Even the most careful professional can make a mistake. An overlooked detail, a missed deadline, or advice that doesn't pan out can have serious financial consequences for your clients—and in turn, for your business. That’s where Errors & Omissions (E&O) insurance comes in.

Think of it as your professional safety net, designed to protect you and your company from claims of negligence or failure to perform your professional duties. If a client sues, alleging your work caused them a financial loss, an E&O policy covers the staggering costs of legal defense and potential settlements.

What Is Errors And Omissions Insurance, Really?

Simply put, E&O insurance is like malpractice coverage, but for a much wider range of service-based professions. While a general liability policy handles physical risks like someone slipping in your office, E&O is all about protecting you from the financial fallout of your services or advice.

It’s a critical shield in a world where a simple mistake—or even a completely unfounded accusation—can trigger a lawsuit that costs you a fortune to fight.

Here's the key thing to remember: even if you did nothing wrong and the claim is baseless, you still have to pay to defend yourself. An E&O policy steps in immediately to cover attorney fees, court costs, and any judgments or settlements, preventing a single lawsuit from bankrupting your business.

Who Truly Needs This Coverage?

If you provide a service or expert advice for a fee, you should be seriously considering E&O insurance. The risk isn't confined to just a few high-stakes fields; it's a reality for any professional whose clients depend on their expertise to make important decisions.

Without this specific protection, your business assets—and sometimes even your personal ones—are on the line.

Here’s a look at some of the professions that need E&O insurance and why.

Professions That Need E&O Insurance

| Profession / Industry | Common Risks Covered by E&O | Example Scenario |

|---|---|---|

| Consultants | Negligent advice, failure to deliver promised outcomes, project mismanagement. | A business consultant’s strategic advice leads to a significant drop in a client's revenue, prompting a lawsuit for the financial losses. |

| IT Professionals | Software bugs, data breaches, system implementation errors, service outages. | A software developer's code has a bug that crashes a client's e-commerce site during a major sale, causing massive business interruption losses. |

| Architects & Engineers | Design flaws, errors in calculations, failure to meet building codes, project delays. | An architect's design contains a flaw that requires costly rework during construction, and the project owner sues for the additional expenses. |

| Real Estate Agents | Failure to disclose property defects, errors in paperwork, misrepresentation of a property's value. | A real estate agent neglects to disclose a known foundation issue, and the buyer sues for the subsequent repair costs after the sale closes. |

| Accountants | Incorrect tax advice, bookkeeping errors, audit mistakes, poor financial guidance. | An accountant provides flawed tax advice that results in a client facing significant IRS penalties and back taxes. |

The common thread here is clear: if your knowledge is your product, you have a professional liability risk that needs to be managed.

More Than Just Insurance—It’s a Business Necessity

In today's business world, carrying a solid E&O policy is more than just a smart defensive move; it's often a requirement to even get in the door. Many clients, especially larger corporations and government agencies, won't sign a contract without proof of insurance.

Having this coverage shows you're a professional who stands behind your work and has the financial stability to make things right if a mistake happens. It builds trust and credibility.

The demand for this protection is surging. The global E&O insurance market was valued at USD 15 billion in 2023 and is expected to hit USD 25 billion by 2032. This isn't just a random trend; it shows a growing awareness among business owners that they need to shield themselves from these specific risks.

As you evaluate your own needs, it's helpful to see how this policy fits with others. For a deeper dive, check out our guide on the differences between professional and general liability insurance.

So, What Does Your E&O Policy Actually Cover?

Think of an errors & omissions insurance policy like learning the rules of a game before you start playing. Knowing what moves are covered—and which ones are out of bounds—is the only way to really protect yourself. At its heart, this insurance is designed to cover the financial losses a client suffers because of a professional mistake you made.

This isn't about covering intentional harm. It's about acknowledging the human element of error that can find its way into any service-based business, no matter how careful you are.

Let’s dig into the specific professional missteps your policy is built to handle.

Key Areas of Coverage

Your E&O policy is your financial backstop when a client claims your work caused them harm. While the exact wording differs from one policy to the next, the coverage typically centers on a few core areas.

