A waiver of subrogation is a powerful, yet often misunderstood, clause in a contract. It's essentially a pre-emptive agreement between two parties to let their insurance companies handle losses, preventing the insurers from suing each other to recover money after a claim.

Think of it as a financial peace treaty. It protects business relationships by stopping costly, finger-pointing legal battles before they can even start.

Decoding the Waiver of Subrogation Concept

To really get what a waiver of subrogation does, we first have to talk about subrogation itself. In the insurance world, subrogation is the legal right your insurer has to "step into your shoes" and sue a third party that caused a loss they paid you for. It's how insurance companies hold the at-fault party accountable and get their money back.

Here's a simple example: a delivery driver accidentally backs their truck into your warehouse, causing $50,000 in damage. Your property insurance pays you to make the repairs. Thanks to subrogation, your insurer can then turn around and sue the delivery company to recover that $50,000. They're acting on your behalf to get the money back from the party who was actually responsible.

The Power of a Simple Agreement

A waiver of subrogation flips this entire script. It's a formal agreement where you voluntarily give up your insurer’s right to sue that other party. When this clause is in a contract, you're telling your insurance company, "Hey, even if the other party is at fault for this loss, you can't go after them for reimbursement."

Why on earth would you do that? It seems counterintuitive, right? The main reason is to manage risk and keep business relationships from going sour.

In complex projects like construction or in everyday landlord-tenant agreements, multiple parties are working in close quarters. A waiver of subrogation makes sure that if an accident happens, it’s handled by insurance without creating a hostile, litigious environment that could tank the whole project or relationship.

A waiver of subrogation fundamentally shifts risk, ensuring that a covered loss remains with the insurers rather than turning into a legal dispute between business partners. This pre-emptive agreement is the key to maintaining smooth operations and avoiding relationship-ending lawsuits.

This isn't some new legal gimmick; the concept has deep roots. It became a standard practice after landmark court cases in the 1970s confirmed that waivers were a valid way to stop insurers from fighting each other. Since then, it’s become a cornerstone of commercial contracts and has dramatically cut down on industry disputes.

Why This Matters for Your Contracts

Understanding a waiver of subrogation isn't just about memorizing a definition. It’s about recognizing a critical tool for transferring risk. When you sign a contract that includes one, you’re agreeing to let insurance policies—not the courts—be the final word on who pays for a covered loss.

This is a massive detail that's often buried in the fine print. Being able to spot and understand this clause is a big part of learning https://wexfordis.com/2025/09/06/how-to-read-insurance-policy/.

