When you look at an insurance policy, one name stands out above all others: the named insured. Think of this person or company as the policy's official owner. They're the captain of the ship, holding the ultimate authority to steer the coverage.

The named insured is the individual or entity listed right on the declarations page—the policy's cover sheet. They're not just someone covered by the policy; they are in complete control of it.

Defining the Named Insured in Your Policy

Every insurance policy needs a designated owner, whether it's for your car, home, or business. That’s the whole point of the named insured. They have the final say on everything.

This distinction is what separates the policy owner from others who might also be covered, like a family member driving your car or an employee using company equipment. The named insured has the broadest rights but also carries the primary responsibilities. Getting this concept right is the first step in learning how to read your insurance policy and making sure your protection is set up correctly.

Core Rights and Responsibilities

Being the named insured comes with some serious duties. You're the main point of contact for the insurance company and the one calling the shots.

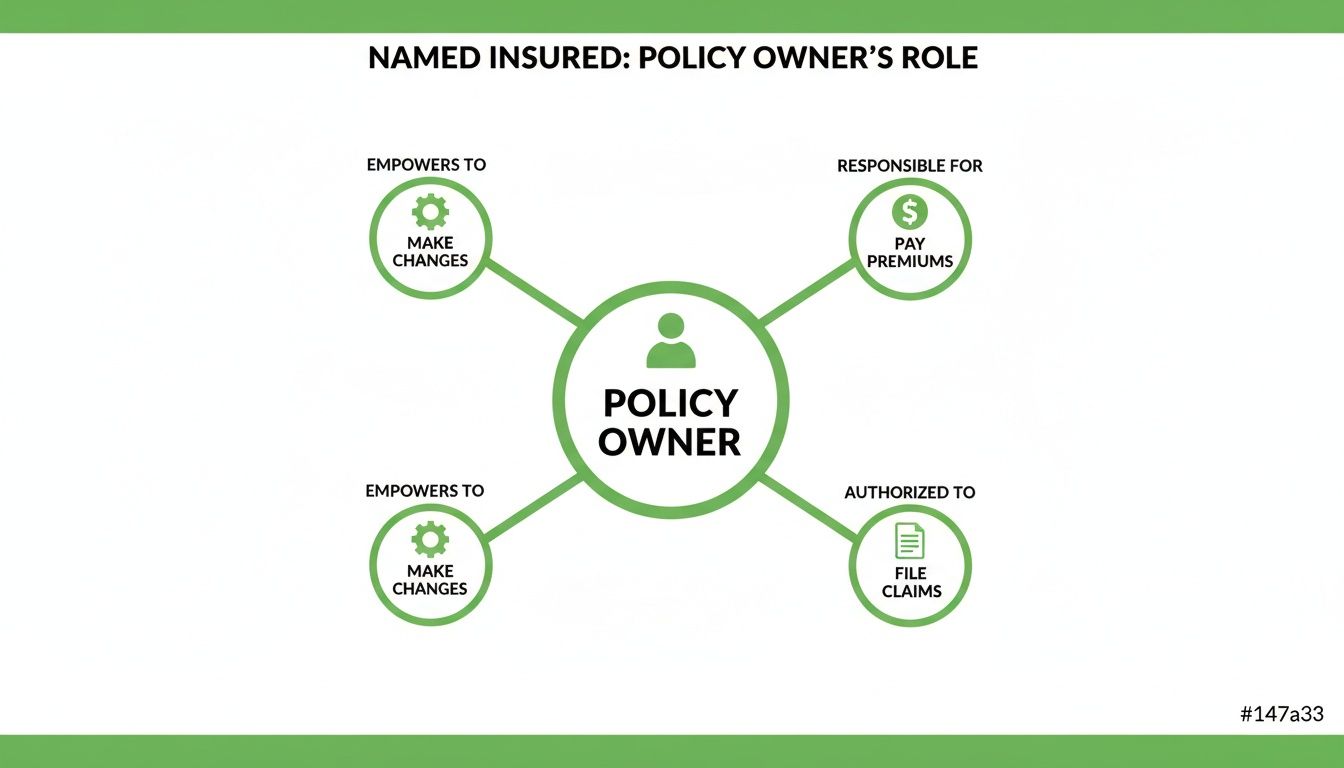

- Managing the Policy: You are the only one who can request changes, whether it’s adjusting coverage limits, adding a new driver, or updating your address.

