As a professional painter, you know that the secret to a great finish lies in the prep work. You tape, you cover, you protect. General liability insurance is the most important piece of prep work you can do for your business itself. Think of it as the ultimate drop cloth—the non-negotiable safeguard against the spills and mishaps that can threaten everything you've built.

Your First Line of Defense in the Painting Business

You take immense pride in your work. Every edge is crisp, every coat is even. But no matter how skilled or careful you are, accidents are a part of the job. A ladder slips and dents a custom-built cabinet. A paint tray gets knocked over, ruining an expensive antique rug. A client walks through the work area and trips over a cord.

These are the real-world moments when general liability insurance for painters proves its worth. It’s the bedrock of your protection, shielding you from the devastating financial fallout of an unexpected claim. Without it, one small mistake could force you to pay thousands out of pocket, jeopardizing the future of your company.

Core Protections for Painting Contractors

This isn't just a compliance document; it's an active defense against the risks you face every single day. The need for this coverage is more recognized than ever. The global painting contractor insurance market was valued at around $5.2 billion in 2024, and it's projected to nearly double in the next ten years. This isn't surprising—it reflects a growing understanding of just how vulnerable a painting business can be to claims of property damage or injury. You can learn more about the painting contractor insurance market and its projected growth to see the full picture.

So, what does this policy actually do for you on the job? Let’s break down the essential protections.

This table shows the fundamental ways a general liability policy has your back.

Core Protections in a Painter's General Liability Policy

| Coverage Area | What It Protects You From | Real-World Painter Scenario |

|---|---|---|

| Bodily Injury | Medical and legal costs if a third party (like a client or visitor) gets hurt because of your business operations. | A homeowner trips over your extension cord while you're working in their living room, resulting in a broken wrist and medical bills. |

| Property Damage | Costs to repair or replace a third party's property that you or your employees accidentally damage. | While spray painting exterior trim, a gust of wind causes overspray to drift onto the client’s car, requiring a professional repaint. |

| Personal & Advertising Injury | Claims of libel, slander, copyright infringement, or misappropriation of advertising ideas in your marketing materials. | You use a photo of a beautifully painted home from a competitor's website in your new brochure without permission, leading to a lawsuit. |

Each of these coverages addresses a specific, common risk that painters encounter, making this policy a true cornerstone of your business’s financial safety.

What Your Painter Insurance Actually Covers

Let's be honest, insurance policies can feel like they're written in another language. But your general liability insurance isn't some abstract concept; it's a practical shield designed to protect you from the kind of expensive accidents that can happen on any job site.

We're going to break down exactly what this coverage does for you, using real-world scenarios you've probably worried about yourself.

