Let's say you've landed a huge account and extend them credit, feeling secure in their history and your relationship. But then, out of nowhere, an unexpected market downturn hits them hard, and they can't pay. What happens to your bottom line? This exact scenario is why trade credit insurance exists—it's your financial safety net. It’s a smart way to protect your accounts receivable from the risk of a customer defaulting.

Your Financial Shield, Explained

At its heart, trade credit insurance is all about protecting your business when customers fail to pay what they owe. Think of it as a protective layer guarding your company’s cash flow. Every time you sell goods or services on credit, you’re essentially creating an IOU that sits on your balance sheet as an asset. But until that cash is actually in the bank, it's a risky asset.

This insurance takes that unpredictable credit risk and transforms it into a manageable, fixed business expense. Instead of gambling on whether a major customer will pay, you pay a predictable premium. This lets you operate with much more confidence, knowing a vital part of your business is secure.

How the Coverage Actually Works

The main job of a trade credit insurance policy is simple but incredibly powerful. It's built to shield your company from two key commercial risks:

- Insolvency: This covers you if a customer goes bankrupt or enters a similar legal status and simply cannot pay their debts.

- Protracted Default: This kicks in when a customer is late on their payment for an undisputed invoice—well past the agreed-upon date—even if they haven't officially declared insolvency.

By covering these situations, the policy makes sure you get reimbursed for a large portion of your unpaid invoices. That kind of stability is a game-changer for any company, but it's especially critical for small and mid-sized businesses where one bad debt could be catastrophic. For a deeper dive into other essential protections, our guide on insurance for small business owners is a great resource.

Trade credit insurance isn't just about getting paid back for losses; it's about enabling smarter business decisions. When the fear of non-payment is off the table, you can offer more competitive credit terms, go after bigger clients, and explore new markets with way less financial stress.

A Tool for Growth, Not Just Defense

It's a common mistake to see this coverage as purely defensive. It’s actually a proactive tool for driving sustainable growth. Once your receivables are insured, you can make bolder, more strategic choices about who you extend credit to and how much.

Your insurer's credit analysis of your customers also gives you a powerful dose of market intelligence. It helps you steer clear of risky accounts while confidently identifying stable partners for growth. To really get the full picture, it helps to see trade credit insurance as one of several modern credit risk management tools available. It works hand-in-hand with your other financial strategies to strengthen your business, turning what could be a huge liability into a real opportunity.

