Think of your business insurance like a financial first-aid kit. You have your primary policies—General Liability, Commercial Auto, Employer’s Liability—ready for the everyday cuts and scrapes. They’re absolutely essential.

But what happens when a true emergency strikes? A catastrophic, multi-million dollar lawsuit isn't a simple scrape; it's a threat to the entire life of your business. This is where commercial umbrella insurance comes in. It's not just another policy; it's your ultimate financial safety net.

Your Ultimate Financial Safety Net

Imagine your main insurance policies are the first responders. Your General Liability policy handles a slip-and-fall at your office. Your Commercial Auto policy covers a fender bender. They are your first, and most important, line of defense for specific risks.

The problem is, in our very litigious world, the costs of a single major incident can easily blow past the limits of those primary policies. A multi-car pileup caused by a company driver, a devastating injury on your property, or a major professional error can lead to judgments and legal bills that dwarf a standard $1 million policy limit.

This is exactly when a commercial umbrella policy goes to work. It’s not a standalone product. Instead, picture it as a massive, reinforced canopy that sits over your existing liability policies. Once the limit on one of those policies is exhausted, the umbrella kicks in, providing an additional layer of protection, usually in increments of $1 million or more.

An umbrella policy does more than just add a bigger number to your coverage. It gives you critical breathing room, ensuring one catastrophic event doesn’t become a business-ending disaster. It’s what protects your hard-earned assets and secures your company's future.

The Growing Need for Broader Protection

The demand for this kind of high-level protection isn't just a niche concern anymore—it’s a rapidly growing market reality. The commercial umbrella insurance market is forecast to jump from USD 19,639.88 million in 2025 to an incredible USD 39,711.83 million by 2033.

Fueling this is a powerful 9.2% compound annual growth rate (CAGR), which clearly shows that businesses are waking up to the escalating risks they face. You can dive deeper into these trends and what's driving them in the full report on commercial umbrella insurance growth.

This isn't just a "big corporation" problem. Small and mid-sized businesses are just as exposed. A single verdict could force you to sell off assets, empty cash reserves, or even shut your doors for good.

Primary Policies vs Commercial Umbrella Insurance At a Glance

To see how these policies work together, it helps to compare them side-by-side. Your primary policies are the foundation, while the umbrella is the essential reinforcement.

| Coverage Type | What It Covers | When It Activates | Typical Role |

|---|---|---|---|

| Primary Policies | Specific liability claims like third-party injury (General Liability) or at-fault vehicle accidents (Commercial Auto). | Immediately after a covered incident occurs. | Your first line of defense for common liability risks. |

| Commercial Umbrella | The same types of claims as the underlying policies, but only after their limits are maxed out. | Only after the full limit of a primary policy has been paid out. | A secondary, high-limit layer of protection for catastrophic events. |

This table shows the clear distinction: the umbrella doesn’t replace anything. It simply adds a crucial layer of security on top.

A Key Piece of Your Insurance Puzzle

Understanding how umbrella coverage fits into your overall risk management strategy is key. It's a complementary policy, not a replacement. In fact, insurers require you to have specific primary policies in place with certain minimum limits before they will even issue an umbrella policy. To see how this fits with other essential protections, you can learn more about the different types of commercial insurance coverage every business should consider.

Ultimately, a commercial umbrella policy is a powerful backstop. It’s the difference between weathering a severe financial storm and being completely washed away by it. By providing that extra layer of liability coverage, it shores up your financial stability and delivers invaluable peace of mind.