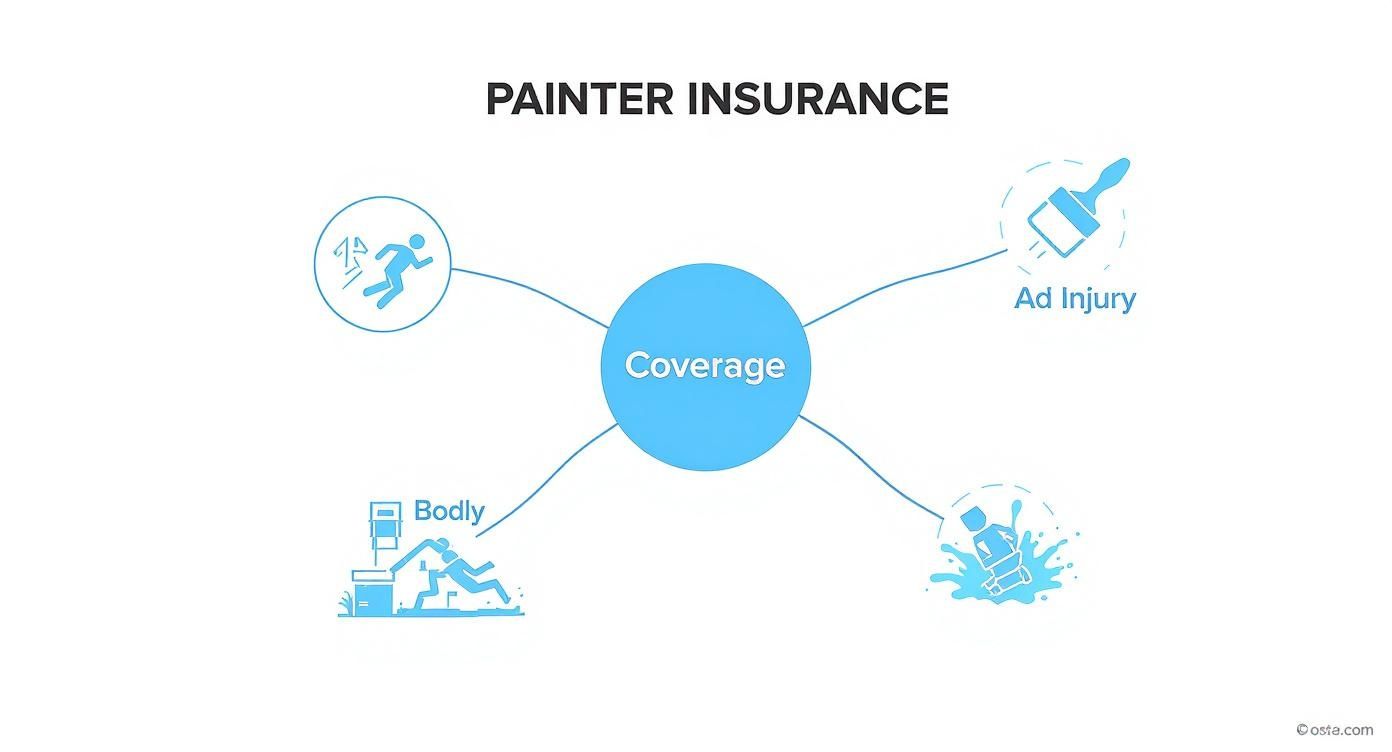

Think of your policy as having a few core functions, each designed to handle a different kind of risk: Bodily Injury, Property Damage, and Personal & Advertising Injury. They might sound a bit formal, but what they cover is anything but.

This isn't just a "nice to have" policy. General liability is part of a global casualty insurance market valued at around $290.5 billion in 2024. With lawsuits on the rise, experts predict that businesses will pay about $330 billion in general liability premiums worldwide by 2025. This shows just how critical this protection has become for skilled professionals like you.

Bodily Injury: When a Simple Trip Becomes a Major Problem

This part of your policy kicks in if a third party gets hurt because of your work. We’re not talking about your employees here—that’s a job for workers' compensation. This is for your client, their kids, a neighbor, or anyone else who might get injured on your job site.

Here’s a classic example:

You're in the middle of painting a two-story foyer. You’ve got drop cloths down and a ladder set up. The homeowner pops in to see how it’s going, but they don’t notice a ladder leg tucked under a cloth. They trip and fracture their wrist.

Without insurance, you could be on the hook for their medical bills, time off work, and any legal fees if they sue. A general liability policy steps in to handle those costs up to your limit, making sure one clumsy moment doesn't tank your business. For a deeper look at how this works, check out our guide on what commercial general liability is.

Property Damage: The Dreaded Overspray Incident

This is probably the most common claim painters face. Property damage coverage is your safety net for those "oops" moments. It pays to fix or replace someone else's property that you or your crew accidentally damage.

We’ve all seen it happen:

You're spraying the exterior of a house on what seems like a perfectly still day. A surprise gust of wind kicks up and carries a fine mist of paint over to the neighbor’s brand-new black SUV. Now that car has a speckled finish that’s going to cost thousands to fix.