These protections are what pay for your legal defense, any settlements you reach, and court-ordered judgments, all the way up to your policy limit.

- Alleged Negligence: This is the big one and the most common reason for a claim. It means a client believes you failed to use the same level of care that any other reasonable professional in your shoes would have. Imagine an architect whose design plans have a structural miscalculation, leading to expensive construction delays. That’s a classic negligence claim.

- Errors and Mistakes: This covers straightforward, honest mistakes in your work. Picture an accountant who makes a simple data entry error on a tax return, causing their client to face hefty IRS penalties. The E&O policy would be there to respond to the client's claim for that financial loss.

- Omissions: An omission is all about what you didn't do. It’s when you fail to perform a necessary action or leave out a critical piece of information. For instance, a real estate agent who forgets to disclose a known plumbing issue could face a lawsuit when the new homeowner discovers an expensive, watery mess.

- Misrepresentation: This happens when you make inaccurate statements or give misleading advice that a client relies on, only to lose money. A marketing consultant who guarantees a 200% ROI in a signed contract but doesn't deliver could get sued for misrepresenting the results they could achieve.

An E&O policy is your financial shield for professional judgment calls that, in hindsight, turn out to be incorrect and cause a client a monetary loss. It covers the gap between your best intentions and an imperfect outcome.

What's Not Covered: Common Exclusions

Just as important as knowing what’s covered is understanding what’s not. E&O insurance is a highly specific tool; it is not a catch-all policy for every possible business risk. Being crystal clear on these boundaries helps you avoid dangerous gaps in your protection.

Most E&O policies will not cover the following situations:

- Intentional or Criminal Acts: If you or an employee commits fraud, deliberately harms a client, or does something illegal, your E&O policy won’t be there for you.

- Bodily Injury or Property Damage: These claims are what General Liability insurance is for. If a client trips over a cord in your office and breaks their arm, that’s a general liability claim, not an E&O matter.

- Employee-Related Claims: Lawsuits from your own staff over issues like wrongful termination or discrimination are handled by a completely different policy called Employment Practices Liability Insurance (EPLI).

- Your Own Business Losses: E&O is built to cover your liability to third parties—your clients. It won't pay for your own financial losses if a project goes over budget or a new service you launched doesn't pan out.

While an E&O policy provides broad protection, it’s also smart to understand specific contractual tools like an indemnification clause to better manage your liability. For a complete picture of your coverage, learn more about what professional liability insurance covers in our detailed guide.

Real-World Scenarios Where E&O Saved a Business

Reading about insurance can feel a bit abstract. So, let’s get down to brass tacks. The best way to understand the real power of errors & omissions insurance is to see how it works in the real world when things go wrong.

A simple mistake, an oversight, or a promise you couldn’t keep can quickly escalate into a lawsuit that puts your entire business on the line. These stories show exactly how E&O acts as a financial backstop, turning a potential disaster into a manageable problem.

The IT Consultant and the Costly Crash

An IT consultant, well-respected in his field, was hired to upgrade a logistics company’s servers and patch a critical vulnerability. It was a routine job. But during the update, a hidden software conflict brought the client's entire inventory and shipping system to a screeching halt.

For 48 hours, the company was flying blind. They couldn't track shipments, manage their warehouse, or process orders. The financial fallout was immediate and severe, leading to hundreds of thousands in losses from delays, penalties, and emergency workarounds.

The client hit the consultant with a $350,000 negligence lawsuit. Without insurance, the legal fees alone would have been a massive blow, never mind a potential judgment. Thankfully, his E&O policy sprang into action, covering his legal defense and ultimately paying the $185,000 settlement that let him keep his business afloat.

The Marketing Agency and the Unmet Promise

A sharp digital marketing agency landed a big contract with an e-commerce startup, promising a 40% boost in online sales within six months. They wrote that specific number right into the contract—a bold but confident move.

But even with a solid strategy and a big ad budget, the results fell short. Sales only climbed by 15%. The client was furious. They sued for breach of contract, demanding a full refund of their $90,000 in fees, arguing the agency failed to deliver on its professional promise.