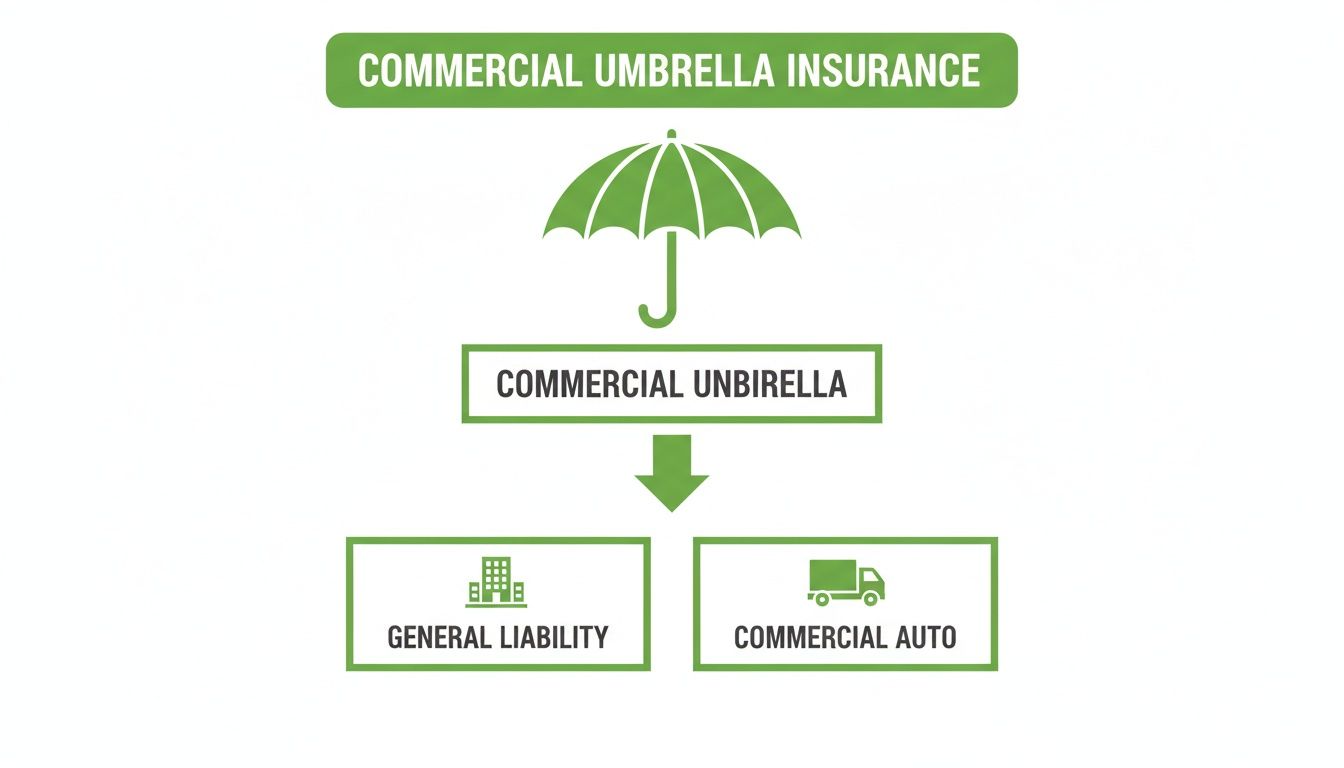

How an Umbrella Policy Actually Works

The best way to understand commercial umbrella insurance is to think of it as a second line of defense for your business. Imagine your primary liability policies—like General Liability and Commercial Auto—are your frontline soldiers. They handle the everyday skirmishes.

Your umbrella policy is the heavily armored backup, waiting in reserve. It doesn't jump into the fight until your frontline is completely overwhelmed. It’s there for the catastrophic events, the ones that threaten to wipe you out completely.

This visual shows exactly how it works, with the umbrella sitting on top of your other policies, ready to step in when they're maxed out.

It’s not a starting point for your insurance strategy; it’s the capstone that holds everything together when a major storm hits.

The Claim Trigger Mechanism

A lot of people think you can pick and choose which policy pays a claim. That's not how it works. The process is strict: your umbrella policy only kicks in after a primary policy has paid out every last dollar of its limit. This is called exhaustion.

Let’s see it in action with a real-world example:

- The Accident: A driver for your delivery service causes a major pile-up on the highway. Multiple people are seriously injured, and the final judgment against your company is $2.5 million.

- Primary Policy Steps Up: Your Commercial Auto policy has a $1 million liability limit. Your insurance company pays that full $1 million to the claimants, exhausting the policy.

- The Massive Shortfall: You’ve still got a $1.5 million bill to pay. Without any other coverage, this is coming directly out of your business's bank accounts, potentially forcing you into bankruptcy.

- Umbrella to the Rescue: This is where your umbrella policy activates. It covers the remaining $1.5 million, bridging the gap and protecting your company’s assets from being seized.

This "drop-down" feature is the heart of what makes an umbrella policy so powerful. It’s your financial safety net when a claim is far bigger than you ever anticipated.

Required Underlying Policies

You can't just buy an umbrella policy on its own. Insurers see it as a supplemental product, and they won't even give you a quote unless you have solid foundational policies already in place. It's a package deal.

Before you can get an umbrella, you’ll almost always need to have:

- General Liability Insurance: This is the absolute bare minimum. It covers things like slip-and-fall accidents on your property or damage your operations cause to a client's property.

