"So, what's the bottom line?" That's the first question every business owner asks about insurance. While the numbers can swing from $400 a year to well over $7,000, there's no single price tag that fits everyone.

Think of it like buying a vehicle. The heavy-duty truck a landscaping company needs is a totally different investment than the sedan a consultant uses to visit clients. Your business insurance premium works the same way; it’s a unique blend of your specific risks, the coverage you choose, and the nitty-gritty details of how you operate.

Deconstructing Your Business Insurance Cost

To get a real handle on what you'll pay, it helps to stop thinking of insurance as a single product. Instead, see it as a collection of individual shields, each designed to protect you from a different kind of threat.

You wouldn’t use a rain umbrella to block the sun, right? The same logic applies here. You need the right policy for the right risk, and your final cost is simply the sum of all the protections you’ve put in place. This tailored approach ensures you’re not paying for coverage you don’t need or, even worse, leaving your business dangerously exposed.

Average Annual Business Insurance Premiums

Let's look at some real-world numbers. The table below gives you a snapshot of what small businesses typically pay for the most common types of coverage. These figures are a great starting point to set expectations before we dig into the specific factors that will shape your final quote.

Average Annual Business Insurance Premiums

| Insurance Policy Type | Typical Annual Premium Range | Who It Protects |

|---|---|---|

| General Liability Insurance | $400 – $1,200 | Your business from claims of third-party bodily injury or property damage. |

| Business Owner's Policy (BOP) | $500 – $2,500 | Your business by bundling General Liability and Commercial Property insurance. |

| Workers' Compensation | $550 – $2,000 per employee | Your employees from work-related injuries or illnesses, covering medical bills and lost wages. |

| Professional Liability (E&O) | $600 – $1,500 | Your business from claims of negligence, errors, or omissions in professional services. |

It's important to see these numbers as guideposts, not guarantees. They give you a general idea, but your actual premium will be specific to your situation.

Key Takeaway: These figures are ballpark estimates. A high-risk industry like construction will naturally see higher premiums than a low-risk one like freelance writing, even for the same type of policy. Your specific operations are the most significant driver of your final cost.

While this table offers a helpful overview, the only way to get a precise number is to dive into your unique business needs. For those who want a more personalized estimate, you can learn more about how to use our business insurance cost calculator in this detailed guide. In the next sections, we'll break down exactly how insurers arrive at your specific number.

What's Inside Your Business Insurance Policy? A Practical Guide

Think of your business insurance not as a single, monolithic thing, but as a custom-built toolkit. Each policy is a specific tool designed to handle a particular kind of risk. You wouldn't use a wrench to hammer a nail, and you wouldn't rely on a property policy to cover a professional mistake.

To really understand what you're paying for, we need to move past the jargon and look at what these policies actually do in the real world. Let's break down the most common types of coverage and see the kinds of situations they're built to solve.

General Liability Insurance: Your Everyday Shield

This is the bedrock of most business insurance plans. General liability is all about protecting you from claims that your business caused bodily injury or property damage to someone else—think customers, vendors, or just a person passing by. It's your first line of defense for the common, everyday accidents that can happen when you're open for business.

Imagine a customer walks into your shop on a rainy day, slips on a wet floor, and fractures their arm. That's exactly what this policy is for. Without it, you could be on the hook for their medical bills and any legal fees if they decide to sue.

General liability typically covers:

- Bodily injury to a third party: Pays for medical costs if a non-employee gets hurt on your premises.

- Property damage to a third party: Covers repairs if you or an employee accidentally damages someone else's property—like a landscaper breaking a client's window.

- Legal defense: Helps pay for lawyers, court fees, and settlements related to a claim.

Commercial Property Insurance: Protecting Your Stuff

While general liability protects you from claims by others, commercial property insurance is all about protecting your physical assets. This is the policy that covers your building (if you own it), your inventory, computers, tools, and office furniture. It’s what helps you get back up and running after a fire, storm, or theft.