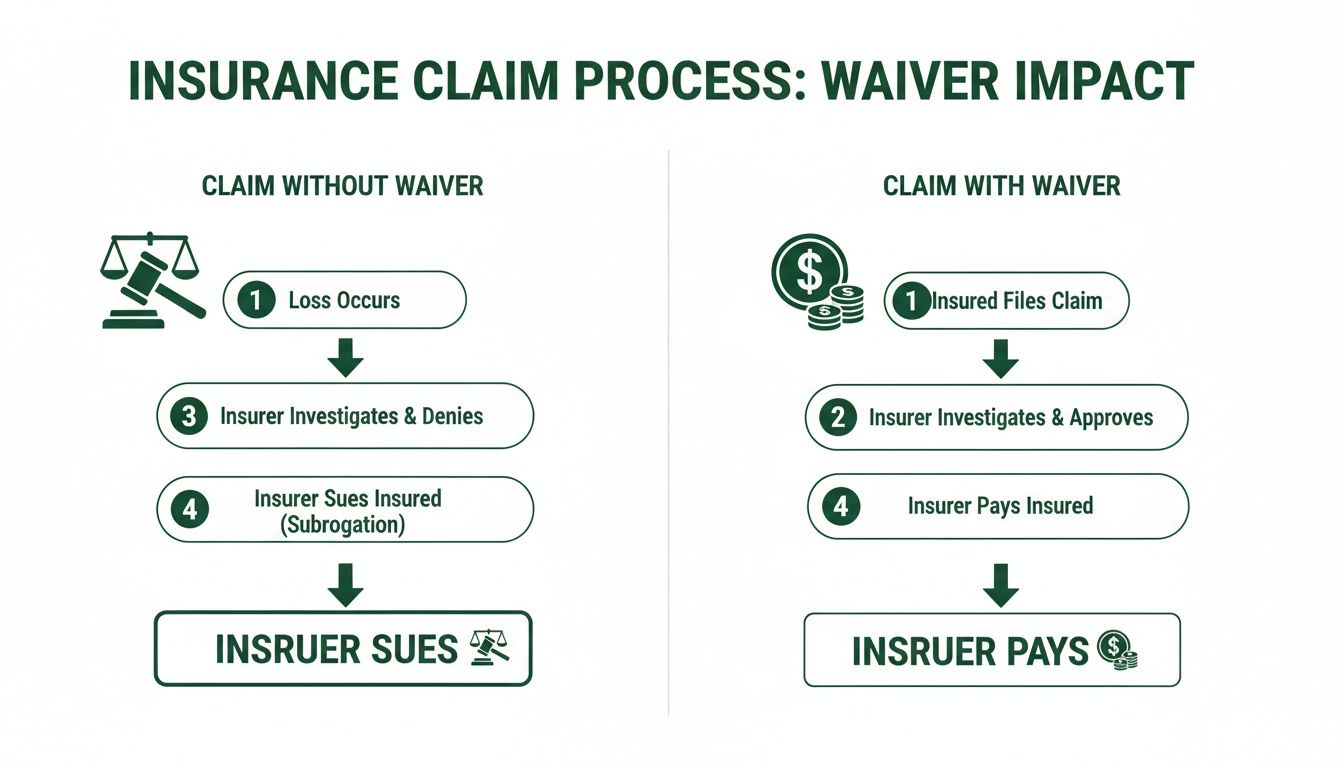

Let's look at how the process changes with and without a waiver in place.

Claim Process With and Without a Waiver of Subrogation

This table breaks down how an insurance claim plays out with a standard subrogation clause versus a waiver. Notice how the waiver stops the cycle of blame and litigation.

| Claim Step | Standard Subrogation Process | Process with a Waiver of Subrogation |

|---|---|---|

| 1. The Incident | A covered loss occurs (e.g., fire, water damage) caused by a third party. | A covered loss occurs (e.g., fire, water damage) caused by a third party. |

| 2. Initial Claim | The insured files a claim with their own insurance company. | The insured files a claim with their own insurance company. |

| 3. Payout | The insurer pays the insured's claim according to the policy terms. | The insurer pays the insured's claim according to the policy terms. |

| 4. Subrogation Action | The insurer sues the at-fault third party to recover the money they paid out. | The insurer's right to sue the at-fault party is blocked by the waiver. |

| 5. Final Outcome | A legal battle ensues between the insurer and the at-fault party. | The insurer absorbs the loss. The claim process ends here. |

As you can see, the waiver brings the process to a clean, final stop, which is exactly why it's so valuable in collaborative business environments.

To get the full picture, it helps to have a little context on broader insurance concepts, like understanding how different insurance systems, like no-fault insurance, operate. Just like a waiver, these systems also change the traditional rules of blame and recovery, showing just how flexible insurance can be in solving real-world business problems.

The Real-World Impact on Business Contracts

A waiver of subrogation isn't just dry legal theory; it's a practical tool that defines who's on the hook for what in countless business agreements. You’ll see this clause everywhere, from massive construction contracts to simple vendor agreements, and it always serves one core purpose: to sidestep expensive legal fights after an insurable loss.

When two parties agree to a waiver, they're essentially deciding ahead of time that their own insurance policies will be the final stop for recovery. It’s a pre-emptive handshake that prevents a covered accident from blowing up into a lawsuit that could poison a valuable business relationship. Let's look at a few places you’ll see this in action.