This is exactly what general liability is for. Your policy would cover the cost of getting the neighbor's car restored, saving you a huge out-of-pocket expense and a very awkward conversation.

Personal And Advertising Injury: More Than Just Physical Accidents

This coverage is less about ladders and paint cans and more about protecting your business's reputation. It deals with claims like slander, libel, or copyright infringement in your marketing.

Think about this modern-day scenario:

You’re trying to build up your online portfolio and find a gorgeous photo of a professionally painted kitchen online. You post it on your company's social media, making it seem like your work. The original photographer finds out and sues you for copyright infringement.

Your policy can help cover the legal costs to defend yourself and pay for any settlement, protecting you from a simple marketing mistake.

Completed Operations: Your Work Is Done, But Your Protection Isn't

One of the most valuable, and often misunderstood, parts of a general liability policy is completed operations coverage. This protects you from claims that arise after you’ve packed up your gear and left the job.

Imagine you just finished refinishing a client's kitchen cabinets. A few weeks later, one of the cabinet doors you re-installed falls off because a screw wasn't tightened enough. It crashes down, smashing a countertop full of expensive dishes.

Even though you weren't there, the damage was a direct result of your work. Completed operations coverage is designed for exactly this, ensuring you're protected long after the paint is dry.

Decoding Your Policy Limits and Premium Costs

Let's talk about the dollars and cents of your general liability insurance. It might seem a little confusing at first, but once you get the hang of a few core ideas, you'll be able to look at a policy and know exactly what you're getting for your money.

Think of your policy limits and premiums as the financial guardrails for your business. They set the boundaries for how much your insurer will pay out if something goes wrong. If you don't understand them, you could find yourself dangerously underinsured right when you need that protection the most.

Per-Occurrence vs. Aggregate Limits: The Bucket Analogy

Every general liability policy boils down to two critical numbers: the per-occurrence limit and the aggregate limit. The easiest way to wrap your head around this is to think of your policy as a big bucket of water.

This bucket holds all the water you have for the entire year to put out "fires"—in this case, insurance claims.

-

Per-Occurrence Limit: This is how much water you can pour on any single fire. If you have a $1 million per-occurrence limit, that’s the absolute maximum your insurance will pay for one incident. Say a gust of wind causes overspray that damages a half-dozen cars in a parking lot; this limit caps the payout for that entire event.

-

Aggregate Limit: This is the total amount of water in your bucket for the whole year. A common aggregate limit is $2 million. No matter how many different claims you have, once you’ve used up that $2 million, the bucket is empty until your policy renews.

You’ll often see this written as "$1M/$2M," meaning you have a $1 million per-occurrence limit and a $2 million total aggregate limit. This is a solid, industry-standard starting point for most painting contractors.

These limits are what backstop the core coverages your policy provides.

As you can see, these limits are the financial safety net for claims involving property damage, injuries, and even advertising mistakes.

What Goes Into Your Premium?

So, how is your premium—the price you pay—actually calculated? It's not a one-size-fits-all number. Insurers look at your specific business to figure out how much risk they're taking on.

Several key factors will move the needle on your final cost:

- Your Location: Operating in a state known for high-cost lawsuits or frequent weather-related claims will almost always mean higher premiums.

- Size of Your Crew: It’s simple math—the more painters you have on the job, the higher the chances of an accident. Your total payroll is a huge factor here.

- The Work You Do: A crew that only paints residential interiors has a very different risk profile than a team that works on high-rise exteriors with scaffolding or performs specialty work like lead paint removal.

- Your Track Record: A clean claims history is your best friend. It tells insurers you run a tight ship, which often translates to better pricing.

- The Limits You Choose: It stands to reason that a policy with higher limits (like $2M/$4M instead of $1M/$2M) will cost more, since the insurer is on the hook for a potentially larger payout.