Let’s say a fire breaks out in your warehouse overnight, destroying thousands of dollars in stock and equipment. Commercial property insurance is what provides the money to repair the building and replace what you lost, so you can actually reopen your doors.

A solid commercial property policy can be the difference between a disastrous event being a temporary setback or a permanent closure.

Workers' Compensation Insurance: The Team Safety Net

If you have employees—even just one—your state almost certainly requires you to have workers' comp. This coverage is a critical deal between you and your team. It gives your employees benefits if they get sick or injured because of their job.

For example, if one of your roofers falls and injures his back, workers' comp is there to cover his medical treatments and a portion of his lost wages while he recovers. The other side of the coin is that by accepting these benefits, employees generally give up the right to sue you over the injury. It’s a system designed to protect everyone.

Professional Liability Insurance: Guarding Your Expertise

This one is also known as Errors & Omissions (E&O) insurance, and it's essential for any business that gives advice or provides a professional service. It protects you from claims of negligence, mistakes, or failing to deliver on what you promised.

Think about an accountant who makes a clerical error on a client's tax return, leading to a costly IRS audit and penalties. The client could sue the accountant for that mistake. Professional liability insurance would step in to cover the legal defense and any resulting settlement. It's one of the key types of commercial insurance coverage for consultants, architects, real estate agents, and many other service professionals.

Cyber Liability Insurance: Your Digital Bodyguard

Just about every business today handles sensitive data, from customer credit card info to employee records. A data breach can be absolutely devastating, and that's where cyber liability insurance comes in. It's designed to help you manage the fallout from a cyberattack.

If a hacker gets into your system and steals customer information, this policy helps cover the massive and immediate costs.

These often include:

- Notifying everyone who was affected.

- Paying for credit monitoring services for victims.

- Hiring a PR firm to handle the reputational damage.

- Covering regulatory fines and legal fees.

Each of these policies plays a unique and vital role. The right mix for your business will form the foundation of your insurance costs, giving you peace of mind that you’re protected from every angle.

The Key Factors Driving Your Insurance Premiums

Ever wondered why your business insurance quote looks so different from the one the company down the street got? It's not random. Insurers are essentially risk analysts, and they have a detailed process for figuring out the likelihood you’ll file a claim.

Think of it as a financial "health check" for your business. Underwriters comb through a specific set of factors to build a risk profile, and that profile is what ultimately determines your business insurance cost. By understanding what they're looking for, you can start to see your business from their perspective and make sense of the numbers.