Construction Projects A Foundation of Trust

Construction sites are a perfect storm of controlled chaos. You've got general contractors, electricians, plumbers, and a dozen other trades all working on top of each other. The chances of one team's mistake damaging another's work are sky-high, which is exactly why a waiver of subrogation is so critical.

Imagine a plumbing sub is installing pipes on the third floor of a new office building. Overnight, a fitting gives way, flooding the two floors below and wrecking the drywall that another contractor just finished putting up.

Without a waiver, the drywall contractor’s insurance company would pay for the repairs and then immediately turn around and sue the plumber to get that money back. That means project delays, legal bills, and a whole lot of bad blood on the job site. But with a waiver in place, the insurer simply pays the claim, and that’s the end of it. The project moves forward.

Commercial Leases Protecting Landlords and Tenants

Waivers of subrogation are standard issue in most commercial leases. They’re there to protect both the landlord and the tenant from getting dragged into court by the other party's insurance carrier, which keeps the relationship stable and predictable.

Picture this: a tenant in a retail space has a small kitchen fire that sets off the sprinkler system. The fire itself is minor, but the water causes significant damage to the building's structure—damage the landlord is responsible for fixing.

The landlord's property insurance steps in to cover the repair costs. If the lease includes a waiver of subrogation, the landlord’s insurer can't sue the tenant to recover its payout, even though the tenant’s faulty equipment started the fire. This keeps the landlord and tenant from becoming legal adversaries. Seeing how waivers function in common documents like rental agreement templates really highlights their practical value.

This flowchart shows the clear fork in the road between a claim with a waiver and one without.

As you can see, the waiver is a stop sign for litigation. It ensures the insurer's payment is the final chapter.

Service and Vendor Agreements

Anytime you bring an outside company onto your property to perform a service, a waiver of subrogation is a smart move. In fact, many businesses won't let a vendor start working until they can prove their insurance policy includes this waiver.

By requiring a waiver of subrogation from vendors, a business ensures that an accident caused by the vendor is handled by the vendor's insurance without creating a legal liability for the business itself. It transfers the ultimate financial responsibility to the correct insurer from the start.

Let’s say a manufacturing company hires an IT consultant to upgrade its server room. While working, the consultant accidentally drops a tool and damages a critical piece of machinery. The manufacturer's commercial general liability policy might cover the immediate damage, but the waiver prevents their insurer from then suing the IT consultant. If you want to get deeper into this type of coverage, check out our guide on what is commercial general liability.

In each of these real-world examples, the waiver of subrogation proves its worth. It’s a contractual tool that keeps business relationships intact by keeping insurance disputes out of the courtroom where they don’t belong.

Weighing the Pros and Cons for Your Business

Agreeing to a waiver of subrogation is a strategic business decision, and it’s all about a clear trade-off. It’s certainly not a one-size-fits-all solution, so understanding both sides of the coin is crucial before you sign on the dotted line. This decision doesn't just affect you; it impacts your insurance carrier, your professional relationships, and your financial risk profile.

For your business, the upside is all about keeping things running smoothly and maintaining good relationships. The downside? It usually shows up on your insurance bill. Let’s break down this balancing act to see how it really impacts your partnerships and your bottom line.

Advantages for Your Business

By far, the biggest win from a waiver of subrogation is protecting your business relationships. When you agree to one, you're essentially taking a potential lawsuit between your insurer and your business partner off the table before it can even start. That’s invaluable for any long-term collaboration.

Here’s what your business really gains:

- Preserves Key Relationships: Nothing sours a partnership like a lawsuit. A waiver prevents that blame game, ensuring that if an accident happens, your insurer simply handles the loss. Business can continue as usual without the finger-pointing and bad blood.

- Fulfills Contractual Obligations: In many fields, especially construction and commercial real estate, a waiver of subrogation isn't just a suggestion—it's a requirement. Having one in your policy makes you eligible to bid on more projects and land more partnerships.

- Avoids Litigation Headaches: Even when your insurer is the one suing, your business gets pulled into the mess. Think depositions, document requests, and endless meetings. A waiver completely sidesteps that logistical nightmare.