Knowing what drives your premium is the first step to controlling it. The insurance market itself also plays a big role. After a few years of steep price jumps, rate increases began to level off for contractors in 2024, generally landing in the 4–10% range. What's changed is that insurers are now laser-focused on a contractor's safety protocols. If you can show you have a strong risk management program, you're in a much better position to get a competitive quote.

Keeping your insurance costs in check is just one piece of the puzzle. It’s also a good idea to stay sharp on your overall business finances. For example, knowing how to properly manage expenses can unlock major savings elsewhere; this is a great guide on how to reduce your tax bill by finding deductions many people miss. If you want to dive deeper into what you can expect to pay, we break it all down in our guide to https://wexfordis.com/2025/11/20/general-liability-insurance-cost/.

Building Your Complete Insurance Toolkit

Your general liability policy is the multi-tool of your insurance world—it's versatile, essential, and you’ll use it on almost every job. But just as you wouldn't use a multi-tool to rebuild an engine, this policy isn't designed to handle every single risk your painting business faces. To be truly protected, you need to build a complete toolkit with specialized policies that address specific vulnerabilities.

Thinking that general liability covers everything is one of the most common—and most expensive—mistakes a painter can make. It's absolutely critical to understand what it doesn't cover so you can plug those gaps. Certain incidents just fall outside its scope, leaving your business wide open if you haven't planned ahead.

What General Liability Leaves Out

A standard policy has very clear boundaries. It’s built to protect you from claims made by third parties, like a client tripping over your drop cloth or a visitor getting paint overspray on their car. It doesn't, however, cover issues directly related to your own team, the quality of your work, or your business property.

Key exclusions you'll almost always find include:

- Employee Injuries: If one of your painters falls from a ladder and breaks an arm, general liability won’t touch their medical bills or lost wages. That's the specific job of Workers' Compensation insurance.

- Damage to Your Own Equipment: Picture this: your brand-new, expensive paint sprayer gets stolen from a job site overnight. A general liability policy won't pay a dime to replace it. For that, you need a different tool, like Inland Marine or a Business Owner's Policy.

- Faulty Workmanship: This one is a biggie. Let's say you use the wrong type of paint on an exterior, and it starts peeling off the walls a month later. The cost to redo that entire job comes straight out of your pocket. General liability covers accidental damage, not the quality of your professional work itself.

- Auto Accidents in Your Work Vehicle: If you rear-end someone while driving your work van—even if you’re just heading to a job site—your general liability policy offers zero protection. Only a Commercial Auto policy will cover that kind of liability.

Assembling the Right Policies for Your Business

Understanding these exclusions isn't about finding flaws in your policy; it's about smart business planning. Each gap can be filled with a specific type of insurance, creating a comprehensive shield around your operations. Think of it as adding specialized wrenches and screwdrivers to your toolkit instead of trying to do everything with one device.

To help you see how it all fits together, here’s a quick breakdown of the essential insurance policies that work alongside your general liability coverage.

Essential Insurance Policies for a Painting Contractor

This table clearly compares the purpose of each policy and how they team up to protect your business from different angles.

| Insurance Policy | Its Primary Job | You Need It When You… |

|---|---|---|

| Workers' Compensation | Covers medical expenses and lost wages for employees injured on the job. | …hire your first employee. Most states legally require it. |

| Commercial Auto | Protects you from liability and property damage claims if your work vehicle is in an accident. | …use any vehicle for business purposes, like transporting supplies or crew members. |

| Business Owner's Policy (BOP) | Bundles general liability and commercial property insurance into one package, often at a lower cost. | …own or rent a physical office/shop and have tools and equipment to protect. |

| Umbrella Insurance | Provides an extra layer of liability protection that kicks in after your other policy limits are exhausted. | …take on large commercial jobs or have significant personal assets to protect from a major lawsuit. |

A Business Owner's Policy (BOP) is often a great starting point for many painting contractors. It conveniently combines protection for client accidents (general liability) with coverage for your own gear (commercial property).

