For anyone owning a home in New York, insurance isn't just a piece of paper—it's the financial backstop for your single biggest asset. While the state doesn't legally require you to have it, good luck finding a mortgage lender who will give you a loan without it. That makes it a must-have for the vast majority of us.

Think of your policy as a dedicated emergency fund, one specifically designed to help you rebuild your life if disaster strikes.

Why Homeowners Insurance Is Your Financial Safety Net

I like to tell my clients to imagine their home is a ship navigating some pretty unpredictable waters. Your insurance policy is the lifeboat. You hope you never have to use it, but if a storm rolls in—like a burst pipe in your Albany colonial or heavy wind damage on your Long Island roof—that policy is what keeps you from going under financially. It stops one catastrophe from turning into a total economic shipwreck.

This isn't just another bill to pay; it's a core part of being a responsible homeowner. Without it, you're on the hook for everything. The entire cost to rebuild after a fire, replace every stolen laptop and piece of jewelry after a break-in, or cover a guest's medical bills after a fall on your icy steps—it would all come out of your pocket. For most families, those kinds of costs are simply impossible to bear.

The Real Purpose of a Policy

At its heart, homeowners insurance new york is a simple transfer of risk. You pay a predictable, manageable premium to an insurance company. In return, they agree to shoulder the massive, unpredictable financial risks that come with owning a home. It's a trade-off that buys you incredible peace of mind.

This protection goes way beyond just the four walls of your house. It safeguards you in several critical ways:

- Asset Protection: It covers the cost to repair or even completely rebuild your home and other structures, like a detached garage or a shed.

- Personal Belongings: Your policy helps you replace your furniture, electronics, clothes, and other valuables if they're damaged or stolen.

- Liability Shield: This is huge. It defends you against lawsuits and covers medical payments if someone gets hurt on your property, preventing a personal injury claim from wiping out your savings.

A standard policy is designed to put you back in the same financial position you were in before the loss. It’s not meant to be a windfall, but a powerful recovery tool that ensures one terrible day doesn’t derail your entire financial future.

Why Lenders Make It Mandatory

So, if New York State doesn't mandate homeowners insurance, why does your mortgage lender insist on it? Simple: until you pay off that loan, the bank has a massive financial interest in your property. Your insurance policy protects their investment every bit as much as it protects yours.

Look at it from their perspective. If your house burned to the ground and you had no insurance, you'd still legally owe them the full mortgage amount. Most people couldn't afford to rebuild while still paying off the loan for a pile of ashes, which would almost certainly lead to a default. Insurance guarantees the lender gets their money back, making it a non-negotiable part of getting a mortgage. Grasping this is the first real step toward feeling financially secure as a New York homeowner.

What a Standard New York Home Insurance Policy Covers

Think of your homeowners insurance new york policy not as a single shield, but as a multi-tool. Each part has a specific job to do when things go wrong. In New York, the most common policy is the HO-3, and it's the foundation for protecting your home and finances.

Let's break down what's actually inside this policy. Knowing how these pieces fit together is the first step toward making sure you have the right protection and aren't just blindly paying a premium.

Coverage for Your Home and Structures

First up is the big one: Dwelling Coverage (Coverage A). This is the core of your policy, designed to repair or rebuild the physical structure of your house if it gets damaged. We're talking about the roof, walls, foundation, and anything permanently attached, like your kitchen cabinets.

You also get Other Structures Coverage (Coverage B). This protects things on your property that aren't physically connected to your house, like a detached garage, a backyard shed, or the fence around your yard. This is usually set as a percentage of your main dwelling coverage, often around 10%.

Coverage for Your Possessions

Next, there’s Personal Property Coverage (Coverage C). This is what helps you replace all your stuff—furniture, electronics, clothes, you name it—if it’s stolen or destroyed in a covered event. It’s the part of the policy that helps you get back to normal by replacing the everyday items you lost.

To get a fuller picture of how all these coverages interact, our guide on the fundamental home insurance coverage types is a great resource. Just a heads-up: high-value items like jewelry, art, or collectibles usually have strict limits, so you'll likely need a separate add-on to insure them for their full value.

Coverage for You and Your Guests

This is where your policy protects more than just your property. Personal Liability Coverage (Coverage E) is your financial backstop if you're held responsible for someone getting injured at your home. It covers everything from your legal defense fees to court-ordered payouts, up to your policy's limit.