This is a textbook E&O claim. The policy covered the agency’s defense costs from day one. In the end, their insurer’s legal team negotiated a settlement that involved refunding a portion of the fees. The policy paid for it, saving the agency from a huge cash-flow crisis and a very public legal fight.

An Errors & Omissions policy is designed for exactly these situations—where the quality of your professional service is questioned and a client seeks financial damages as a result. It defends your work and your finances.

The Architect and the Design Flaw

An architectural firm drafted the plans for a new commercial building. Everything looked perfect on paper. But as construction neared completion, a contractor on-site found a major problem: the HVAC ductwork design didn't account for several structural beams.

The only way to fix it was to tear down newly built walls and completely reroute the system. The mistake added $120,000 to the project cost and delayed completion by two months. The building’s owner immediately sued the firm to cover the damages.

The firm’s E&O insurance was its lifeline. It paid for the lawyers and the settlement that covered the expensive rework. For any professional whose work involves precise calculations and plans—like architects and engineers—a tiny error can have six-figure consequences. This kind of protection isn’t just nice to have; it’s essential.

These examples show just how fast a project can go sideways. Having the right insurance plan is what makes the difference between a bump in the road and the end of the road. If you ever find yourself in a similar spot, it helps to be prepared. You can learn more about how to file an insurance claim in our step-by-step guide.

How Policy Limits and Deductibles Work

When you’re looking at an errors & omissions insurance policy, the numbers can feel a bit abstract. But understanding your policy limits and deductibles is probably the most important part of making a smart financial choice. These two levers control how much protection you actually have and what you'll pay for it.

Think of them as the blueprints for your financial safety net. The limits set the maximum amount your insurer will ever pay for a covered claim. Your deductible, on the other hand, is the amount you agree to pay yourself before the insurance company steps in.

Breaking Down Your Policy Limits

Your E&O policy will almost always have two distinct limits. It’s critical to know the difference, because they work together to protect your business.

- Per-Claim Limit: This is the absolute maximum your insurance provider will pay out for any single lawsuit or claim. So, if your per-claim limit is $1 million, that's the ceiling for everything related to one incident—legal fees, settlements, you name it.

- Aggregate Limit: This number represents the total amount your insurer will pay for all claims you file during your policy period, which is usually one year. If you have a $2 million aggregate limit, you could have multiple claims, but the grand total paid out by the insurer can't go over that amount for the year.