Building out this full toolkit ensures you're prepared for whatever a project throws at you. For those looking to safeguard against truly catastrophic claims, understanding your high-limit options is key. You can explore the nuances between excess liability and umbrella insurance in our detailed guide to see which is right for your business.

Ultimately, the goal is to have a seamless protection plan where each policy knows its role, leaving no part of your business vulnerable.

How to Get the Right Insurance for Your Painting Business

Getting the right general liability insurance for your painting business shouldn't be a headache. Think of it like a four-step project, just like prepping a room for that perfect finish.

When you break it down into manageable stages, you take the guesswork out of the equation. This simple approach will help you make a confident, well-informed decision to protect your company's future.

Step 1: Pinpoint Your Business Risks

Before you can get the right coverage, you need a crystal-clear picture of what you're actually protecting against. No two painting businesses are exactly alike, and the specific work you do dictates your insurance needs.

Start by asking yourself a few simple questions:

- What's our bread and butter? Residential interior jobs have completely different risks than large-scale commercial exteriors that require scaffolding.

- Do we use subcontractors? Bringing in subs adds another layer of liability you'll need to account for in your policy.

- Do we tackle high-risk jobs? Things like lead paint abatement or working at serious heights mean you'll need much stronger coverage.

A solid risk assessment is your blueprint. It helps you zero in on what your policy absolutely must cover, so you don't overpay for things you don't need or—even worse—leave a massive vulnerability wide open.

Step 2: Get Your Paperwork in Order

Once you've mapped out your risks, the next move is to gather your documents. Insurance providers need specific details to give you an accurate quote, and having everything ready to go makes the whole process faster and smoother.

You'll generally need to have these items on hand:

- Your business license and federal tax ID number (EIN).

- Clear records of your annual revenue and payroll.

- A full list of all the services you offer.

- Details on any past insurance claims your business has filed.

Being prepared shows insurers you're organized and professional, which can only work in your favor when they're underwriting your policy.

Having your information organized is half the battle. It allows an insurance broker to quickly and accurately shop the market on your behalf, finding the most competitive options available without frustrating delays.

Step 3: Compare Quotes Like a Pro

Getting a few different quotes is smart, but remember that the lowest price isn't always the best value. A cheap policy with huge coverage gaps can end up costing you a fortune down the road. You have to look past the premium and dig into what each policy actually covers.

Pay close attention to the policy limits, deductibles, and any specific exclusions that could affect your jobs. This is where having an expert in your corner really pays off. A knowledgeable insurance broker acts as your guide, helping you decipher the fine print and compare your options apples-to-apples. They're trained to spot red flags you might miss.

To see what a difference this partnership can make, check out our guide on how to choose an insurance broker who understands your business. Working with a professional ensures your final decision is based on total value, not just the sticker price.

Your Certificate of Insurance: The Key to Bigger Jobs

It’s easy to look at a Certificate of Insurance (COI) and see nothing more than a boring piece of paper. But in the painting business, that single document is one of the most powerful tools you have. Don't think of it as paperwork; think of it as your professional passport. It unlocks bigger, better-paying projects and builds immediate trust with clients.

At its core, a COI is just a one-page snapshot proving you have active general liability insurance for painters. It neatly lays out your policy limits, coverage dates, and who your insurance provider is. It’s the quickest, cleanest way to show a potential client or general contractor that you’re a pro who is serious about managing risk.

Why Your COI Is a Deal-Maker

For a lot of clients, especially on the commercial side, seeing your COI isn't a "nice-to-have"—it's a hard requirement before they'll even talk business. It tells them you run a legitimate, responsible company that's prepared for the unexpected.

Here's why this document is so critical for landing jobs:

- Winning Commercial Bids: Forget about bidding on commercial projects or working with general contractors without one. They'll ask for your COI right out of the gate. No certificate, no job. It's that black and white.

