Let's get right to it: your auto insurance deductible is the amount you agree to pay out-of-pocket for repairs before your insurance company steps in to cover the rest. Think of it as your share of the cost when you file a claim for damage to your own car.

How Your Auto Insurance Deductible Works

Imagine you and your insurance carrier are partners in a financial safety net for your vehicle. The deductible is your contribution to that partnership when something goes wrong. It’s a core concept that directly shapes both your premium costs and what you’ll pay after an accident.

It's a lot like the co-pay you have for a doctor's visit. You pay a small, set amount first, and your health insurance takes care of the much larger bill that follows. Your auto deductible operates on the same principle for your car. By taking on a small, predictable piece of the financial risk yourself, you help insurance companies manage their overall costs, which helps keep premiums more affordable for everyone.

To see how this fits into the bigger picture, check out our guide on what is a deductible in insurance.

Where You'll See a Deductible on Your Policy

A common misconception is that a deductible applies to every part of your auto policy. That's not the case. You’ll typically only deal with a deductible for coverages that repair or replace your own vehicle.

- Collision Coverage: This pays to fix your car after you hit another vehicle or an object (like a light pole or a fence).

- Comprehensive Coverage: This handles just about everything else—think theft, vandalism, fire, hail, or hitting a deer.

Deductibles are a key feature of both Collision and comprehensive car insurance coverage, but they don't apply to your Liability coverage, which pays for damages you cause to other people or their property.

Key Takeaway: Your deductible is a cost-sharing tool that only applies to claims for your own vehicle, specifically under Collision and Comprehensive coverages.

A Practical Example of a Deductible in Action

Let's put this into a real-world context. Say you accidentally back into a post in a parking lot, causing $3,500 in damage to your bumper and trunk. Your auto policy has a $500 deductible for Collision coverage.

After you file the claim, the process is simple. You take your car to the repair shop. When the work is done, you pay your $500 deductible directly to the shop. Your insurance company then cuts a check to the shop for the remaining $3,000.

It's a straightforward system. Instead of being on the hook for the full $3,500, your out-of-pocket cost is capped at a manageable $500. That’s your policy doing exactly what it was designed to do: protect you from big, unexpected financial hits.

The Link Between Your Deductible and Insurance Premium

One of the most powerful levers you can pull to manage your auto insurance costs is the deductible. Think of your deductible and your monthly premium as two ends of a seesaw. When you raise your deductible, your premium almost always goes down. Lower your deductible, and you can expect your premium to creep up.

Why does this happen? By choosing a higher deductible, you’re essentially telling the insurance company you're willing to handle a larger piece of the financial pie for smaller claims. This agreement lowers the insurer's potential payout, which in turn reduces their risk. They reward you for taking on that extra responsibility with a lower premium.

This dynamic is more than just a numbers game; it's a strategic choice. It's about balancing what you pay every month against what you could comfortably pay out-of-pocket if you get into an accident.

