers Code Upgrades

Almost every standard property policy has a small, built-in provision for increased construction costs, usually just 10% of your building limit. This is a classic case of a little knowledge being a dangerous thing. It creates a false sense of security, making owners believe they're covered when they are actually staring down a massive shortfall.

Think about it: For a $1 million building, your standard policy might give you $100,000 for code upgrades. That sounds like a lot, but a single mandated upgrade, like installing a commercial fire sprinkler system, can eat up that entire amount. It leaves nothing for demolition costs or the value of the undamaged part of the building you might be forced to tear down.

That built-in clause is rarely, if ever, enough to handle a real-world claim where ordinances come into play. It's a safety net with gaping holes.

What This Coverage Will Not Do

It’s just as important to know what this coverage doesn't do. This endorsement isn't a blank check for every extra expense you might run into during a rebuild.

Here are a few critical things it generally will not cover:

- Pre-existing Violations: If your property had code violations before the damage happened, this coverage won't pay the fines or costs to fix them.

- Pollutant Cleanup: The cost to remove or clean up hazardous materials like asbestos or lead paint is typically excluded unless you have a separate, specific endorsement for it.

- Upgrades to Other Properties: The coverage only applies to the specific building that was damaged. It won’t pay to upgrade other undamaged buildings you own, even if they're on the same lot.

- Voluntary Upgrades: If you decide to add some nice-to-have features during the rebuild that aren't required by code, you'll be paying for those yourself.

This is a complex area where insurance and local law intersect, which is why having an expert on your side is so important. In the U.S. alone, a market of over 1.3 million lawyers is increasingly focused on specialized areas like regulatory compliance. You can find more insights about the evolving legal landscape on Clio.com. Knowing what is and isn't covered allows you to have a much smarter conversation with your agent to make sure your policy is truly buttoned up.

How to Get the Right Coverage for Your Property

Knowing the risks is half the battle. The other half is taking the right steps to protect your investment. Getting proper ordinance or law coverage isn't just about ticking a box; it's about sitting down with a professional and doing a thoughtful risk assessment to head off a potential financial disaster down the road.

The last place you want to discover a gaping hole in your policy is in the middle of a claim.

This means you need to have a very specific, detailed conversation with your insurance agent. Vague promises won’t cut it. You need to come armed with the right questions to make sure the protection you're getting is what your property actually needs, especially if you own an older building or live in an area where building codes change often.

Key Questions for Your Insurance Agent

Before you sign on the dotted line or renew your policy, it's time for a direct chat about this specific coverage. Use these questions as a starting point to make sure nothing gets missed.

- How do my property's age and location affect my risk? A good local agent will know the area's regulations and can give you some real, valuable insight.

- Does my quote include all three parts—Coverages A, B, and C? You need to explicitly confirm you have coverage for the undamaged portion, demolition, and the increased cost of construction.

- What are the limits for each individual part? Be wary of a single, shared limit. That's a huge red flag and a common way people end up underinsured.

- Are my limits a percentage or a flat dollar amount? In many situations, a flat dollar amount gives you more reliable and sufficient protection.

Partnering with an experienced broker isn't just a good idea—it's essential. They live and breathe this stuff, understand the nuances of local building codes, and can properly assess your property's unique risks to ensure your limits can handle a worst-case scenario.

Dealing with repairs after a major loss involves more than just your insurance company. You'll need skilled professionals to ensure all the work is up to code. When it comes to your roof, selecting a reliable roofing contractor is a critical part of a successful recovery.

Ultimately, picking the right coverage is fundamental to your financial well-being. If you'd like a broader look at what makes a solid policy, our guide on how to choose home insurance offers some great additional context. Here at Wexford, our team is ready to sit down with you, review your current policies, find any potential gaps, and build the ordinance or law coverage that lets you sleep at night.

Answering Your Top Questions

Even after you've got the basics down, a few practical questions always pop up about ordinance or law coverage. Let's tackle some of the most common ones we hear from clients.

How Much Coverage Do I Actually Need?

There’s no magic number here, but a solid rule of thumb is to start with 25% to 50% of your property's total replacement cost value for the Increased Cost of Construction portion (Coverage C). If you own an older building, especially one in a town known for strict or constantly changing codes, you'll want to lean toward the higher end of that range—or even push past it.

The right amount really comes down to a few key things:

- The age of your property: The older it is, the more likely it is to be out of step with today's building codes.

- Your local laws: Some municipalities have what's known as the "50% rule," where if a building is more than 50% damaged, they can legally require you to tear the whole thing down and start over.

- What upgrades might cost: Think about what it would take to bring your property up to snuff today. We're talking about things like modern sprinkler systems, new wiring and plumbing, or even meeting new hurricane-readiness standards.

Does This Cover Me If I Just Want to Make Upgrades?

That’s a great question, but the answer is no. This coverage is specifically for upgrades you are forced to make by law after a covered claim.

If you decide during the rebuild that you want to put in a gourmet kitchen or upgrade to triple-pane windows when the code only requires double-pane, those extra costs are on you. The trigger for this coverage is a legal mandate, not your wish list. It's there to save you from expenses you have no choice but to pay.

Is This Going to Be Expensive?

You'd be surprised. For the incredible amount of financial protection it offers, ordinance or law coverage is usually very affordable. For most homeowners, a good endorsement costs less than a couple of fancy coffees each month. On a commercial policy, the premium is a tiny sliver of the six-figure bill you could be staring at without it.

When you think about how a single uncovered claim could be financially devastating, the cost of this endorsement is one of the smartest investments you can make. It’s a low-cost solution to a high-stakes problem.

Isn't This the Same as "Increased Cost of Construction"?

This is a critical point and a common source of confusion. "Increased Cost of Construction" (Coverage C) is just one piece of the puzzle. Many standard policies throw in a very small, often default, amount of Coverage C, which can give property owners a dangerous false sense of security.

A true, comprehensive ordinance or law endorsement bundles all three essential parts:

- Coverage A: Loss to the Undamaged Portion of the Building

- Coverage B: Demolition Cost

- Coverage C: Increased Cost of Construction

Relying only on that small, built-in Coverage C is like having a lifeboat with no oars. It might keep you afloat for a minute, but it's not going to get you safely to shore.

Trying to make sense of local building codes and dense insurance policies can feel overwhelming. At Wexford Insurance Solutions, our job is to dig into these details and make sure you're properly protected. Don't wait until you have a claim to find out you have a major gap in your coverage. Get in touch with us for a complete policy review at https://www.wexfordis.com today.

Your Ultimate Fleet Vehicle Maintenance Checklist for 2025Your Ultimate 2025 Home Maintenance Checklist: 10 Key Tasks

Your Ultimate Fleet Vehicle Maintenance Checklist for 2025Your Ultimate 2025 Home Maintenance Checklist: 10 Key Tasks