Imagine a guest slips on a wet step and decides to sue. This is the coverage that kicks in. It even follows you off your property in some cases. With over 17,000 dog bite claims filed against homeowners policies each year in the U.S., you can see how crucial this protection really is.

A key New York law (Chapter 545) means an insurer can't cancel your policy or jack up your rates just because of your dog's breed. They can, however, take action if a specific dog is declared dangerous, so being a responsible pet owner is more important than ever.

There's also Medical Payments to Others (Coverage F). Think of this as "goodwill" coverage. It pays for small medical bills if a guest has a minor accident on your property, no matter who's at fault. It's designed to handle small incidents quickly and prevent them from escalating into bigger legal problems.

Coverage for Temporary Relocation

Finally, we have Additional Living Expenses (ALE) Coverage (Coverage D). If a fire or a major storm forces you out of your home during repairs, ALE covers the extra costs you rack up. This includes things like a hotel stay, restaurant meals if you can't cook, and even laundry expenses.

Water damage is one of the most common reasons people have to temporarily relocate. For a closer look at what is and isn't covered, you can find helpful information on homeowners insurance coverage for water damage.

To make it easier to see how these pieces work together, here's a quick summary of what a standard policy includes.

Standard Homeowners Insurance Coverage in New York

| Coverage Type | What It Protects | Example Scenario |

|---|---|---|

| Dwelling (A) | Your home's physical structure, including the roof, walls, and foundation. | A fallen tree damages your roof during a storm, requiring major repairs. |

| Other Structures (B) | Detached structures like garages, sheds, and fences. | Your detached garage is destroyed in a fire. |

| Personal Property (C) | Your belongings, such as furniture, electronics, and clothing. | A burglar steals your laptops and television while you're on vacation. |

| Additional Living Expenses (D) | The increased cost of living if your home is uninhabitable. | You have to stay in a hotel and eat out while your home is being rebuilt. |

| Personal Liability (E) | Your assets if you're sued for injury or property damage. | A visitor slips on your icy driveway, breaks their leg, and sues you. |

| Medical Payments (F) | Minor medical bills for guests injured on your property. | A neighbor's child gets a cut that needs stitches while playing in your yard. |

These six coverages form the backbone of a New York homeowners policy, offering a comprehensive safety net for your biggest investment and your financial well-being.

How Your New York Insurance Premium Is Calculated

Ever wonder why your homeowners insurance premium is so different from your neighbor's, even when your houses look almost identical? It’s not just a number pulled out of thin air. Insurance pricing is a sophisticated calculation of risk, almost like a complex recipe where insurers blend dozens of ingredients to come up with your final policy cost.

For homeowners in New York, that recipe is particularly nuanced. It has to balance the unique details of your property with broader environmental risks and even your personal financial habits. Once you understand what goes into the mix, you can start to see which elements you can actually control to potentially lower your rates.

Your Home's Unique Risk Profile

The single biggest factor is, of course, your home itself—its location, age, and how it was built. A newer home in Albany with all the latest electrical and plumbing is going to look a lot less risky to an insurer than a century-old brownstone in a flood-prone part of Brooklyn.

Insurers dig into the specifics of your property:

- Location, Location, Location: This old real estate mantra is just as true for insurance. A house on the South Shore of Long Island faces a much higher threat from hurricanes and wind damage than a home in Syracuse, and that difference shows up in the premium.

- Construction Materials: It’s simple, really. Homes built with fire-resistant materials like brick or stone are tougher to damage, so they might earn you a better rate than a standard wood-frame house.

- Age of Key Systems: The age and shape of your roof, plumbing, and electrical systems matter a lot. An old roof is a prime candidate for leaks, and outdated wiring is a serious fire hazard in an insurer's eyes.

- Protective Devices: Things like smoke detectors, a central fire alarm, or a burglar alarm system can often lead to discounts. Why? Because they actively reduce the chances of a major loss.

Your Personal History and Choices

Beyond the bricks and mortar, your personal information plays a huge part in setting your premium. Insurers use this data to get a sense of how likely you are to file a claim down the road.

One of the most impactful factors is your insurance score, which is closely related to your credit history. The data shows a strong correlation: people with higher credit scores tend to file fewer claims, so insurers often reward them with lower premiums. Your claims history is also under the microscope. If you've filed several claims in the past few years, an underwriter might see you as a higher risk.