- Paying the Premiums: The buck stops with you. The responsibility for paying the policy premiums falls squarely on the named insured.

- Filing Claims: You hold the primary right to file claims and negotiate any settlements with the insurance company after a loss.

- Receiving Notices: All official mail—from cancellation warnings to renewal offers—is sent directly to you.

The idea of a named insured has been a bedrock of insurance for over a century, created to clearly define who holds the exclusive rights to a policy. It's a foundational role that brings order to the process and prevents confusion. With the global insurance market hitting $6.9 trillion in premiums by 2023, and named insureds anchoring 85% of commercial policies, its importance is undeniable.

To put it simply, being the named insured grants you specific powers and assigns you key duties. The table below breaks down exactly what that means.

Key Rights and Responsibilities of a Named Insured

| Responsibility or Right | Description | Why It Matters |

|---|---|---|

| Policy Control | The exclusive authority to modify, cancel, or renew the insurance contract. | Prevents unauthorized changes and ensures the primary stakeholder maintains control. |

| Claim Initiation | The primary authority to report a loss and manage the claims process. | Guarantees the policy owner can seek financial recovery without needing others' consent. |

| Official Communication | The designated recipient for all legal notices, bills, and policy updates. | Ensures critical information is delivered to the person responsible for the policy. |

Ultimately, these rights ensure that the person with the most at stake is the one in the driver's seat. It's a simple but powerful system for keeping insurance clear and functional.

Named Insured vs. Additional Insured Explained

If you’ve ever felt tangled up in insurance terms, you’re not alone. One of the most common mix-ups is the difference between a named insured and an additional insured. It sounds technical, but the concept is actually pretty straightforward once you get the hang of it.

Think of it this way: The named insured is the owner of the house. They hold the deed, pay the mortgage, and decide when to repaint the walls. An additional insured is like a long-term tenant. They get a key and can live there, but they can't sell the property or take out a second mortgage on it.

The named insured is the person or entity who owns and controls the insurance policy. They pay the premiums, they're the ones who can make changes, and they're the only ones who can cancel it. The additional insured, on the other hand, is just borrowing a slice of that protection, almost always because a contract or agreement requires it.

The Core Difference in Rights and Control

This distinction in control isn't just semantics—it has a massive impact in the real world. The named insured gets the full benefit of every part of the policy and is the insurance company's main point of contact. An additional insured has a much more limited set of rights, which are almost always tied directly to whatever the named insured is doing for them.

Here’s a classic example: A general contractor hires a plumbing subcontractor for a big project. That contractor will almost certainly demand to be added as an additional insured on the plumber’s general liability policy. This protects the contractor, but only from liability that arises directly from the plumber's work.

So, if a visitor trips over the plumber’s toolbox and decides to sue everyone, the plumber's policy steps in to defend the contractor. But if that same visitor gets hurt because of the contractor's own separate negligence—something that had nothing to do with the plumbing work—the plumber's policy offers zero protection.

Additional insured status is an extension of coverage, not an ownership stake in the policy. It provides a shield against liability stemming from the named insured's actions but does not grant the power to manage or change the policy itself.

A Look at Claims and Payouts

The numbers tell the story. Named insureds have the undisputed right to file claims whenever they need to. For an additional insured, that right is secondary and hinges entirely on the actions of the named party.