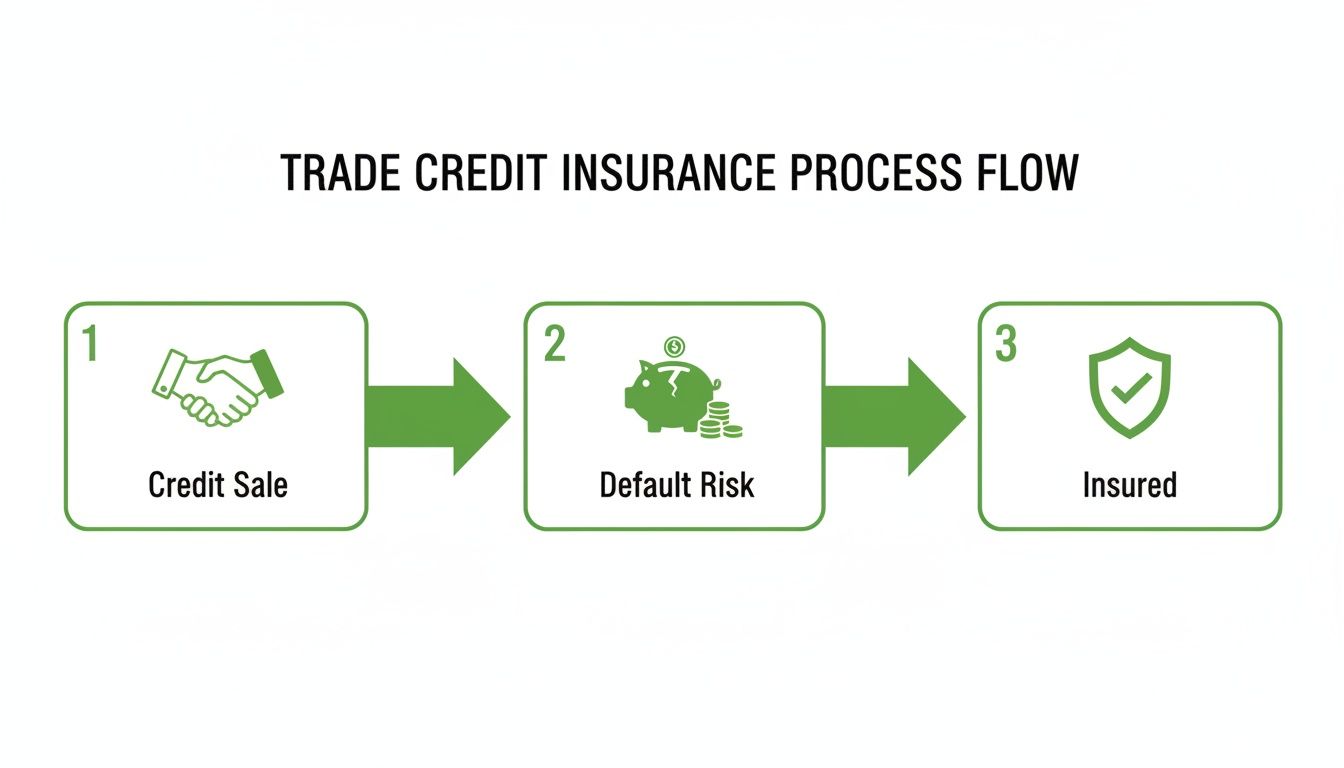

How the Process Works From Policy to Payout

Let's break down how trade credit insurance works in the real world. Thinking about it in terms of its lifecycle—from setting up the policy to what happens when you actually need it—makes the whole concept much clearer. It’s not just an abstract financial product; it’s a practical tool that protects your cash flow.

The journey follows a logical path: assessing risk, setting coverage limits, keeping an eye on your customers, and, if the worst happens, filing a claim.

This visual shows that simple, everyday process of selling on credit and how insurance steps in to shield you from the risk of non-payment.

As you can see, every time you extend credit, you're taking on a risk. The right policy turns that uncertainty into a manageable part of doing business.

The Underwriting and Credit Limit Stage

Everything starts with underwriting. This is where the insurance company essentially becomes an extension of your credit department. They dig deep into the financial health of your customers—the whole portfolio or just specific ones you want to insure. They'll look at everything from payment histories and industry trends to political and economic stability in your customers' home countries.

Based on this analysis, the insurer assigns a credit limit for each buyer. This isn't just an arbitrary number; it's the maximum invoice amount they will cover for that specific customer. Think of it as a safety net for your accounts receivable. It gives your sales team a clear, pre-approved boundary to work within, so they can confidently close deals without second-guessing the risk.

Ongoing Risk Monitoring

Here's where a good trade credit policy really shines. The insurer’s job isn't done once the limits are set. They provide continuous risk monitoring on all your covered buyers. With their global reach and access to massive amounts of payment data, they can often spot trouble brewing long before you can.

It’s like having an early-warning system for your receivables. If a major customer starts paying other vendors late, the insurer might see that pattern and proactively lower their credit limit, giving you a heads-up. This kind of intelligence lets you take action—maybe by tightening payment terms or reducing your exposure—before a problem becomes a crisis.

This ongoing partnership is one of the most valuable parts of a policy. You're getting access to a level of credit intelligence that would be incredibly expensive and time-consuming to build in-house.

The Claims Process When a Customer Defaults

So, what happens when a customer simply can't or won't pay? This is the moment the insurance proves its worth. The claims process is designed to be a clear, supportive path to getting your money back and keeping your business on track.