The logic here is that past behavior can be a good predictor of future risk. An insurer might look at a homeowner with a few liability claims and assume they are more likely to have another one, adjusting the premium to match that higher perceived risk.

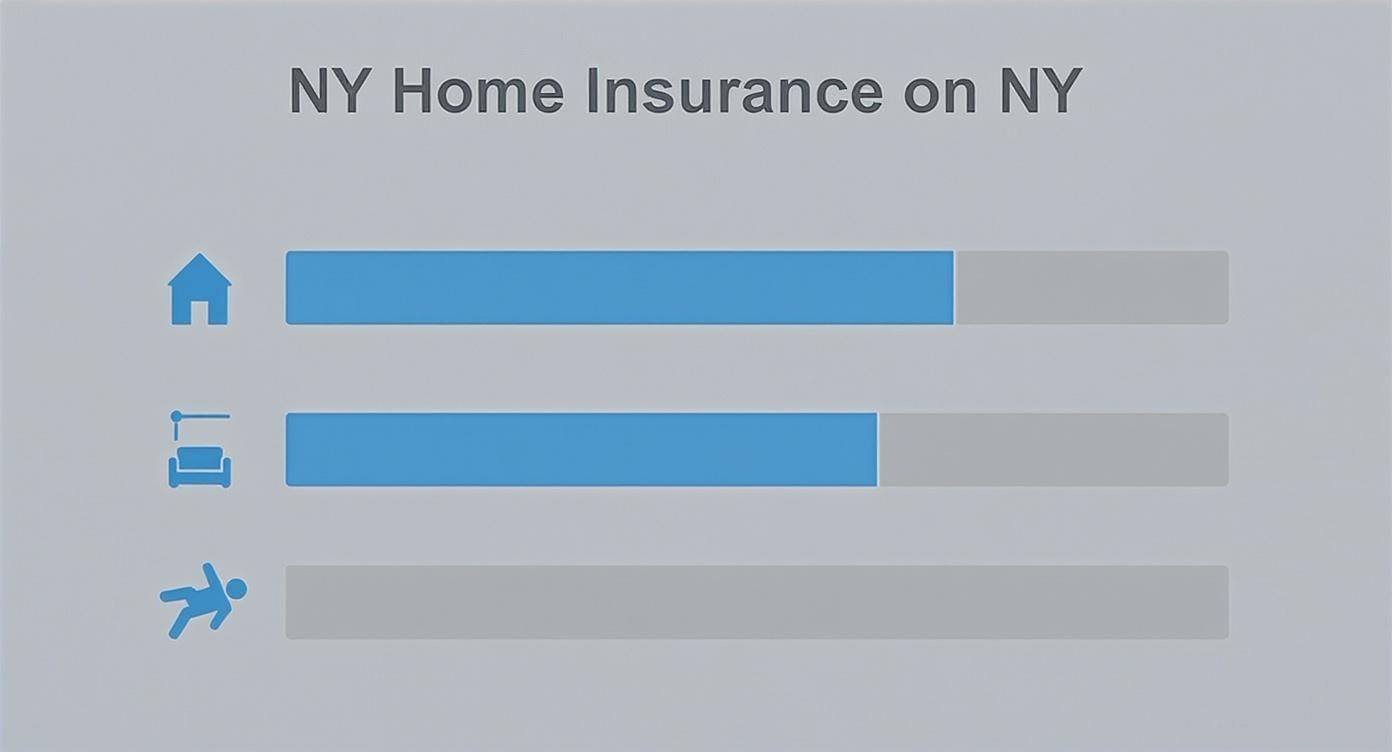

This infographic breaks down how the main policy components—dwelling, property, and liability—all contribute to your overall risk profile.

As you can see, while the structure of your home (dwelling) is the biggest piece of the puzzle, your personal liability and property risks are also major contributors to the final calculation.

The Financial Side of Your Policy

Finally, the coverage decisions you make have a direct line to your wallet. The higher your coverage limits for your dwelling, personal property, and liability, the higher your premium will be. It's a straightforward trade-off: more protection costs more money.

Your deductible is another key lever you can pull. This is simply the amount of money you agree to pay out-of-pocket on a claim before your insurance company starts paying.