In 2022, U.S. general liability claims topped 6.2 million. Named insureds saw their claims succeed 92% of the time, collecting on $78 billion in payouts. Claims filed by additional insureds, however, only succeeded 67% of the time because their coverage is so much more specific and narrow. You can dig deeper into these roles with resources from platforms like TrustLayer.

This diagram breaks down the key powers that belong only to the policy owner.

As you can see, only the named insured—the true policy owner—has the authority to pay premiums, make changes, and file claims.

Proving Your Status

So, how do you prove that you've added someone as an additional insured? This is where a certificate of insurance (COI) comes in.

This document is the official proof of coverage that you provide to the third party who requested it. It’s a snapshot of your policy that confirms who is covered, effectively showing that you've met your contractual obligations. To learn more, check out our guide on what is a certificate of insurance. This simple piece of paper gives clients, landlords, and business partners the peace of mind they need.

Understanding the First Named Insured Role

When an insurance policy lists more than one person or business, a simple question can create a lot of confusion: who's in charge? Who pays the bill? Who gets the important mail from the insurance company? To solve this, policies with multiple named insureds always designate one as the first named insured.

Don't mistake this for a simple matter of whose name is printed first on the declarations page. The first named insured is the official point person for the policy, holding a unique set of administrative powers and responsibilities. Think of them as the captain of the ship, speaking for everyone else on board.

For example, imagine two partners who co-own a company. Both are listed as named insureds, but only one is designated as the first named insured. While a claim might cover both of them, only that one partner has the authority to make changes to the policy, ensuring a clear and efficient line of communication with the insurer.

The Administrative Leader of the Policy

The role of the first named insured is all about administration, but it’s a role with real teeth. This person or entity is trusted to manage the day-to-day nuts and bolts of the insurance contract for every other party covered under it.

This designation is especially critical in the world of commercial insurance, where a single master policy might cover a parent company and several of its subsidiaries. For anyone trying to get a handle on business coverage, learning what a business owner’s policy covers is a fantastic first step in seeing how these different roles all fit together.

So, what exclusive duties fall on their shoulders? The first named insured is the only one who can:

- Receive Official Mail: All policy documents, renewal notices, and other critical communications from the insurer are sent directly to them.

- Pay the Premiums: They are ultimately responsible for making sure the policy premiums get paid on time.

- Authorize Changes: Need to adjust a coverage limit or add a new business location? Only the first named insured has the power to make that call.

- Receive Cancellation Notices: If the insurer cancels the policy, the official notice goes to the first named insured. The other insureds might not be notified directly by the carrier.

By centralizing these duties, the first named insured role prevents administrative chaos. It ensures that critical decisions and communications are handled by a single, designated authority, which is vital for maintaining clear and effective coverage.

This structure just makes everything simpler. The insurance company has a single, reliable contact instead of having to chase down multiple people. It also sidesteps potential disagreements among the other insured parties about who is supposed to be managing the policy, creating a clear chain of command.

Why Your "Named Insured" Status Really Matters

Getting the named insured designation right isn't just a matter of paperwork; it's the bedrock of your financial security. That single line on your policy's declarations page dictates who has the authority to make changes, who gets the check after a claim, and who the insurance company will defend in a lawsuit.

It sounds simple, but a small mistake here can have devastating consequences.

Picture a business partnership where only one partner is listed as the named insured. If a fire wipes out their shared inventory, the partner who isn't listed has no legal right to file a claim or receive a single dollar from the payout. Even if they own half the business, their entire financial stake could be wiped out in an instant.

It's Your Ticket to Claims and Legal Defense

Being the named insured is your all-access pass to the full benefits of your policy. It gives you the primary right to file claims and, maybe even more importantly, access to the insurer's legal team if someone sues you. This is a level of protection that no one else covered under the policy receives.

For you and your family, this could be the difference between your insurer paying to defend you after a major car accident versus you having to find and pay for an attorney out of your own pocket. For a business, the stakes are even higher.