This isn't just theory; it works in practice. The widespread adoption of these waivers has statistically lowered litigation rates between business partners by 28% since the 1980s. This shift was heavily influenced by the Insurance Services Office (ISO) standardizing the endorsements that now shape most commercial general liability policies. You can find more detail on how these clauses work in modern policies by checking out property and casualty insurance on fliprogram.com.

Disadvantages for Your Business

While the relationship benefits are clear, they aren't free. The primary drawback of a waiver of subrogation is financial. You’re asking your insurer to absorb more risk without giving them a way to get their money back.

- Higher Insurance Premiums: When you give up your insurer's right to subrogate, you're taking away one of their key tools for cost recovery. To make up for that added risk, they will almost certainly charge a higher premium or a specific fee for the waiver endorsement.

- Potential for Uncovered Claims: A waiver only applies up to your policy limits. If a loss is bigger than what your insurance covers, you could still be on the hook for the rest, and the other party might come after your business directly for the difference.

When you add a waiver of subrogation, you are essentially paying a little more in premiums to purchase a lot more peace of mind and protect your professional network from the fallout of a potential lawsuit.

This premium increase is a critical factor to consider when looking at different insurance options for small business, as the cost has to make sense for the contracts you’re trying to win.

The Insurer's Perspective

From an insurance carrier’s point of view, a waiver is a direct hit to their ability to manage losses. By giving up the right to recover money paid out for a claim, their bottom line is directly affected. This is exactly why they charge more for it—it’s a straightforward calculation of risk versus reward.

But it's not all bad for the insurer. Often, the businesses asking for waivers are more sophisticated and risk-aware, working on larger, more professional projects. By offering these endorsements, insurers can attract and retain stable, long-term clients. In a way, they trade a specific recovery right on one claim for a more predictable and profitable book of business overall.

How to Get a Waiver of Subrogation for Your Policy

Getting a waiver of subrogation is a pretty standard part of doing business, but it's not quite as simple as just ticking a box on a form. It’s a formal request you have to make to your insurance company, and it usually involves some paperwork and a fee. Knowing the ropes can save you from a lot of headaches and delays down the line.

First off, let's be clear about why waivers aren't free. When you ask for one, you're essentially telling your insurer, "Hey, if this other company causes a loss, you can't go after them to get your money back." You’re asking them to give up their right to recover their payout, which naturally increases their risk. To balance that out, they charge a bit extra—either a flat fee or a small percentage added to your premium.

Blanket vs. Specific Waivers

Before you even pick up the phone to call your agent, you need to know which type of waiver you need. There are two main flavors, and they serve different purposes.

-

Specific Waiver: This is sometimes called a "scheduled waiver." It’s tailored for a single, named entity on a specific project. Think of it as a one-off. It’s perfect if you only need a waiver for one contract, but it can become a real administrative chore if you have to get a new one for every client.

-

Blanket Waiver: This one is the "set it and forget it" option. It automatically applies to any party you have a written contract with that requires a waiver. It costs more upfront, but if your business constantly signs contracts demanding waivers, it will save you a massive amount of time and hassle.

So, which one is right for you? A blanket waiver is all about convenience, while a specific waiver is the more budget-friendly choice for isolated projects. It really just comes down to how often your business needs one.

The Step-by-Step Process to Obtain Your Waiver

Getting the waiver added to your policy is a pretty logical process, but you have to pay attention to the details to make sure everything is squared away. Here’s how to do it right.

-

Review Your Contract Immediately: The second you see a "waiver of subrogation" clause in a contract, hit pause. Read that section carefully. You need to know exactly which of your policies it applies to—like General Liability or Workers' Compensation—and the exact legal name of the party it needs to protect.

-

Contact Your Insurance Agent or Broker: Don't sign anything until you've looped in your insurance professional. A good agent is your best friend here; they’ll know if your carrier offers the waiver and can give you a clear idea of the cost. If you’re not confident in your current advisor, our guide on how to choose an insurance broker is a great place to start.