- A lower deductible (say, $500) means you pay less when something goes wrong, but your annual premium will be higher.

- A higher deductible (like $2,500) means you’ll have a bigger upfront cost for a claim, but you'll save money on your yearly premium.

Choosing a higher deductible is a popular way to bring down costs, but you have to be honest with yourself. Pick an amount you know you could comfortably pay on short notice. With trends showing that New York home insurance rates are on the rise, these choices are more critical than ever. To get a better handle on these changes, you can read our detailed look at how New York home insurance rates are shifting across the state.

The cost of homeowners insurance in New York is a reflection of all these moving parts. The average annual cost for a standard policy is projected to hit around $1,229 in 2025. But that average hides a huge range. Homeowners in the NYC metro area often pay between $1,700 and $1,800, and those with poor credit could see premiums shoot past $2,400. You can discover more insights about these cost breakdowns and what drives them in this detailed analysis of New York homeowners insurance costs.

Closing Common Gaps in Your NY Home Coverage

Think of your standard homeowners policy as a really good umbrella. It'll keep you dry in a normal downpour, but it's not going to help much if the creek behind your house decides to become a river. A basic policy is a great starting point, but New York's unique mix of coastal weather and inland storms means you need to think beyond the basics.

Pinpointing and closing these coverage gaps is one of the smartest things a homeowner can do. If you don't, you could find yourself holding a policy that lets you down right when you need it, leaving you to foot the bill for a disaster you thought you were insured against.

The Big One: Flood Damage

Let’s get this out of the way immediately: standard homeowners insurance policies in New York do not cover flood damage. This is easily the most common and costly misunderstanding among homeowners. It doesn't matter if the water is from a hurricane storm surge on Long Island, a river overflowing its banks in the Hudson Valley, or a sudden flash flood upstate—your main policy won't cover it.

To protect yourself, you need a separate flood insurance policy. Most people get this coverage through the National Flood Insurance Program (NFIP), which is backed by the federal government, but a growing market of private insurers now offer their own alternatives.

Don't assume you're safe just because you aren't in a high-risk flood zone. FEMA reports that over 25% of all NFIP flood claims come from properties located outside of those designated high-risk areas.

Must-Have Endorsements for New York Homeowners

Beyond major flooding, other common events can leave you with a massive, uncovered bill. Fortunately, you can patch these holes by adding endorsements (sometimes called riders) to your existing policy. Think of them as small, specialized upgrades for specific risks.

Here are a few every New Yorker should consider:

- Sewer and Water Backup: This is a lifesaver. It covers the damage when water backs up through your drains or your sump pump gives out. It's a messy, expensive, and surprisingly common problem that standard policies specifically exclude.

- Scheduled Personal Property: Do you own valuable jewelry, art, collectibles, or high-end camera gear? Your base policy has very low payout limits for these items. This endorsement insures them for their full, appraised value.

- Windstorm Deductibles: If you live in a coastal area like Long Island, insurers often attach a separate—and much higher—deductible just for wind damage. This means you’ll pay a lot more out of pocket for a hurricane claim, so you absolutely need to know your percentage and be prepared for it.

Taking proactive steps, like installing smart water leak detectors, can also go a long way in preventing some of the most common types of water damage.

To really get a handle on your specific risks, a personal review is the best approach. Our guide on how to perform an insurance gap analysis offers a clear framework for spotting where you might be vulnerable. This simple process ensures your homeowners insurance new york policy is truly customized for your home and your life.

A Smart Approach to Shopping for Home Insurance

Finding the right homeowners insurance new york policy can feel overwhelming, but if you break it down into a few simple steps, it's a lot more manageable. The key is to be methodical. Your goal shouldn't be just finding the absolute cheapest price, but securing the best possible value for your home and family.

The whole process kicks off with a clear understanding of what you actually need to protect. This isn't about your home's market value; it's about what it would cost to rebuild it from scratch if a disaster struck. You'll also want to pull together a home inventory—a list of your possessions—to make sure you have enough personal property coverage.

Step 1: Gather and Compare Quotes

Once you know what you need, it's time to see what's out there. The biggest mistake you can make is grabbing the first quote you see and calling it a day. You should always aim to get at least three to five quotes from different insurance companies to get a true feel for what the market looks like.