It generally follows these steps:

- Notification: The moment an invoice becomes overdue past a certain point (as defined in your policy), you let your insurer know.

- Waiting Period: There's typically a waiting period where you and the insurer might continue collection efforts.

- Claim Filing: If the bill is still unpaid after that period, you officially file a claim, providing documentation like the original invoices and proof of delivery.

- Payout: Once your claim is approved, the insurer pays you the covered portion of the bad debt—usually up to 90% of the invoice value.

This kind of protection is becoming more critical than ever. The global trade credit insurance market was valued at up to $13.29 billion in 2025 and is expected to keep growing. That number tells a story: businesses everywhere are realizing they need to secure their sales, both at home and abroad.

Knowing how to file a claim properly is key to a fast and successful outcome. For a step-by-step guide, check out our article on how to file an insurance claim. A well-managed policy transforms a potentially catastrophic bad debt into a predictable, manageable event, protecting your business from a serious financial hit.

Strategic Benefits Beyond Just Getting Paid

Sure, the most obvious reason to get trade credit insurance is to make sure you get paid if a customer doesn't come through. But thinking of it only as a defensive play is like using a smartphone just to make calls—you're missing out on its real power.

When you look closer, a well-structured policy is actually a proactive engine for growth. It can completely reshape how you approach business, turning uncertainty into a serious competitive advantage. Instead of hesitating on bigger orders or backing away from new markets, you can chase them confidently. This one shift can move your business from a cautious, risk-averse mindset to one of calculated, ambitious growth.

Drive Safer and More Ambitious Sales

Picture this: your sales team is on the verge of landing a massive new client. The catch? They want generous credit terms, but your internal policy is buttoned-up and cautious. Without insurance, you're stuck. You could offer restrictive terms and probably lose the deal, or you could take a huge risk and just cross your fingers.

Trade credit insurance completely changes that scenario. With a policy backing you up, you can offer those competitive terms without breaking a sweat, knowing your receivables are protected. This gives your sales team the power to:

- Attract Larger Customers: Go after those enterprise-level clients who demand extended payment terms, without shouldering all the risk yourself.

- Increase Sales to Existing Clients: Feel comfortable raising the credit limits for your best customers, letting them place larger, more frequent orders.

- Shorten Sales Cycles: Close deals faster. With pre-approved credit limits on potential buyers, there's no more waiting around for lengthy internal credit reviews.

Ultimately, it gives you the confidence to say "yes" to game-changing opportunities you might have been forced to turn down before.

Unlock Better Financing and Improve Cash Flow

Your accounts receivable are one of your biggest assets, but banks often get nervous about them. An unpaid invoice is just a promise, not cash in the bank. But when those same receivables are insured, they suddenly look a lot more reliable to lenders.

Lenders often allow companies with trade credit insurance to borrow against a higher percentage of their accounts receivable. Insured receivables are seen as high-quality collateral, directly improving your borrowing capacity.

This stronger borrowing base has an immediate impact. It can lead to better loan terms, lower interest rates, and much-needed access to working capital. It's not just about getting paid; a policy helps you improve working capital by protecting your balance sheet from the shock of a bad debt.

Sharpen Your Internal Credit Management

Think of your insurer as a powerful extension of your own credit department. They have access to incredible amounts of data and market intelligence on millions of companies around the world—far more than any one business could ever hope to gather.

This partnership gives you critical insights that make your own risk assessment process sharper. Your insurer constantly monitors the financial health of your customers, often flagging potential red flags long before they turn into real problems. This kind of expert oversight is a cornerstone of any solid approach to what is risk management in business. This lets you make smarter credit decisions, sidestep high-risk buyers, and point your sales team toward stable, creditworthy partners.

Expand into New Markets Confidently

Thinking about exporting? Taking your business global comes with a whole new set of risks. You're dealing with unfamiliar legal systems, currency swings, and political instability, all of which crank up the risk of non-payment. This is where trade credit insurance becomes absolutely essential.