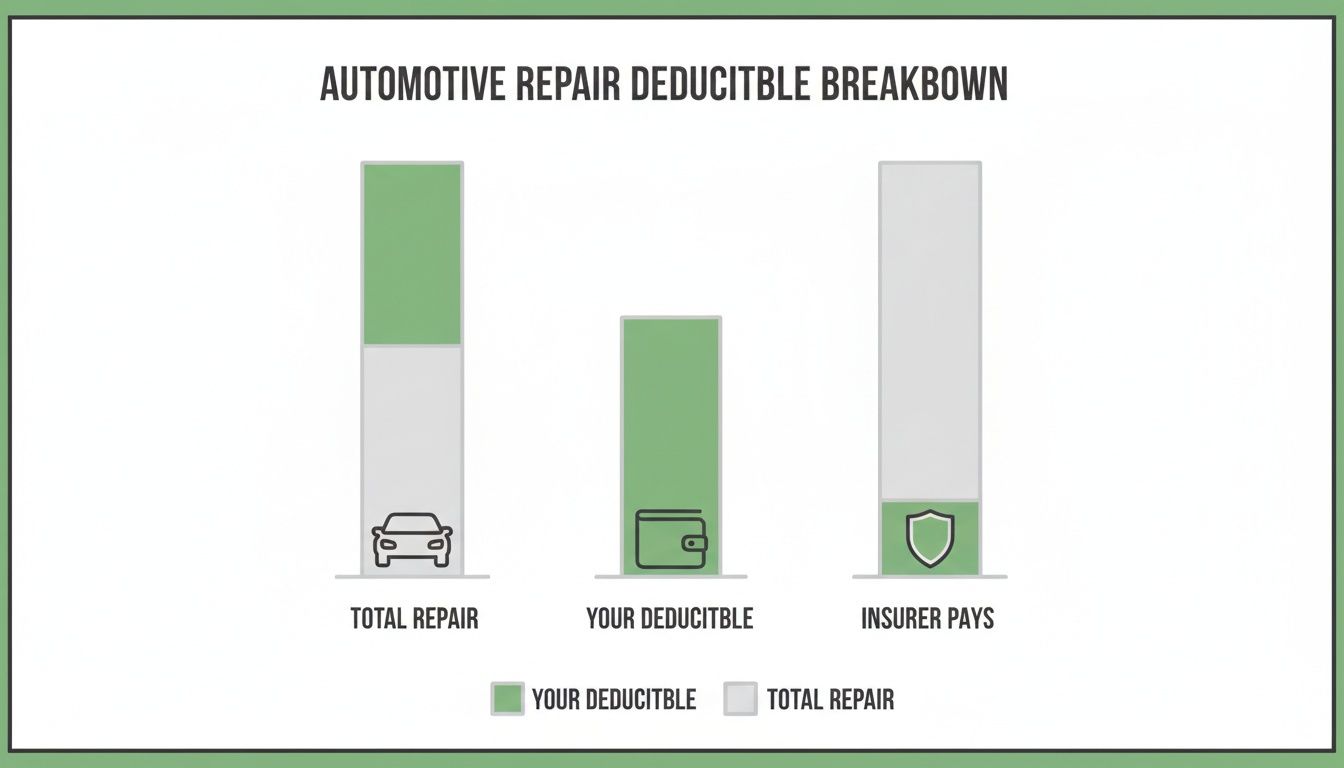

Visualizing the Payout Structure

It’s crucial to understand exactly how the costs break down when you file a claim. After a covered incident, the total repair bill gets split between you and your insurer. You pay your deductible first, and they cover the rest.

The chart below gives you a clear picture of this split, showing your fixed portion versus the insurer's share.

As you can see, your deductible is a predictable, one-time cost for a given claim. Your insurance carrier is there to handle the bigger, often unpredictable portion of the bill, which is exactly why you have coverage in the first place.

Quantifying the Premium Savings

The savings you can unlock by tweaking your deductible are often substantial. While every policy is unique, bumping your deductible from a common $500 to $1,000 or more can make a real dent in your monthly payments.

This strategy has become incredibly relevant lately. With motor vehicle insurance costs jumping 20.6% year-over-year by early 2024, drivers are actively looking for ways to keep their premiums in check. Opting for a higher deductible is one of the most effective ways to do it. As a general rule, each step up—from $500 to $1,000, for example—can trim 10–20% or more from the collision and comprehensive portions of your premium.

From an insurer's perspective, policyholders with higher deductibles are seen as better risks. Why? Because they're less likely to file small, frequent claims for minor dings and scratches. This helps keep the carrier’s costs down, a concept you can explore further by understanding what a loss ratio in insurance is.

To make this more concrete, here’s a breakdown of how different deductible levels can influence your premium savings.

Estimated Premium Savings with Higher Deductibles

The following table shows the potential savings you could see on your collision and comprehensive coverage by choosing a higher deductible. It’s a great way to weigh the immediate monthly savings against your potential out-of-pocket costs after an accident.

| Deductible Amount | Estimated Premium Reduction (Collision/Comprehensive) |

|---|---|

| $500 | Baseline (A common starting point for many policies) |

| $1,000 | 15% to 30% Savings (A popular choice for balancing savings and risk) |

| $1,500 | 25% to 40% Savings (Ideal for those with a healthy emergency fund) |

| $2,500 | Up to 40%+ Savings (Often used by high-net-worth clients or for older cars) |

As the table illustrates, the incentive for taking on a higher deductible is significant. The trick is to land on an amount you know you can pay without causing financial stress.

Of course, your deductible is just one piece of the puzzle. Other factors play a big role in your overall premium, too. For instance, things like the impact of anti-theft devices on insurance premiums can offer another path to lowering your costs. By combining a smart deductible strategy with other discounts, you can build a policy that gives you solid protection at a price that fits your budget.

How to Choose the Right Deductible for Your Needs

Picking the right auto insurance deductible isn't about finding a single magic number. It’s a personal financial decision, plain and simple. What works for a family with a daily driver is going to be completely different from the right strategy for a business managing a whole fleet of vehicles. It all comes down to your unique situation, your comfort with risk, and your cash flow.