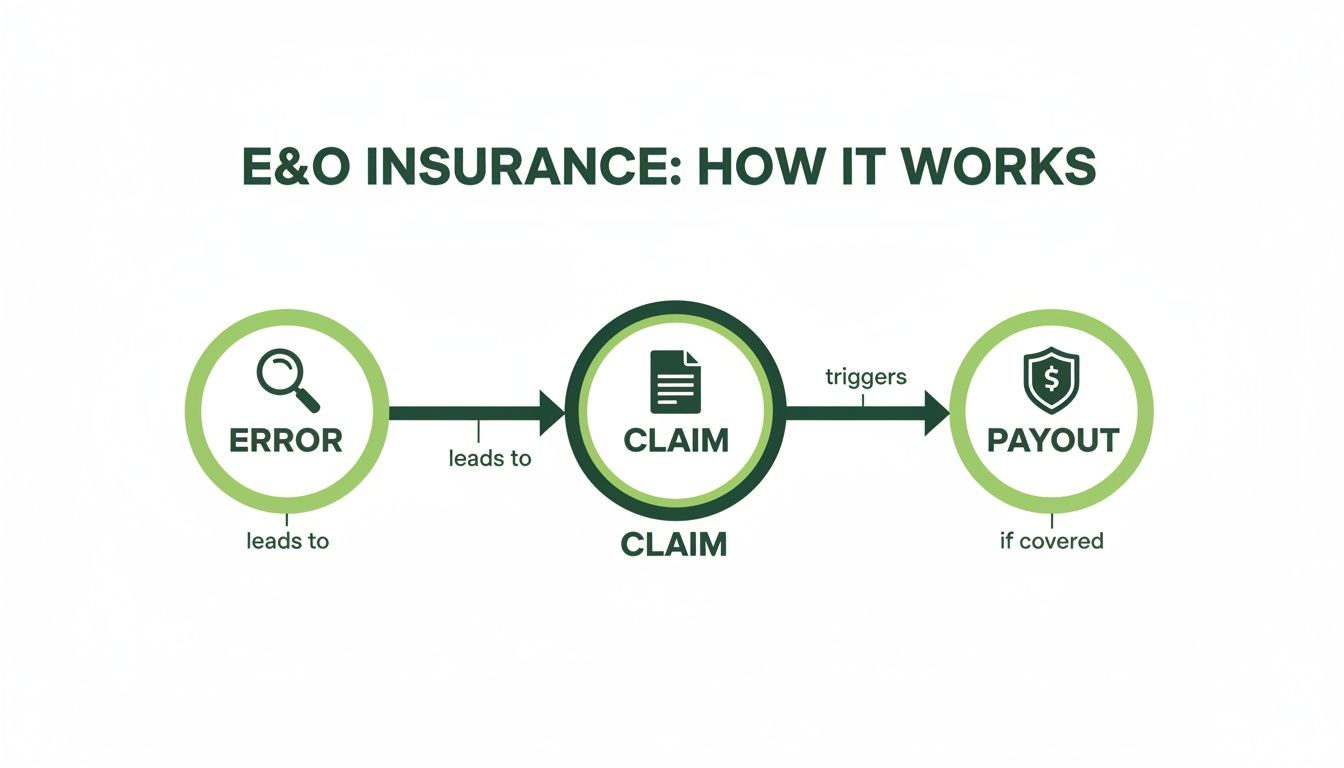

This simple flowchart shows how a professional mistake can quickly turn into a financial event where your E&O coverage becomes essential.

As you can see, a professional error doesn't just disappear. It can easily trigger a client claim, and that’s precisely when your E&O policy is supposed to kick in and cover the financial fallout.

Understanding Your Deductible

The deductible is simply the portion of a claim you have to pay out of your own pocket before your insurance coverage starts.

Let’s say you face a covered claim for $50,000 and your policy has a $5,000 deductible. You’d pay the first $5,000, and your insurer would handle the remaining $45,000. It’s that straightforward.

A good rule of thumb: opting for a higher deductible usually means a lower annual premium. Why? Because you're agreeing to take on more of the initial risk. Just be sure to pick a deductible that your business could genuinely afford to pay without hesitation if a claim pops up.

If you want to get into the weeds on this, we have a whole guide on what a deductible in insurance is that breaks down how it fits into your broader financial picture.

What Drives Your E&O Premium Cost

Ever wonder how an insurer lands on a specific price for your policy? They're weighing a handful of key risk factors to figure out the likelihood you'll file a claim.

Here’s what’s on their checklist:

- Your Industry: High-stakes fields are a bigger risk. Architects, financial advisors, and lawyers often see higher premiums because a single mistake can have massive financial consequences for a client.

- Annual Revenue: More revenue often means bigger projects and more on the line, which can nudge your premium upwards.

- Claims History: If you have a track record of past claims, an insurer sees you as a higher risk. That will almost always translate to a higher cost.

- Policy Limits and Deductible: This one’s a trade-off. Higher coverage limits will cost more, while choosing a higher deductible can bring the price down.

It’s also worth noting that the market itself is seeing more claims, particularly for professionals like lawyers, agents, and accountants who are often required to carry E&O coverage by contract. For many, claims for the "cost of correction"—fixing a mistake before it becomes a lawsuit—are a major driver, which really underscores the value of having a solid policy in place.

Comparing E&O With Other Business Insurance

The world of business insurance can feel like an alphabet soup of policies. When you’re trying to protect your company, it’s easy to get lost in the jargon and wonder what you actually need. Think of it like a toolkit: you need the right tool for the right job.