It gives you the security blanket you need to offer credit terms to international buyers, which puts you on equal footing with their local competitors. Even with these benefits, it's surprising how few businesses take advantage of it. Right now, only about 15% of global trade is covered by these policies, which means there's a huge opportunity for savvy companies to get ahead.

With your foreign receivables secured, you can explore new territories and build a global customer base without constantly looking over your shoulder. You can grow with confidence, knowing your revenue is protected no matter where in the world you do business.

Is Trade Credit Insurance Right for Your Business?

While the strategic benefits are clear, trade credit insurance isn't a one-size-fits-all solution. The real question is whether the protection it offers lines up with the day-to-day reality of your business operations. It’s all about understanding if your company’s risk profile is a good match for what this coverage is built to do.

Deciding if a policy makes sense means taking a hard look at who you sell to, the industry you operate in, and your plans for the future. For some businesses, it's a critical safety net. For others, it’s the fuel needed for aggressive expansion. Let's dig into the types of businesses that typically see the biggest upside.

A Game Changer for SMBs

For any small or medium-sized business (SMB), cash flow is the lifeblood. A single large customer failing to pay isn't just a minor setback; it can create a dangerous ripple effect that threatens your ability to make payroll, pay your own suppliers, and keep the lights on. Unlike massive corporations with deep cash reserves, most SMBs are working with a much thinner financial cushion.

This is where trade credit insurance can be a complete game-changer. It effectively transfers a huge chunk of your credit risk to an insurer, letting you focus on running the business instead of constantly worrying about who might not pay. It turns a potential disaster into a predictable, manageable business expense.

For an SMB, a bad debt isn't just a line item on a spreadsheet—it's a direct threat to survival. Insuring that receivable gives you the confidence to make bold decisions.

Essential Protection for Exporters

When you start selling across borders, your risks don't just add up—they multiply. Exporters have to deal with a whole layer of complexity that domestic-only companies never see.

Think about challenges like:

- Political Risks: Sudden events like civil unrest, war, or a government seizing assets can make it impossible for an overseas buyer to pay you.

- Currency Fluctuations: A sharp, unexpected swing in exchange rates can wipe out your profit or make the invoice unaffordable for your customer.

- International Laws: Trying to collect a debt in a foreign legal system can be a nightmare—it's often slow, expensive, and confusing.

Trade credit insurance is built to handle these international risks. It gives you the security to offer competitive payment terms to buyers in other countries, which is often what it takes to win the deal. It essentially builds a bridge of trust, letting you grow your global footprint without shouldering an impossible amount of risk.

Critical for Wholesalers and Manufacturers

Wholesalers, distributors, and manufacturers often run on tight profit margins and rely on high sales volume to succeed. Their business model means they are constantly extending credit, and that risk is often concentrated in just a handful of major buyers. If one of those key accounts goes under, the financial hit can be massive.

Just imagine these everyday scenarios:

- A wholesaler lands a huge order, sending pallets of goods to a major retail chain on net-60 terms.

- A manufacturer ships a large, custom-built order to their primary distributor, with payment due upon delivery.

In both situations, the seller's money is tied up in accounts receivable. If the buyer files for bankruptcy, that cash is likely gone for good. Trade credit insurance protects that crucial link in the supply chain. It ensures that even if a customer defaults, you get paid, allowing you to maintain operations and keep your own business healthy.

To put it in perspective, let's look at how this applies across different business types.

Trade Credit Insurance Applicability by Business Type

This table breaks down the primary risks different businesses face and shows exactly how trade credit insurance steps in to help.

| Business Type | Primary Credit Risk | How Trade Credit Insurance Helps |

|---|---|---|

| Small & Medium Businesses (SMBs) | A single large customer default could threaten the entire business due to limited cash reserves. | Provides a financial backstop, stabilizing cash flow and enabling confident growth decisions. |

| Exporters | Political instability, currency volatility, and complex foreign legal systems make collecting overseas payments uncertain. | Covers non-payment due to political and commercial risks, making it safer to offer competitive terms and enter new markets. |

| Wholesalers & Distributors | High-volume, low-margin sales model with significant credit exposure concentrated among a few key retailers or buyers. | Protects against the catastrophic impact of a major buyer's insolvency, securing the supply chain. |

| Manufacturers | Large capital outlay for raw materials and production, with payment often delayed until after delivery (e.g., net-90 terms). | Safeguards working capital tied up in receivables, ensuring funds are available for ongoing production and operations. |

As you can see, the core benefit is the same—protecting your cash flow—but the specific problem it solves can look very different depending on how your business operates.