A 2023 report from Insureon noted that 78% of U.S. small businesses correctly listed their legal business entity as the named insured. That's a critical step. Why? Because the named insured gets the broadest protection, including defense costs that averaged $30,000 per claim back in 2022. According to their analysis, getting this detail right helped prevent coverage gaps in 85% of the litigated cases they reviewed. You can dig into the specifics in this breakdown of named insured responsibilities.

Protecting Your Contracts and Your Assets

For any business, listing the wrong named insured can bring things to a grinding halt. Many client contracts require you to add them as an "additional insured" on your policy. But if your own business isn't listed correctly as the primary named insured, that certificate of insurance you hand over could be completely worthless.

This kind of oversight can quickly snowball into bigger problems:

- Breach of Contract: If you can't provide valid proof of insurance, you could be in default of your client agreements, leading to lost work and potential legal action.

- Uncovered Operations: Do you run multiple LLCs or subsidiaries? If you only list the parent company, your other entities might have zero coverage.

- Denied Claims: An insurer has every right to deny a claim if the loss involves a business or property that isn't officially listed on the policy.

An accurately structured policy is your first and most effective line of defense. Ensuring the right people and legal entities are listed as named insureds closes dangerous loopholes and secures your financial foundation against unexpected disasters.

The same logic applies to your personal assets. If you co-own a property—maybe a vacation home with your sibling or a house with your partner—but only one of you is on the policy, you're taking a massive risk. Both owners need to be listed as named insureds to have equal rights and protection. Otherwise, one person is left completely powerless if something goes wrong.

Getting Your Named Insured Details Right

Your insurance policy isn't a static document you file away and forget. Think of it as a living agreement that must evolve with your life. Keeping your named insured designations current is crucial for making sure you don't have dangerous coverage gaps when you need protection the most.

Failing to update your policy is a bit like not updating the deed to your house after a marriage or divorce—it can create huge ownership and legal headaches later on. An outdated policy can easily lead to a denied claim at the worst possible time.

How to Check Who Is Currently a Named Insured

First things first, you need to know exactly who is listed on your policy right now. Thankfully, this is straightforward.

Pull out your policy documents and find the declarations page. It’s almost always the very first page, and it acts as the summary of your entire policy. The named insured will be listed clearly right there. This is your single source of truth; if a person or business name isn't on that page, they don't have the rights of a named insured.

Can't find your paperwork? No problem. A quick call to your insurance agent or a few clicks in your online portal will give you the same information. Making this simple check a part of your annual financial review is a great habit to build.

Key Takeaway: An incorrect named insured is one of the most common—and completely avoidable—reasons for a claim to be denied. A quick check of your declarations page ensures your policy matches your reality.

Adding or Removing a Named Insured

Life changes are what usually trigger the need to update your policy. Getting married, going through a divorce, merging your business, or forming a new LLC are all moments when you must contact your insurer. The policy won't update itself.

The official process involves submitting a formal change request, which your insurer will use to issue a policy endorsement. This endorsement is a legally binding amendment to your insurance contract that officially adds or removes a named insured.

To get the ball rolling, you'll generally need to provide:

- The full legal name of the person or business being added or removed.

- Their relationship to the primary insured (spouse, business partner, etc.).

- Supporting documents, like a marriage certificate, divorce decree, or articles of incorporation.

Handling these updates is a key part of good insurance policy management systems, but your agent is there to walk you through it. They’ll help you submit the right information and ensure the endorsement is issued correctly, keeping your coverage accurate and reliable.

Common Mistakes to Avoid With Named Insureds

It’s the small details that often cause the biggest headaches in insurance. A simple oversight in how you list a named insured can create massive coverage gaps, and you usually don't discover them until a claim gets denied—the worst possible time.

Knowing what not to do is the first step toward making sure your policy actually protects you when you need it.