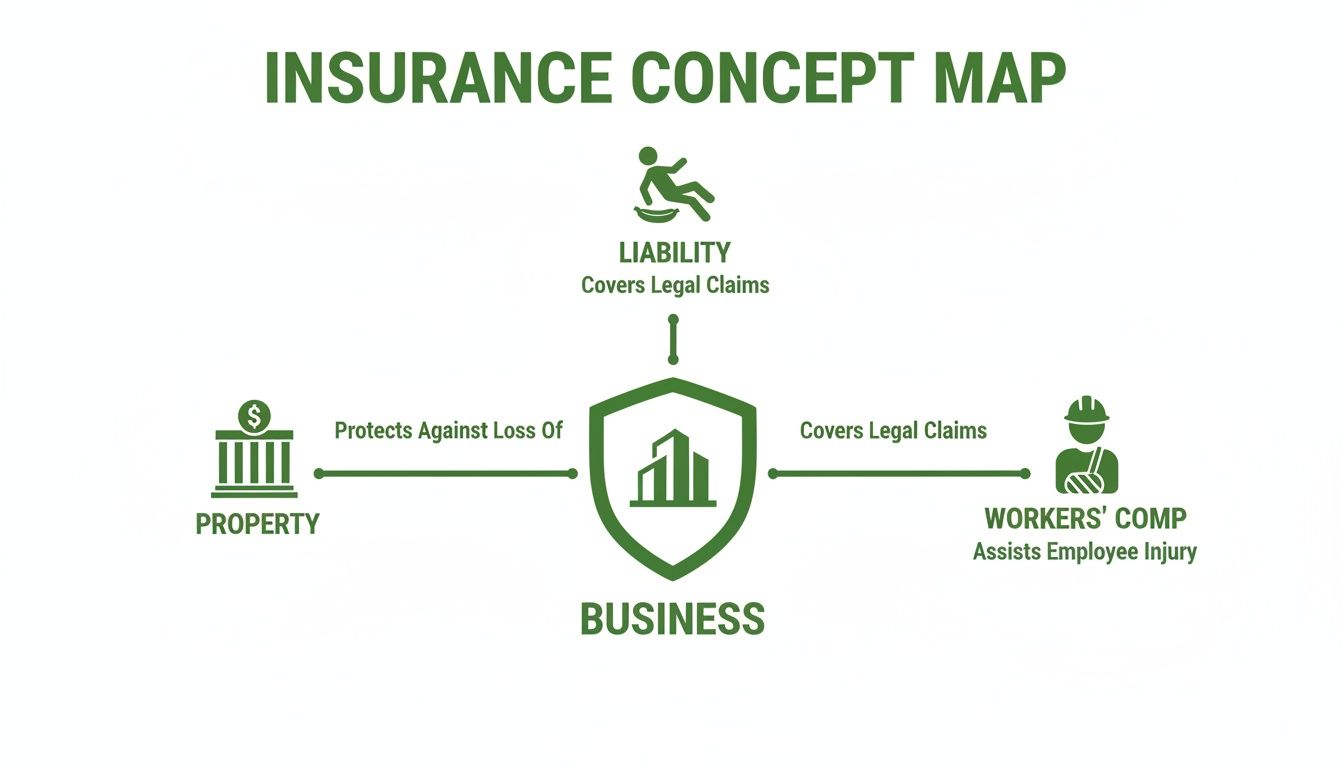

Your Industry and Business Operations

Right out of the gate, the single biggest factor is your industry. A roofer working on steep pitches faces a world of risk that a freelance graphic designer simply doesn't. Insurers lean heavily on decades of data, looking at how often—and how severely—claims happen in different fields. That data sets the baseline.

But it goes deeper than just a job title. What you actually do every day is what truly matters. A quiet bookstore has a much different liability profile than a packed restaurant serving alcohol. The specific services you offer, the machinery you operate, and the environment your team works in are all critical parts of the equation.

This image breaks down how those core operations translate into the major types of insurance you'll need.

Each of these pillars represents a major category of risk that underwriters have to weigh when calculating your final premium.

Business Size and Financials

The sheer scale of your business is another huge piece of the puzzle. When insurers look at size, they're typically focused on two main things:

- Number of Employees: More people on your team usually means a greater chance of a workers' compensation claim. Your total payroll is a direct input for that specific policy's cost.

- Annual Revenue: Higher revenue often corresponds with more customers, larger projects, and just more activity in general. A company bringing in $5 million a year has a lot more exposure than one doing $50,000.

These numbers give underwriters a clear picture of your operational footprint and the potential financial impact if something goes wrong.

Location, Location, Location

It’s an old saying in real estate, but it’s just as true for insurance. Where you set up shop can dramatically affect your rates. A retail store in a high-crime area will naturally pay more for property insurance to cover the higher risk of theft or vandalism.

The same logic applies to geography. If your business is in a hurricane-prone part of Florida or a wildfire zone in California, your premiums will reflect that elevated risk of natural disaster. Even state laws and the local legal climate can have a big impact, especially on liability and workers' comp policies.

Underwriter's Insight: An insurer's goal is to balance the premiums collected against the claims paid out. The global insurance industry is massive, and its growth reflects this constant recalibration. In 2024, the property and casualty segment—which includes many essential business policies—grew by 7.7%, driven heavily by the 8.2% premium increase in North America. These broad market trends ultimately influence the rates available to individual businesses. You can explore the full breakdown of these market dynamics in Allianz's comprehensive Global Insurance Report 2025.