Errors and omissions insurance is a highly specialized tool. Its job is very different from other, more common policies. Mistaking one for the other can leave you with a dangerous gap in your coverage just when you need it most. Let's break down the key differences.

E&O vs. General Liability Insurance

This is the most common point of confusion for business owners. The simplest way to tell them apart is to think about the type of damage being claimed.

- General Liability Insurance is for the physical world. It covers tangible risks like bodily injury or property damage. If a client slips on a wet floor in your office or you accidentally knock over their expensive server, that's a job for your general liability policy.

- Errors & Omissions Insurance, on the other hand, deals with financial harm. It's for claims of financial loss caused by your professional advice or services. If your bad accounting advice results in a huge IRS penalty for your client, that's squarely in E&O territory.

In short, general liability is for when your business physically hurts someone or something. E&O is for when your professional work financially hurts them.

E&O vs. Cyber Liability Insurance

As nearly every business becomes a tech business, the line between E&O and Cyber Liability can get blurry. They both deal with digital risks, but they cover fundamentally different types of failures.

The insurtech E&O market alone is projected to grow from USD 3.67 billion in 2025 to USD 14.09 billion by 2035, a clear sign of how crucial this coverage has become.

- Cyber Liability Insurance is your defense against data breaches and security failures. If a hacker steals customer credit card numbers or a ransomware attack locks up your network, your cyber policy steps in to cover everything from forensic investigations and notification costs to credit monitoring.

- Technology E&O Insurance covers the failure of your actual tech service or product. If a bug in your custom software corrupts a client's database, or your cloud hosting service goes down and costs them a day's worth of sales, that’s a Tech E&O claim. It's about your service not working as promised.

To give you a clearer picture, here's a simple breakdown of how these policies stack up against each other.

E&O vs General Liability vs Cyber Insurance

| Policy Type | Primary Purpose | Typical Covered Claim |

|---|---|---|

| Errors & Omissions (E&O) | Covers financial loss due to professional negligence, errors, or failure to perform a service. | An architect's design flaw leads to costly structural repairs for a client. |

| General Liability | Covers bodily injury and property damage to third parties caused by your business operations. | A customer slips and falls in your retail store, breaking their arm. |

| Cyber Insurance | Covers financial losses resulting from data breaches and other cyber threats. | A hacker steals your customer database, and you must pay for credit monitoring. |

Understanding these distinctions is the key to building a complete protective shield around your business. Each policy is designed to respond to a specific type of threat.

It's also important to remember that E&O doesn't cover everything. For instance, claims from your own employees related to wrongful termination or discrimination fall under Employment Practices Liability (EPLI). To get even deeper into policy structures, it's also helpful to understand the crucial difference between claims-made vs. occurrence coverage.

Finding the Right E&O Partner for Your Business

Getting a handle on how errors & omissions insurance works is step one. But the next step is arguably the most critical: picking the right partner to help you get that coverage in place. This isn’t just about shopping for the lowest price—it's about finding a true expert who can look at your unique business risks and translate them into a policy that actually protects you.

A generic, off-the-shelf policy might look good on paper, but it's often riddled with gaps that you won't discover until you're trying to file a claim. The right insurance partner acts more like a risk advisor, making sure your coverage is built around your specific industry, the services you provide, and the contracts you sign. This isn't a luxury; it’s a core part of managing your business wisely.

When you work with an expert, you’re getting more than just a policy. You’re getting an advocate who’s in your corner for the long haul, from the first quote to helping you through the headaches of a claim.

The Wexford Advantage: Human Expertise Meets Modern Convenience

Here at Wexford Insurance Solutions, we bring old-school insurance know-how together with the ease of modern technology. We get it—you need straight answers and simple access to your information, but you don't want to give up the guidance of someone who’s seen it all before. Our whole approach is designed to make managing your errors & omissions insurance feel straightforward, not overwhelming.

We operate on a few core beliefs:

- A Real Risk Assessment: We always start by learning about your business. We dig into your operations, review your contracts, and identify the specific risks tied to your industry. Only then can we recommend limits and endorsements that actually make sense for you.