The goal is to strike a balance. A lower monthly premium always sounds great, but it’s worthless if an accident puts you in a financial bind because you can't cover the deductible. You need a number that lets you sleep at night, offering both affordable payments and real peace of mind. Let’s break down how to find that sweet spot for different types of drivers. For a more detailed look at the mechanics, check out our complete guide on how a car insurance deductible is explained.

Guidance for the Everyday Driver

For most of us, choosing a deductible comes down to the “sleep-at-night” test. It’s a straightforward but revealing question: Could you write a check for the deductible amount tomorrow without it causing a major financial headache?

If the answer is no, your deductible is too high. A $1,000 or $1,500 deductible might look tempting on paper because of the premium savings, but that advantage disappears fast if you have to drain your savings or max out a credit card to pay it after a claim.

Here’s a practical way to think through it:

- Check Your Emergency Fund: Take a hard look at your savings. Your deductible should be an amount you can pull from your emergency fund without derailing your financial stability.

- Consider Your Car's Value: If you’re driving an older, paid-off car that’s only worth a few thousand dollars, a high deductible like $1,500 probably doesn't make sense. You could easily end up paying a huge chunk of the car's value just to fix it.

- Gauge Your Risk: Are you a cautious driver with a squeaky-clean record? Or do you battle heavy traffic on a long commute every day? How likely you think you are to file a claim should influence how much you’re willing to pay out-of-pocket.

For most drivers, a $500 or $1,000 deductible is a smart, common choice. It hits that sweet spot between premium savings and a manageable out-of-pocket cost if something happens.

A Strategy for High-Net-Worth Individuals

For high-net-worth clients, especially those with luxury or collector cars, the deductible isn't just an expense—it's a strategic financial tool. The mindset shifts from simply insuring against damage to actively managing risk and cost.

By choosing a much higher deductible—think $2,500, $5,000, or even more—you can unlock some serious premium reductions. The logic is simple: you agree to self-insure for the smaller stuff, like minor fender-benders or cosmetic dings. This reserves your insurance policy for what it's truly meant for: major, high-cost events like a total loss or a catastrophic collision.

This approach treats insurance as true protection against catastrophic loss rather than a maintenance plan for small repairs. By handling minor issues out-of-pocket, you maintain a claims-free record and benefit from the lowest possible premiums.

Over a few years, the savings on your premium can easily add up to more than the deductible itself, resulting in a net financial win. It's a calculated decision, of course, built on the confidence that you can comfortably absorb a five-figure repair bill without blinking an eye.

Deductible Planning for Business Fleets

When you're managing a fleet of commercial vehicles, deductibles become a key part of your company's overall risk management program. The focus isn't just on lowering the insurance premium; it's about reducing the total cost of risk. This often means taking on even higher deductibles, sometimes $5,000, $10,000, or more per vehicle.

This is a sophisticated financial play. By retaining more of the risk through a high deductible, a business can achieve massive premium savings across its entire fleet. Those savings can then be put back into the business, funding loss-control programs like driver safety training or telematics systems designed to prevent accidents in the first place.

For commercial fleets, this layered approach is essential. Risk advisors often pair high deductibles with strong fleet management technology and safety protocols to keep total costs down. This allows the business to absorb the routine, predictable losses while transferring only the large, potentially crippling events to the insurance company. It's a strategy that aligns with what we're seeing globally in commercial insurance. You can discover more insights on global insurance trends from the OECD.

At the end of the day, whether you’re a daily commuter, a luxury car owner, or a fleet manager, the right auto insurance deductible is the one that fits your financial reality and your philosophy on managing risk.

Deciding When to File a Claim or Pay Out of Pocket

After a fender bender, your first instinct might be to call your insurance company. But in the heat of the moment, that's not always the smartest financial move. The real question you need to ask is whether the damage is actually worth a potential spike in your future premiums.

This is where a quick cost-benefit analysis saves the day. You have to weigh the immediate cash you'd get from the insurance company against the long-term costs that could follow. Filing a claim—especially a small one—goes on your permanent record and can haunt your rates for years.

Finding Your Breakeven Point

The whole decision boils down to one simple calculation: how much will your insurer actually pay you after you’ve covered your auto insurance deductible? If that number is surprisingly small, you’re often better off handling the repair yourself.

Let's walk through an example. Say you have a $1,000 collision deductible, and the body shop quotes you $1,300 for the repair. If you file a claim, your insurance company will cut you a check for just $300. Now, ask yourself: is that $300 payout worth the risk of your premium jumping at your next renewal?