Your Claims History

Nothing tells an underwriter more about your risk level than your track record. If your business has filed a number of claims in the past, you'll be seen as a higher risk, and your premiums will likely be higher. This is especially true for workers' comp, where your claims history directly shapes your experience modification rate—a multiplier that can push your premium up or down.

On the flip side, a clean claims history is proof of a well-run, safe operation, and that can earn you better pricing over time. Prioritizing safety and minimizing accidents is one of the most effective ways you can directly control your insurance costs long-term. You can learn more about how your claims history affects your experience modification rate in our detailed guide.

Coverage Limits and Deductibles

Finally, your premium is directly tied to the coverage you choose. This is where you have the most control.

- Coverage Limits: This is the absolute maximum an insurer will pay for a covered claim. Higher limits offer greater protection, but they come with a higher price tag.

- Deductible: This is the amount you agree to pay out-of-pocket on a claim before the insurance company steps in. A higher deductible tells the insurer you're willing to share more of the risk, which in turn lowers your premium.

It's all about finding the right balance. You're making a strategic trade-off between paying less on your premium now versus potentially paying more out of your own pocket if you have to file a claim later.

Real-World Examples of Business Insurance Costs

Theory is one thing, but nothing brings the concept of business insurance cost to life like real-world examples. The price on your policy isn't just some abstract number; it's a direct reflection of your business's day-to-day operations, the risks you face, and what could go wrong.

To connect the dots, let's walk through three completely different small businesses. Each has a unique risk profile, which means they need a different mix of insurance policies with very different price tags. These stories will help you see how all the factors we've discussed translate into actual dollars and cents.

Profile 1: The Freelance Marketing Consultant

First up is Sarah, a marketing consultant who runs her business from a home office. She works with clients mostly through email and video calls, with the occasional in-person meeting at their office. Her annual revenue is about $90,000, and she works completely solo—no employees.

Sarah’s business is about as low-risk as it gets. There’s no storefront for customers to slip and fall in, she owns very little business property, and she isn’t operating any heavy equipment. Her main exposure comes from the advice she gives. What happens if a marketing strategy she recommended ends up costing a client a lot of money?

Because of this, her insurance needs are pretty straightforward:

- Professional Liability (E&O) Insurance: This is her non-negotiable policy. It’s designed to protect her from claims of negligence or mistakes in her professional advice.

- General Liability Insurance: Even though she works from home, this is a smart move. It covers things like accidentally spilling coffee on a client's expensive laptop during an office visit.

Sample Annual Cost Breakdown:

- Professional Liability ($1M Limit): $650

- General Liability ($1M Limit): $400

- Total Estimated Annual Premium: $1,050

Profile 2: The Small Construction Contractor

Next, let's look at Mike. He runs a small construction company specializing in residential remodels. He has three full-time employees on his crew, operates two work trucks, and brings in around $500,000 a year in revenue.

Mike’s business is on the complete opposite end of the risk spectrum. His team is on active job sites every day, surrounded by power tools, ladders, and heavy materials. This creates a huge potential for both employee injuries and damage to a client's property. The commercial trucks he owns add yet another layer of risk. As you can imagine, the business insurance cost for his company will be much higher.

His insurance package needs to be far more robust:

- Workers' Compensation: This is required by law for his employees and covers their medical bills and lost wages if they get hurt on the job.

- General Liability Insurance: Absolutely critical for covering accidents. Think about a dropped hammer smashing a client's custom tile floor. To learn more about what goes into this policy's pricing, you can read our complete guide to general liability insurance cost.

- Commercial Auto Insurance: Protects his two trucks and covers liability if one of his crew members causes an accident while driving for work.

- Inland Marine Insurance: This policy is designed to cover his expensive tools and equipment while they're being moved to and from job sites.