You have a few solid options for gathering these quotes:

- Go Direct to Insurers: You can always contact big national or regional carriers yourself, either through their websites or over the phone.

- Work with an Independent Agent: This is often a game-changer. An independent agent works with many different insurers, so they do all the heavy lifting and comparison shopping for you.

- Use Online Comparison Tools: Some websites let you enter your details once to get quotes from multiple carriers, which can be a real time-saver.

For a more detailed breakdown, our guide on how to compare home insurance quotes walks you through the entire process. There's no single "best" way—it really comes down to how much time you have and how comfortable you are with the process.

Step 2: Look Beyond the Premium

The lowest price tag is tempting, but it’s rarely the whole story. A cheap policy might hide dangerously high deductibles, major gaps in coverage, or be from a company known for making the claims process a nightmare. As you line up your quotes, you've got to read the fine print.

A policy that saves you $200 a year is no bargain if it leaves you with a $15,000 uncovered claim. The true value of a policy is revealed when you need it most, so comparing coverage details is just as important as comparing prices.

Pay close attention to the coverage limits and exclusions. Look for any special deductibles, too—in New York, it's not uncommon to see a separate, higher deductible for wind damage. It's also smart to check out each insurer's financial strength rating (from services like A.M. Best) and read customer reviews to see how they actually treat their policyholders.

Step 3: Decide How You Want to Buy

The last piece of the puzzle is deciding how you want to buy and manage your policy. Are you someone who wants professional guidance, or do you prefer to handle things yourself?

- Working with an Independent Agent: An agent provides personalized advice, helps you sort through the jargon, and can be your advocate if you ever need to file a claim. This is the way to go if you value having an expert in your corner.

- Buying Directly from the Carrier: If you feel you have a good grasp of insurance and like a do-it-yourself approach, buying directly can be quick and easy. Just remember, you’ll be in charge of all the research and policy decisions.

By following this simple plan—figuring out your needs, comparing quotes beyond just the price, and choosing how you want to buy—you can lock in a homeowners insurance new york policy that gives you solid protection and real peace of mind.

Actionable Ways to Lower Your Insurance Premiums

While homeowners insurance is a non-negotiable expense for New Yorkers, the premium you pay isn't set in stone. The good news is that you have more control than you might think. With a little proactive effort, you can find real savings without cutting corners on your coverage.

Think of it this way: insurers reward homeowners who actively reduce risk. Every smart upgrade, policy tweak, and even your loyalty can chip away at your annual costs. It's all about making your home a safer bet for them, which translates directly into savings for you.

Unlock Common Discounts

The quickest wins often come from discounts you might already qualify for. Insurance companies have a whole menu of them, but they won't always hand them out unless you ask.

It's always worth starting a conversation with your agent about these popular options:

- Bundling Policies: This is the big one. Combining your home and auto insurance with the same carrier is one of the easiest and most effective ways to save. You could see your total premium drop by as much as 15-20%.

- Home Security Systems: A centrally monitored alarm system that alerts the police or fire department is a huge plus. It shows you're serious about protecting your property, and insurers will often reward you for it.

- Protective Devices: Little things can add up. A newer roof, storm shutters, or even just having fire extinguishers handy can sometimes trim your costs.

These discounts aren't just arbitrary; they reflect the fact that a well-protected home is a less risky one to insure. For a more detailed breakdown, check out our guide on how to lower home insurance premiums.

Re-Evaluate Your Deductible

One of the most direct levers you can pull to adjust your premium is your deductible. This is simply the amount you agree to pay out-of-pocket on a claim before your insurance kicks in. By choosing a higher deductible, you're taking on a bit more of the initial risk yourself, and your insurer will thank you with a lower premium.

Here's a powerful example: Increasing your deductible from $500 to $1,000 can potentially save you up to 25% on your annual premium. It's a strategic trade-off that puts you in the driver's seat.

Just be realistic. Before you bump it up, make sure you could comfortably cover that new deductible amount tomorrow without it causing a financial headache.

Maintain a Strong Insurance Score

In New York, insurance companies often look at what's called an "insurance score" to help determine your rates. This score is heavily influenced by your credit history. A solid track record of paying bills on time and managing debt responsibly signals that you're a reliable, lower-risk client. Keeping your credit in good shape is a long-term strategy for securing better insurance rates.