- Giving Homeowners Peace of Mind: Smart homeowners have heard horror stories about uninsured contractors. When you proactively show them your COI, you instantly erase their biggest worry and stand out from the competition.

- Meeting Contractual Requirements: If you're painting in a commercial building or for a property management company, their own contracts and leases almost always require vendors to carry and prove a certain level of insurance.

Think of it this way: a client is trusting you with their most valuable asset, whether it's their home or their business. Your COI is the tangible proof that you have a major insurance company backing you up if an accident happens.

Getting your hands on a COI is usually fast and simple. Just call or email your insurance agent and tell them who needs it. To really understand every line item on that form, check out our guide on what is a Certificate of Insurance.

Understanding "Additional Insured" Status

Sooner or later, a client or general contractor is going to ask to be named as an "additional insured" on your policy. This might sound like a huge, complicated request, but it’s a totally normal part of the business.

When you add someone as an additional insured, you’re simply extending your liability coverage to protect them, but only for claims that arise directly from your painting work.

For example, if a client’s customer trips over your drop cloth and decides to sue everyone in sight—you, the client, the building owner—your policy would step in to defend the client, too. Agreeing to this shows you understand how professional projects work and that you’re ready for the big leagues.

Got Questions? We’ve Got Answers.

When you're digging into the nitty-gritty of general liability insurance for painters, a few practical, real-world questions always pop up. Getting straight answers is the final piece of the puzzle, making sure you can walk onto any job site with total confidence.

Let’s break down some of the most common questions we hear from painting pros just like you.

"I'm a Solo Painter. Do I Really Need Insurance?"

Yes, 100%. Flying solo doesn’t mean you’re flying without risk. In fact, it means every bit of that risk lands squarely on your shoulders.

Think about it: one slip-up—a bit of overspray on a client's antique furniture or a ladder scuffing a priceless hardwood floor—could put your personal savings and the future of your business on the line. Besides, most clients worth their salt will ask for proof of insurance before they even let you tape the baseboards, no matter how big or small your operation is.

"What Happens If a Claim is Bigger Than My Policy Limit?"

This is a scenario no business owner wants to face. If a claim blows past your policy limits, you’re on the hook for the rest, paid directly out of your pocket.

Let's say a court awards a $1.5 million judgment against you, but your policy tops out at $1 million per occurrence. You'd have to find a way to cover that extra $500,000. To avoid this nightmare, many painters, especially those tackling bigger commercial jobs or with significant assets to protect, add an Umbrella policy. It's an extra layer of liability protection for when things go really wrong.

An Umbrella policy is like a backup generator for your insurance. It only kicks in when your main policy’s limits are totally exhausted, providing a critical safety net against those massive, business-ending claims.

"How Fast Can I Get a Certificate of Insurance?"

Getting a Certificate of Insurance (COI) is usually quick and painless. As soon as your policy is active, just ask your agent. Most of the time, you can have it in your hands—or your client's inbox—the very same day, often within just a few minutes or hours.

This speed is a game-changer when a last-minute job opportunity comes up and the client needs to see proof of your coverage right away.

"Are My Subcontractors Covered Under My Policy?"

This is a big one: generally, no. Your general liability policy covers the work done by you and your direct employees (your W-2 crew). It almost never extends to the independent contractors or subcontractors you bring on for a job.

The right way to handle this is to require every single subcontractor to give you their own COI, listing your business as an "additional insured." This simple step makes their insurance policy the first line of defense if they're the ones who cause an accident, protecting your business and your bottom line.

Working through these details is always easier with a trusted partner in your corner. The team at Wexford Insurance Solutions is here to give you clear answers and help you find the perfect coverage for your painting business. Start your quote today at https://www.wexfordis.com.

What Does a Business Owners Policy Cover? A Clear GuideWhat Is a Premium Audit for Business Insurance

What Does a Business Owners Policy Cover? A Clear GuideWhat Is a Premium Audit for Business Insurance