Sample Annual Cost Breakdown:

- Workers' Compensation (3 Employees): $6,000

- General Liability ($2M Limit): $2,800

- Commercial Auto (2 Trucks): $4,500

- Inland Marine (Tools/Equipment): $900

- Total Estimated Annual Premium: $14,200

Profile 3: The Boutique Coffee Shop

Finally, let's pop into a boutique coffee shop owned by Maria. It’s in a bustling downtown area, does $300,000 in annual sales, and has five part-time employees. She leases the retail space, which is packed with expensive gear like commercial espresso machines and grinders.

Maria's risks are a blend of public liability, property damage, and employee safety. With dozens of customers walking in and out all day, the chance of a slip-and-fall is always present. The combination of hot liquids, food service, and pricey equipment adds to her risk profile.

A Business Owner's Policy (BOP) is the perfect solution for her, as it bundles the main coverages she needs into one package, usually at a discount.

Her protection plan looks like this:

- Business Owner's Policy (BOP): This combines General Liability (for customer injuries) and Commercial Property (to protect her equipment, inventory, and the improvements she's made to the leased space).

- Workers' Compensation: A must-have for her five employees, covering everything from burns from the espresso machine to a slip on a wet floor.

Sample Annual Cost Breakdown:

- Business Owner's Policy (BOP): $1,800

- Workers' Compensation (5 Part-Time Employees): $3,500

- Total Estimated Annual Premium: $5,300

Actionable Strategies to Lower Your Insurance Costs

While many of the factors that shape your business insurance cost might feel out of your hands, you have more control than you probably realize. By getting proactive about how you manage risk, you can make your business a much more attractive client to insurance carriers—and that often translates directly into lower premiums.

It all comes down to showing them you take safety and security seriously. These aren't complicated, overnight fixes. They're practical, common-sense steps you can take to bring down your costs without cutting corners on your protection.

Strengthen Your Risk Management Practices

Hands down, the most powerful way to lower your insurance bill is to reduce the chances you'll ever have to file a claim. A strong safety culture is your best defense against accidents and your most convincing argument for a better rate.

Start by creating a formal, written safety program. This isn't just a binder that sits on a shelf; it's a living document that includes regular employee training on topics that matter to your business. Think proper lifting techniques in a warehouse or cybersecurity awareness in an office. Keep detailed records of every session you run.

Next, turn a critical eye to your physical workspace.

- Improve Security: Install security cameras, a monitored alarm system, and high-quality locks. These are major deterrents for theft and vandalism.

- Enhance Safety: Make sure walkways are clear, lighting is bright and effective, and any potential hazards are clearly marked. If you have company vehicles, a driver safety program is a must.

- Maintain Your Property: Keeping up with regular maintenance on your building and equipment doesn't just prevent accidents; it proves to insurers that you're a responsible owner.

Proactively managing risk isn't just about preventing losses. It's about signaling to your insurance carrier that you are a well-run, low-risk operation deserving of better rates.

Optimize Your Policy Structure

Beyond the physical stuff, how you put your policies together can unlock some serious savings. It's about being smart with your coverage choices and taking advantage of discounts that are often hiding in plain sight.

One of the easiest wins is to bundle your policies. Most insurers offer something called a Business Owner's Policy (BOP), which conveniently packages General Liability and Commercial Property insurance together. Buying them this way is almost always more affordable than purchasing each policy on its own.

Another key lever you can pull is your deductible. That's the amount you pay out of pocket before your insurance starts paying. By choosing a higher deductible, you're agreeing to take on a little more of the initial financial hit yourself, which in turn lowers your annual premium. It's a trade-off, of course, so you need to pick a deductible amount that your business could genuinely afford to pay if something happened.

Stay Informed and Work with an Expert

The insurance world doesn't stand still. Keeping an eye on market trends can help you time your renewals and negotiate better terms. For example, after years of climbing, global commercial insurance rates actually dropped by 4% in the fourth quarter of 2025, the sixth quarter in a row of decreases. That kind of shift, fueled by more competition among insurers, opens up opportunities for business owners. But these trends aren't uniform; the US market stayed relatively flat, and some liability policies even saw rates go up. You can discover more insights about these global insurance market dynamics to stay informed.