-

Provide All Necessary Information: Your agent is going to need some specific details to get the ball rolling. Be ready to provide the full legal name of the other party, the project name or address, and a copy of the insurance requirements section from your contract.

-

Receive and Confirm the Endorsement: Your insurance company will send over an official endorsement. This is the document that legally adds the waiver to your policy. Don’t just assume you’re covered; wait until you have this paper in hand. Give it a once-over to make sure all the names and details are spot on.

-

Issue an Updated Certificate of Insurance (COI): The last step is providing proof. Your agent will generate a new COI that clearly states the waiver of subrogation is active for the policies you specified. This is the document you'll give to the other party to show you’ve met your obligation.

Following these steps in order keeps things clean and ensures you're not accidentally in breach of contract.

Common Questions About Waivers of Subrogation

Even after you get the hang of waivers of subrogation, some specific questions almost always pop up. It makes sense—this is where insurance policies and legal contracts collide, and the details really matter. Let's clear up some of the most common points of confusion so you can handle your contracts with confidence.

Think of this as your quick-reference guide for the tricky "what ifs" and "how is this different from…" scenarios that business owners run into all the time.

How Is a Waiver of Subrogation Different from Additional Insured Status?

This is easily the question we hear most often. Both are common contract requirements designed to manage risk, but they do completely different jobs. The easiest way to think about it is a shield versus a peace treaty.

-

Additional Insured Status: This is the shield. By adding another party (like your client or landlord) as an additional insured, you are extending your policy to protect them directly. They are now under the umbrella of your coverage for claims related to your work.

-

Waiver of Subrogation: This is the peace treaty. It's an agreement where you promise that your insurance company won't come after the other party to recover money after paying a claim. You’re essentially telling your insurer to stand down and not sue them.

So, one gives them your coverage, while the other prevents your insurer from suing them. They aren't mutually exclusive; in fact, many contracts require both to create a really strong, multi-layered risk protection plan.

Can a Waiver Be Added to a Policy at Any Time?

The short answer is no, not reliably. You should always aim to get the waiver in place before any work starts or a lease is signed. Trying to add it mid-term is a gamble.

While some insurance carriers might allow it, many won't. When they first issued your policy, they calculated your premium based on a specific level of risk. Adding a waiver changes that calculation because it takes away their right to recover money. This last-minute change can lead to delays, denials, or extra fees that put you in a tough spot with your contract.

The best practice is to make the waiver a non-negotiable part of your pre-project checklist. Address it during contract negotiations, not as an afterthought. This ensures you’re compliant from day one and avoids any risk of a claim happening before the waiver is officially active.

What Happens if I Don’t Get a Required Waiver?

Failing to secure a waiver when a contract demands it is a bigger deal than most people realize. It’s not a minor oversight; it's a breach of contract, and the fallout can be incredibly damaging for your business.

Here’s a look at what could happen:

- The Contract Gets Terminated: The other party can legally void the agreement, leaving you without a project or a place to operate.

- You Get Sued Directly: If a loss occurs, you lose a critical layer of protection. Without the waiver, the other party’s insurance company can—and likely will—sue your business directly to recoup their losses.

- Your Own Claim Gets Denied: In a worst-case scenario, your insurer could argue that by not getting the waiver, you failed to uphold your end of the policy agreement, potentially giving them grounds to deny your claim.

This single mistake can unravel the very risk protection you thought the contract and your insurance provided. Always send the insurance requirements section of any new contract to your broker. They can confirm your compliance and provide the necessary proof, often on a what is a certificate of insurance.

Navigating the complexities of insurance requirements is what we do best. If you're facing a contract with confusing clauses or need help securing the right endorsements for your policy, the team at Wexford Insurance Solutions is here to provide the expert guidance you need to protect your business. Contact us today to ensure your coverage is rock-solid at https://www.wexfordis.com.

How to Choose Homeowners Insurance a Guide to Protecting Your HomeBusiness Insurance New York A Small Business Owner's Guide

How to Choose Homeowners Insurance a Guide to Protecting Your HomeBusiness Insurance New York A Small Business Owner's Guide