In most cases, the answer is a hard no. A potential rate hike over the next few years could easily cost you more than that $300 you got from the claim, making it a net financial loss in the long run.

The Hidden Costs of Small Claims

Filing a claim for minor damage can set off a chain reaction of hidden costs that you won't see right away. These financial consequences can stick around long after your car is back on the road.

- Premium Surcharges: An at-fault accident is one of the fastest ways to watch your insurance rates climb. A single claim can add a hefty surcharge to your policy that lasts for three to five years.

- Loss of Discounts: Many insurers reward safe drivers with a valuable "claims-free" or "good driver" discount. Filing one small claim can instantly make you ineligible, causing your premium to jump even higher.

- Impact on Future Insurability: A history of frequent claims can paint you as a high-risk driver. In some scenarios, it could even lead to your policy being non-renewed, forcing you to shop for more expensive coverage elsewhere.

Expert Insight: Think of your insurance policy as a safety net for major, wallet-crushing events, not a maintenance plan for dings and scratches. Using it for small stuff is like calling the fire department because you burnt a piece of toast—it's an overreaction that comes with unintended consequences.

It also helps to know what you're getting into. You can get a clearer sense of the timeline by reading up on how long the insurance claim process can take, which gives you another factor to weigh against the financial payout.

A Checklist for Making a Smart Decision

Before you dial your agent, take a deep breath and run through these questions. Answering them honestly helps you make a logical choice based on numbers, not post-accident stress.

- Is the repair cost significantly higher than my deductible? If the total repair bill isn't at least double your deductible, paying out of pocket is usually the smarter play.

- Am I clearly at fault? If the answer is yes, a claim is far more likely to trigger that dreaded rate increase.

- Can I afford to pay for the damage myself? If the repair cost would cause you genuine financial hardship, then using your insurance is exactly what it’s there for.

- How much is my claims-free discount worth? Check your policy. Is losing a 15-25% discount really worth a small claims check? Probably not.

- Was anyone injured? If there are any injuries, even minor ones, you should report the incident to your insurer immediately. This is non-negotiable—your liability coverage is there to protect you.

Thinking through these points puts you in control. It helps you use your insurance strategically, saving it for the big stuff when you truly need it most.

Putting Your Deductible to Work: The Claims Process

Knowing what a deductible is feels very different from knowing how it works after the stress of an accident. The theory is simple, but the real-world process can feel overwhelming. Let's break down exactly what to expect when you file a claim, because it all hinges on one key question: who was at fault?

An accident is chaotic enough. You shouldn't have to worry about how the payments will be handled. Your deductible is the first step in the financial recovery, and understanding its role will give you confidence from start to finish.

When You’re At Fault

If the accident is determined to be your fault, the process is pretty straightforward. You’ll file a claim under your own collision coverage, get an approved estimate, and head to the repair shop.

Once the work is done, you pay your deductible directly to the shop. For instance, if the total repair bill is $4,000 and you have a $1,000 deductible, you’ll pay the shop $1,000. Your insurance company then covers the remaining $3,000. It's a clean handoff—you cover your share, and your policy covers the rest.

When Another Driver Is At Fault

Things get a bit more interesting when the other driver is clearly at fault. Their liability insurance is ultimately responsible for your vehicle's damages, but dealing with another insurance company can be a slow, frustrating process. You could be waiting weeks for them to accept liability, all while you're stuck without a car.

This is where your own policy can save the day. You can choose to file the claim under your own collision coverage to get your car fixed immediately. You'll pay your deductible to the shop upfront, but here’s the important part: your insurer will then go after the at-fault driver's insurance company to recover the entire cost of the claim, including your deductible. This is a process called subrogation.

What is Subrogation? Think of it as your insurance company going to bat for you. They cover your claim first to make you whole, then they fight to get reimbursed by the party who was actually responsible. When they win, you get your deductible paid back.

An independent agent acts as your advocate here, making sure the subrogation process moves along correctly so you get that money back in your pocket. Knowing how to negotiate an insurance settlement is a skill, and having an expert on your side makes a huge difference.

Special Deductible Programs

It's also worth noting that some carriers offer creative ways to manage your deductible. One of the most common is a disappearing deductible (sometimes called a diminishing deductible). It’s designed to reward safe drivers.

The way it works is simple: for every year you go without a claim, the carrier reduces your deductible. A $500 deductible might shrink by $100 for each accident-free year, eventually hitting $0 after five years. It’s a fantastic perk that can eliminate your out-of-pocket cost entirely if you ever do need to file a claim down the road. An independent agent can point you toward carriers with these programs and help build a policy that truly rewards you for your driving habits.