Diving Into the Details: Underwriting and Pricing

To get the most out of a trade credit insurance policy, you have to understand how it’s built from the ground up. Insurers don’t just pull a price out of a hat. Instead, they conduct a detailed analysis of your company's specific risk profile in a process called underwriting. This is what determines your premium, coverage limits, and the overall structure of your policy.

Think of it like getting a business loan. The lender needs to understand the odds of you paying them back. Similarly, an insurer needs to gauge the likelihood of one of your customers failing to pay you. Knowing what they look for puts you in a much stronger negotiating position and helps you land a policy that’s both effective and fairly priced.

Key Factors in the Underwriting Process

Insurers are looking at the whole picture of your credit risk, not just your customers' payment habits. A big part of their assessment comes down to how well you manage that risk internally. Strong, consistent processes can make a world of difference.

Here’s what they’ll zoom in on:

- Your Internal Credit Management: Do you have a clear, documented system for vetting new customers, setting credit limits, and chasing down overdue payments? A well-oiled credit department signals to insurers that you’re a proactive and low-risk partner.

- Historical Bad Debt Experience: Your past is a pretty good predictor of your future. A clean track record with minimal write-offs is powerful proof that your credit controls work.

- Industry and Sector Risk: Let's face it, some industries are just more volatile than others. Underwriters will analyze the overall economic health and typical default rates within your specific business sector.

- Buyer Quality and Concentration: The creditworthiness of your customers is obviously front and center. But they also look closely at risk concentration. If 80% of your revenue is tied up with a single buyer, that’s a much bigger risk than if it’s spread across 50 different customers.

How Pricing and Premiums Are Calculated

After the underwriting deep-dive, the insurer puts a price on the policy. This isn't a standard, off-the-shelf number; it’s a premium calculated specifically for your business based on the risk you present.

Typically, the premium is a small percentage of your total insured sales. For instance, a rate might be set at 0.25% of your projected annual turnover. The factors we just covered will push that rate up or down. A business with rock-solid credit controls and a diverse, high-quality customer base will always get a better rate than one with concentrated risk and a history of bad debt.

The goal of underwriting is to establish a fair price for the risk being transferred. A lower premium reflects the insurer's confidence in your ability to manage credit effectively, complemented by their safety net.

Getting comfortable with these details is a huge advantage. If you want to get even more familiar with the fine print, our guide on how to read an insurance policy is a great place to start. This knowledge empowers you to work with insurers as a truly informed partner.

Partnering with Wexford to Secure Your Business

Let's be honest: navigating the world of trade credit insurance can be a real headache. You're faced with a dozen different insurers, each with its own jargon and pages of fine print. It's easy to get lost in the weeds.

This is exactly where a specialist broker like Wexford Insurance Solutions comes in. Think of us as your guide and advocate, here to cut through the complexity and make the entire process straightforward.

Your Advocate in the Insurance Market

Instead of you spending countless hours chasing down quotes from multiple insurance companies, we bring the market directly to you. We start by getting to know your business inside and out—your sales process, your customer base, and your comfort level with risk.

Armed with that understanding, we tap into our deep relationships with top-rated carriers to find the right coverage. It’s not just about finding a policy; it’s about finding the right policy that fits your company like a glove, offering solid protection without breaking the bank.

Our goal is simple: to lower your total cost of risk. We do this by blending expert, one-on-one advice with smart, tech-driven service that makes managing your policy and handling claims a breeze.

Essentially, we become a part of your team. You get all the benefits of having a risk management expert on staff, focused on protecting your cash flow so you can focus on growing your business.