This is where having an expert on your side really pays off. A good independent agent can help you make sense of these market shifts. They'll also review your coverage with you every year to make sure it's still the right fit. As your business grows—you add employees, launch new services, or bring in more revenue—your risks evolve, and your insurance needs to keep up.

An annual review ensures you're not underinsured or, just as bad, paying for coverage you don't need anymore. It’s the key to optimizing your business insurance cost for the long haul.

Let's Find the Right Partner for Your Insurance Needs

Trying to figure out business insurance on your own can feel overwhelming. As we've seen, your final business insurance cost isn't some fixed number pulled from a hat; it's something you can actually control. The trick is having someone in your corner to help you make smart decisions without leaving your business exposed.

That’s exactly why teaming up with a real expert makes all the difference. An independent agent isn't tied to one carrier. Instead, they act as your personal shopper in the insurance marketplace, comparing options from dozens of providers to find the best possible price for the coverage you genuinely need. It’s the best way to ensure you're getting robust protection that doesn't break the bank.

It's About More Than Just a Policy

At the end of the day, getting the right insurance is about finding a trusted advisor, not just buying a piece of paper. You need someone who takes the time to understand the real-world risks your business faces, from the daily grind to your biggest growth plans. To get a better feel for this, take a look at our guide on how to choose an insurance broker.

Your goal should be to find an advisor who helps you build a resilient business, offering peace of mind that allows you to focus on what you do best—running your company.

Ready to get a clear picture of what your insurance should cost and build a plan that fits your budget? The team at Wexford Insurance Solutions is here to help. Contact us today for a personalized quote.

Answering Your Questions About Business Insurance Costs

As you dig into business insurance, you'll naturally have a few questions pop up. It's one thing to understand the moving parts, but another to see how they apply in the real world. Let's tackle some of the most common questions we hear from business owners just like you.

Do I Legally Have to Get Business Insurance?

The honest answer? It's complicated. Some policies are required by law, while others are mandated by the people you do business with.

For example, the moment you hire your first employee, nearly every state requires you to have Workers' Compensation insurance. That one is non-negotiable.

Then you have things like General Liability insurance. While it might not be a state law, good luck finding a landlord who will lease you an office or a major client who will sign a contract without seeing proof of it first. In practice, it’s just as essential.

Can I Pay for My Insurance in Monthly Installments?

Yes, absolutely. Insurers get it—cash flow is the lifeblood of any business. Just about every carrier offers a monthly payment plan to help you spread out the cost and keep your budget on track, avoiding a huge one-time hit.

One quick tip, though: always ask if there’s a discount for paying the entire premium upfront for the year. Sometimes you can shave off a few percentage points, and over the long run, those savings really start to add up.

How Often Should I Revisit My Insurance Coverage?

Think of your insurance policies like a business plan—they need to be reviewed and updated as your company evolves. A great habit is to sit down with your agent for a full review at least once a year. Your business isn't the same as it was 12 months ago, so your coverage shouldn't be either.

Beyond your annual check-up, you should get on the phone with your agent immediately after any major change. That means things like hiring new people, moving to a bigger space, buying that expensive new piece of machinery, or rolling out a new service.

What’s the Real Difference Between a Captive and an Independent Agent?

This is a big one, and it can have a major impact on your options and the final business insurance cost. It boils down to choice.

- A captive agent works for one specific insurance company. Think of them as a brand specialist—they know their company's products inside and out, but they can only sell you what that one carrier offers.

- An independent agent, on the other hand, works with many different insurance companies. They can shop around on your behalf, comparing policies and prices from multiple carriers to find the right fit for you. It puts you in a much stronger position.

Having an expert on your side makes all of this much simpler. The team at Wexford Insurance Solutions is here to walk you through the details and find a plan that truly protects what you've built. Get your personalized quote today.

What Does Comprehensive Insurance Cover and Is It Worth It

What Does Comprehensive Insurance Cover and Is It Worth It