Building a Smarter Insurance Strategy with an Advisor

Choosing the right auto insurance deductible isn't just about picking a number from a dropdown menu. It's a core part of your personal financial strategy, a decision that directly affects both your monthly budget and how much risk you carry. Think of it as the centerpiece of a plan built to protect what you own.

This is a classic balancing act: lower premiums today versus potentially higher out-of-pocket costs tomorrow. An everyday commuter, a high-net-worth individual with a car collection, and a commercial fleet manager all look at this equation differently because their risks and financial goals are worlds apart. A one-size-fits-all policy just won't cut it.

Why Expert Guidance Matters

Trying to figure all this out on your own can feel like guesswork. That’s where working with a dedicated, independent advisor really pays off. Instead of just hoping you've picked the right number, you're partnering with a professional who can analyze your specific situation and build a policy that actually works for you.

An advisor helps you look past the obvious and craft a truly strategic plan. They do this by:

- Analyzing Your Financial Picture: They'll take a look at your savings, cash flow, and overall comfort with risk to recommend a deductible you can genuinely afford if something happens.

- Aligning Coverage with Your Assets: Whether it's a family minivan, a prized classic car, or a fleet of work trucks, they ensure your policy matches the real value and use of your vehicles.

- Uncovering Hidden Savings: An expert knows where to find discounts and policy structures you might easily miss when going it alone.

Partnering with an expert turns your insurance policy from a simple monthly bill into a strategic asset. It becomes a tool that actively protects your financial health without forcing you to overpay for coverage you don't need.

In the end, a smart insurance strategy means you never have to second-guess your coverage after an accident. With an advisor's help, you can be confident that your policy is built for your life, ready to do its job when you need it most.

Common Questions About Auto Insurance Deductibles

Even when you’ve got a good handle on what an auto insurance deductible is, real-life situations can throw you a curveball. Think of this section as your quick-reference guide for those tricky scenarios. We'll cut through the confusion and give you straight answers to the questions we hear most often.

Getting these details right helps you make the most of your insurance, so you feel ready for whatever the road throws your way.

Do I Have to Pay a Deductible If an Accident Is Not My Fault?

This is easily the most common question we get, and the answer can be a bit surprising. Initially, yes, you'll probably have to pay your collision deductible to get your car fixed right away. You don't want to wait weeks for the other driver's insurance to admit fault, and this gets you back on the road.

But here's the good part. Once the other driver is officially found to be at fault, your insurance company goes after theirs to get reimbursed. This process is called subrogation. When they succeed, you get your deductible paid back to you in full. A great agent will stay on top of this for you to make sure that check comes back.

Can I Change My Deductible at Any Time?

Absolutely. You don’t have to wait for your renewal to adjust your deductible. You can make a change anytime during your policy term, and the new rate will kick in right away. If you raise your deductible, for example, your remaining premium payments for the term will be lower.

That said, it’s always smart to have a quick chat with your agent first. They can walk you through how the change affects your budget both now and in the long run, making sure it’s a sound financial decision and not just a quick fix.

Key Insight: Think of your deductible as a flexible tool for managing your budget. Just make sure the new amount passes the "sleep-at-night" test—meaning you could write a check for it tomorrow without breaking a sweat.

Is a Lower Deductible Always the Better Option?

Not always. It’s a classic trade-off. A low deductible feels safe because your out-of-pocket cost is small, but it comes at the price of a higher premium. More importantly, it might tempt you into filing small claims for every little ding and scratch.

A history of frequent claims, even minor ones, can make your rates shoot up or even lead to your insurer deciding not to renew your policy. Often, choosing a higher deductible saves you more money over time through lower premiums and encourages you to save your claims for the big stuff.

Does My Liability Coverage Have a Deductible?

Nope. Standard auto policies don't have a deductible for liability coverage. Liability is there to pay for injuries and property damage you cause to other people. Your insurance company covers those costs from the very first dollar, right up to your policy limit.

Deductibles only apply to the coverages that protect your property, like Collision and Comprehensive.

At Wexford Insurance Solutions, our advisors are here to help you find that perfect balance. We'll work with you to choose a deductible that fits your financial comfort zone. Start a conversation with our team today to get your coverage dialed in just right.

Cyber Insurance Coverage Checklist: Protect Your Business in 2026Homeowners Insurance Coverages Explained: A Complete Guide

Cyber Insurance Coverage Checklist: Protect Your Business in 2026Homeowners Insurance Coverages Explained: A Complete Guide