One of the most common blunders we see with business owners is listing a trade name or "Doing Business As" (DBA) instead of the proper legal entity name. An insurance policy covers the legal entity, not the brand name on your sign. If your policy lists "Sunny Day Cafe" but the legal business is "SDC Ventures, LLC," a claim filed under the LLC could easily be rejected.

Forgetting Life and Business Changes

It's also a mistake to assume your insurance just automatically keeps up with your life. A lot of people think that once they get married, their new spouse is instantly covered on their home or auto policy. That's rarely the case. You have to be proactive and call your agent to officially add them as a named insured.

Businesses are even more dynamic. Things change, and your policy has to change right along with them. Here are a few triggers that demand an immediate call to your insurance professional:

- A business merger or acquisition that creates new legal entities.

- Restructuring your company, like moving from a sole proprietorship to an LLC.

- Adding a new partner who has a real ownership stake in the business.

If you don't update your policy after these big moves, you could leave entire parts of your new operation completely uninsured. These kinds of mistakes are some of the most common reasons for an insurance claim denial, and they are almost always avoidable.

A policy is a legal contract with a specific person or entity. If the named insured on that policy no longer exists or has the correct legal status, the contract can become void, leaving you without any protection.

Another devastating, and surprisingly common, misstep is failing to notify the insurance company after a named insured passes away. A policy that gets renewed in the name of a deceased person is likely invalid. This can leave their estate and family members facing huge losses with no coverage to fall back on.

Every one of these mistakes is preventable. It all comes down to proactive communication and regular policy reviews.

Your Top Questions About Named Insureds, Answered

Insurance jargon can feel like a different language, but you don't need a translator to understand your policy. Let's clear up some of the most common questions we hear about the named insured role.

Can My Policy Have More Than One Named Insured?

Absolutely. It's actually quite common. Think of spouses listed on a homeowner's policy or business partners on a commercial liability plan.

When you have multiple names on the policy, it's crucial to know who is the "first named insured." This person is the main point of contact and has the authority to handle administrative tasks, like making changes or receiving cancellation notices.

Does Adding Another Named Insured Make My Insurance More Expensive?

It often does, yes. When you add a named insured, you're asking the insurance company to cover another person or entity's risk, and that added exposure usually comes with a higher premium.

A classic example is adding a teenage driver to your auto policy—your rates will almost certainly go up. For a business, bringing a new partner or an entire subsidiary under your policy can also affect the final price. It's always best to have a conversation with your agent about the cost before making the change.

Key Insight: A named insured isn't just a label; it's a person or business whose risk profile is woven into the fabric of your policy's cost. The more people on that list, the more potential there is for a claim.

What’s the Difference Between a Named Insured and a Loss Payee?

This one trips people up all the time, but the distinction is pretty simple. A named insured is the policy owner who gets the full suite of protections, including liability coverage. A loss payee, on the other hand, is just a third party with a financial interest in your property, like the bank that holds your car loan.

If your car is totaled, the insurance check is usually made out to both you and the bank. This ensures the lender gets their money back. But that's where their rights end—a loss payee has no say in managing the policy.

What Happens if the Named Insured on a Policy Dies?

When a named insured passes away, the policy doesn't just disappear. Coverage typically extends to their legal representative or the person managing their estate, but only for the property already covered.

It is absolutely critical that the representative contacts the insurance company right away. This allows the policy to be updated correctly and prevents any gaps in coverage. If you don't, you could run into major legal trouble—renewing a policy in the name of someone who has passed away could make it completely void.

Getting the named insured details right is fundamental to your financial security. At Wexford Insurance Solutions, our team is ready to comb through your policies and make sure they’re perfectly aligned with your life and business. Contact us today for a complimentary policy review.

A Shipper's Guide to Marine Cargo InsuranceA Smart Traveler's Guide to Insurance When Renting a Car

A Shipper's Guide to Marine Cargo InsuranceA Smart Traveler's Guide to Insurance When Renting a Car