Speaking of costs, premiums can vary quite a bit across the state. Most New York homeowners find themselves paying somewhere between $1,000 and $1,499 each year. You can discover more insights about these costs and trends on Realtor.com, which does a great job of explaining the different risk factors behind those prices.

Ready to see how these strategies stack up? Here’s a quick-reference table to help you identify the best ways to start saving.

Effective Ways to Reduce Your New York Home Insurance Premium

| Strategy | Potential Savings | What's Involved |

|---|---|---|

| Bundle Home & Auto | 15-20% | Insuring your home and vehicle(s) with the same company. |

| Increase Deductible | Up to 25% | Choosing a higher out-of-pocket amount for claims (e.g., from $500 to $1,000). |

| Install Security Systems | 5-15% | Installing centrally monitored smoke and burglar alarms. |

| Improve Your Credit | Varies | Maintaining a good credit history by paying bills on time. |

| Make Home Upgrades | Varies | Installing a new roof, updating wiring, or adding storm shutters. |

| Ask About Discounts | Varies | Inquiring about loyalty programs, claims-free history, or other available price breaks. |

By regularly reviewing your policy and actively seeking out these opportunities, you can ensure you’re not just covered, but that you're paying a fair price for your specific situation.

Got Questions? Let's Get You Some Answers

When it comes to homeowners insurance new york, a few key questions come up time and time again. Getting these right is crucial, so let's walk through the most common ones to make sure you're crystal clear on how your protection works.

Is Homeowners Insurance Mandatory in New York State?

Officially, no. The state government doesn't have a law forcing you to buy homeowners insurance. But don't let that fool you. If you have a mortgage, your bank or lender absolutely will require it as part of your loan agreement.

Think of it from their perspective: they have a massive financial investment in your property. They need to know that if something disastrous happens, their investment won't literally go up in smoke. So for nearly every homeowner with a mortgage, insurance isn't optional—it's a must-have.

Does My Policy Cover Hurricanes and Floods?

This is a huge one for New Yorkers, and the answer is tricky: it covers one but not the other. A standard home policy will cover damage from a hurricane's powerful wind, but it will not cover damage from the storm surge or rising water that often comes with it. That’s considered flooding, which is a specific exclusion.

To be truly protected, you need a separate flood insurance policy. Most people get this through the National Flood Insurance Program (NFIP), though some private insurers offer it too. Also, be aware that policies in coastal areas often have a separate (and higher) "hurricane deductible" for wind damage claims.

How Is Insurance Different for a Co-op or Condo?

Insuring a co-op or condo is a whole different ballgame. You’ll have what’s called an HO-6 policy, which is designed to work alongside the building’s master policy. The master policy covers the big stuff—the building's structure, the roof, and common areas like the lobby.

Your personal HO-6 policy picks up where that leaves off, covering everything from the "walls-in." This typically includes:

- Your stuff: All your furniture, clothes, and electronics.

- The inside of your unit: Things like your kitchen cabinets, flooring, and light fixtures.

- Upgrades: Any renovations or improvements you've made.

- Personal liability: This protects you if a guest is injured inside your apartment.

Getting this right means knowing exactly what the building's master policy covers. Your job is to buy an HO-6 policy that fills in the rest, leaving no expensive gaps in your coverage.

What’s the First Thing I Should Do When Filing a Claim?

Your immediate priority is safety. After a loss, do what you can to prevent more damage, like throwing a tarp over a hole in your roof. But before you start any major cleanup, stop and document everything. Take photos and videos of the damage from every possible angle.

Once you and your family are safe, call your insurance agent or the company's claims hotline right away. From that point on, keep a detailed record of every single conversation—who you spoke to, the date, and what was said. And hang on to every receipt for temporary repairs, hotel stays, or other expenses you have to cover while displaced.

Figuring out the ins and outs of homeowners insurance new york is what we do best. The independent agents at Wexford Insurance Solutions are here to cut through the complexity and find you the right protection for your home and budget. We make it simple, so you can feel secure. Secure your free, no-obligation quote today at https://www.wexfordis.com.

Insurance Options for Small Business: A Quick Guide7 Best Homeowners Insurance New York Providers for 2025

Insurance Options for Small Business: A Quick Guide7 Best Homeowners Insurance New York Providers for 2025