- Intelligent Claims Advocacy: If you ever have to file a claim, you won't be on your own. We become your advocate, working with the insurance carrier to push for a fair and timely resolution. It makes a stressful situation a lot more manageable when you have an expert on your side.

- A Seamless Digital Experience: You can manage your policy, grab documents, and handle payments whenever it works for you through our secure 24/7 client portal. It’s the convenience you need, with the human support you deserve.

Your E&O policy should give you confidence, not create more confusion. The right partner turns your insurance into a powerful asset that protects everything you've worked so hard to build, freeing you up to focus on running your business.

Secure Your Professional Peace of Mind

Don't leave your business vulnerable to the financial fallout of a professional liability lawsuit. Even a groundless claim can drain your bank account and tarnish the reputation you've spent years building. Getting the right errors & omissions insurance is one of the smartest moves you can make for the future of your company.

Ready to find a policy that works as hard as you do? Contact Wexford Insurance Solutions today for a professional risk assessment. Let us help you secure the coverage that brings you true peace of mind.

Answering Your Top E&O Insurance Questions

When you start digging into the specifics of errors and omissions insurance, a few key questions always seem to pop up. Getting these details right is crucial, because they often determine whether you're fully covered or exposed to a nasty surprise when you need your policy most. Let’s walk through the common questions we hear from professionals every day.

Claims-Made vs. Occurrence Policies: What’s the Real Difference?

This is probably the most important concept to grasp in the world of E&O insurance. The overwhelming majority of E&O policies are claims-made. In simple terms, this means the policy that pays out is the one you have active when the claim is actually filed against you, not when the work was done. There's a catch, though: the incident must have happened after a specific date listed in your policy, known as the "retroactive date."

On the flip side, you have occurrence policies, which are quite rare for E&O. These cover any incident that happens during the policy period, regardless of when the client decides to sue you, even if it's years later. Since almost all E&O is claims-made, it's absolutely vital to keep your coverage continuous. Letting it lapse could leave all your past work completely unprotected.

When Should I Report a Potential Claim?

The second you even think a claim might be coming, you need to call your insurance provider. Don't wait for a formal lawsuit. A threatening email from a client, a formal demand letter, or even a conversation where they blame you for a financial loss—these are all triggers.

Policies have strict rules about reporting, and being early is always the right move. Giving your insurer a heads-up allows them to get ahead of the problem, perhaps by providing legal advice or starting an investigation. This early action can often de-escalate a situation before it turns into a massive, expensive lawsuit.

Do not wait. The moment a client expresses serious dissatisfaction with your professional services and hints at financial damages, it's time to contact your insurance partner. Early intervention is your best defense.

But I Have an LLC. Don't I Already Have Protection?

This is a very common—and very dangerous—misconception. Yes, an LLC or corporation can help protect your personal assets (like your house or car) from business liabilities. But it does absolutely nothing to protect the business itself from being sued.

A disgruntled client will sue your company directly. If they win, they can go after your business's bank accounts, equipment, and other assets. Errors & omissions insurance is what protects the business entity. It's the policy that pays for the lawyers and any potential settlement, ensuring one mistake doesn't sink the entire company you worked so hard to build.

Can I Get Coverage for Work I Did in the Past?

Yes, and this is where the retroactive date on your policy comes into play. When you first purchase a claims-made policy, you can often negotiate a retroactive date that covers work you’ve completed in the past.

This is a lifesaver for any professional who has been operating without insurance for a while. It’s also critically important when you switch insurers. You must make sure your new policy picks up the exact same retroactive date from your old one. If it doesn't, you’ve just created a massive gap in coverage, leaving all your prior work exposed.

Protecting your business from professional liability requires a clear strategy and the right partner. At Wexford Insurance Solutions, we specialize in crafting E&O policies that align with your specific risks, ensuring you have the robust protection you need. To build a true financial safety net for your professional services, visit Wexford Insurance Solutions and get a personalized risk assessment today.

Protect Your Business with commercial umbrella insurance

Protect Your Business with commercial umbrella insurance