A Personalized, Hands-On Approach

From the first conversation to ongoing policy reviews and, most importantly, helping you when a claim arises, we handle the heavy lifting. We'll dig into your accounts receivable ledger, spot potential risks you might have missed, and lay out your options in plain English.

Our entire process is built to give you clarity and peace of mind every step of the way.

You’ve got a business to run. Let us worry about the insurance details. Understanding the difference a true partner can make is the first step. To see what that looks like in practice, check out our guide on how to choose an insurance broker. We’d love to show you how the right partnership can transform your trade credit insurance from a necessary expense into a powerful tool for growth.

Answering Your Top Questions About Trade Credit Insurance

As we wrap things up, let's dig into some of the most common questions business owners ask about trade credit insurance. My goal here is to clear up any lingering confusion with straightforward, practical answers so you can feel confident about your next steps.

Think of this as the final piece of the puzzle, giving you the clarity you need to protect your business effectively.

Is Trade Credit Insurance Really Affordable for a Small Business?

This is probably the number one question I hear, and it's rooted in a big misconception. Many smaller businesses assume this type of coverage is out of reach, something only for the big players. The reality is quite different. The premium is typically just a small fraction of your annual sales—often less than half a percent.

Here’s a better way to think about it: What would happen if your single biggest customer went under tomorrow? For most small businesses, the financial hit from just one major bad debt would be far, far greater than the annual cost of a policy. It’s not so much an expense as it is an investment in your company's stability and your own peace of mind.

Single Buyer vs. Whole Turnover: Which Policy is Right for Me?

Figuring out the right type of policy comes down to your specific business and where your risks are concentrated. It’s all about choosing the right tool for the job.

- Single-Buyer Policy: This is like putting a spotlight on one specific customer. It’s the perfect solution when you have a single, massive account that makes up a huge chunk of your revenue. You’re isolating and neutralizing your biggest risk.

- Whole-Turnover Policy: This is more like a floodlight, covering your entire book of business. It gives you broad protection and is generally more cost-effective per customer, making it a smart choice for companies with a wide and varied customer base.

A whole-turnover policy does more than just protect you from a surprise default by a customer you thought was solid. It also taps into the insurer's vast credit intelligence across your entire sales ledger, seriously upgrading your own credit management process.

Does This Insurance Cover Political Risks for Exporters?

Yes, it absolutely does. This is one of the most valuable features for any company doing business across borders. A good trade credit insurance policy can be built to cover you against both commercial (customer default) and political risks.

This means you’re covered even if your foreign customer can't pay for reasons that are completely out of their hands. These political risks can include events like:

- War or major civil unrest in the buyer’s country.

- Sudden government actions, like canceling an import license or imposing a trade embargo.

- Currency conversion issues, where the local government prevents funds from being transferred out of the country.

For any business venturing into new or emerging markets, this coverage transforms unpredictable global chaos into a manageable business risk.

If I Have to File a Claim, How Quickly Will I Get Paid?

The claims process is laid out clearly in your policy documents. It starts after a set waiting period, which usually kicks in right after an invoice becomes past due. The insurer or their partners might even help with collection efforts during this window.

Once that waiting period is over, you’ll file the claim with the necessary paperwork (invoices, proof of delivery, etc.). From there, the insurer gets to work. While every case is a bit different, a clean, well-documented claim is typically paid out within 30 to 60 days. The whole point is to get that cash back into your business quickly, stopping a bad debt from snowballing into a full-blown cash flow crisis.

Ready to turn accounts receivable risk into a strategic advantage? The team at Wexford Insurance Solutions can help you navigate the market and find the perfect trade credit insurance policy for your business. Contact us today to get a personalized consultation.

Business Income Insurance: Protect Your Revenue After a DisasterWhat Is Completed Operations Coverage And Why Your Business Needs It

Business Income Insurance: Protect Your Revenue After a DisasterWhat Is Completed Operations Coverage And Why Your Business Needs It