- Commercial Auto Insurance: If your business uses vehicles for any reason, this is a must-have. It covers liability from accidents involving your company cars, trucks, or vans.

- Employer’s Liability Insurance: This is usually bundled with your Workers' Compensation policy. It protects you if an employee sues you for a work-related injury that isn't covered by standard workers' comp benefits.

An insurer’s demand for these underlying policies says it all: an umbrella is for the extraordinary, high-stakes claims, not for the day-to-day risks that your primary insurance should be handling.

It's also worth knowing that this isn't the only type of secondary insurance out there. To get a better handle on the specifics, check out our guide comparing umbrella liability vs. excess liability. Knowing the difference is key to making sure you have exactly the right protection for your company.

Real-World Scenarios Where Umbrella Coverage Saved a Business

Theory is one thing, but seeing how commercial umbrella insurance performs in the real world is another. This is where the true value becomes undeniable—in those heart-stopping moments when a business is staring down a potential financial catastrophe, only to be pulled back from the brink.

Let’s walk through a few true-to-life situations where an umbrella policy was the only thing that stood between a company’s survival and its collapse.

The Construction Site Catastrophe

Imagine a mid-sized construction firm managing a high-rise project in a busy downtown area. One afternoon, the unthinkable happens: a crane malfunctions, sending a massive steel beam plummeting to the ground. It smashes into an adjacent office building, causing severe structural damage, while falling debris injures several pedestrians below.

The legal fallout was immediate and overwhelming. Property damage claims for the neighboring building were astronomical on their own, but the personal injury lawsuits quickly piled up. In total, the claims against the construction company ballooned to $4.5 million.

Their General Liability policy had a standard $2 million limit. While that sounds like a lot, it wasn't nearly enough. The policy paid out its full limit, leaving the firm on the hook for a crushing $2.5 million shortfall. For a deeper dive into what these foundational policies cover, check out our guide on general liability claims examples.

This is where their foresight paid off. The construction firm had a $5 million commercial umbrella policy. As soon as the primary GL policy was exhausted, the umbrella coverage kicked in, paying the remaining $2.5 million in full. Without it, the company would have faced certain bankruptcy.

The Outcome: The umbrella policy bridged that critical financial gap. It allowed the company to settle all claims without liquidating assets or shutting its doors, preserving both the business and its hard-won reputation.

The Multi-Vehicle Pileup

A regional logistics company took great pride in its modern fleet and stellar safety record. But on one icy winter morning, one of their trucks lost control on the highway, jackknifed, and triggered a devastating pileup involving more than a dozen other cars.

The accident resulted in multiple serious injuries and, tragically, one fatality. The lawsuits from victims and their families were eventually consolidated into a single massive claim. After a long legal fight, the court handed down a $3 million judgment against the company for negligence.

Their Commercial Auto policy had a liability limit of $1 million per accident—a very typical amount for a commercial fleet. The insurer paid that $1 million maximum, but the company still faced a $2 million deficit. An amount that would have wiped out their cash reserves and forced them to sell off their trucks to satisfy the judgment.

Luckily, the business owner had invested in a $3 million commercial umbrella policy. The moment their auto policy maxed out, this secondary coverage activated, covering the remaining $2 million and satisfying the court's judgment completely.

Financial Breakdown of the Accident

- Total Liability Claim: $3,000,000

- Commercial Auto Payout: -$1,000,000

- Initial Shortfall: $2,000,000

- Umbrella Policy Payout: -$2,000,000

- Company's Out-of-Pocket Cost: $0 (plus deductible)

The Defamation Lawsuit That Rocked a Firm

A successful marketing consulting firm published a competitive analysis report for a major client. The report, however, contained information that was later deemed defamatory and libelous about a rival company. That rival sued for brand damage and loss of business.

The lawsuit was incredibly expensive, racking up huge legal fees over a prolonged court case. The jury ultimately sided with the rival, awarding them $1.75 million in damages. The firm’s professional liability policy (often called Errors & Omissions or E&O) had a limit of $1 million.

After the professional liability policy paid its full amount, the consulting firm was left with a $750,000 bill. For a service-based business with few physical assets, this was a potentially fatal blow.

This is exactly when their $2 million commercial umbrella policy proved its worth. It was designed to sit on top of their E&O policy, and it covered the remaining $750,000 judgment. It prevented the partners from having to pay out of their own pockets or dissolve the very business they had worked so hard to build. These scenarios prove that risk isn't just physical—it's financial and reputational, too.

Understanding Your Policy Limits, Exclusions, and Costs

Choosing the right commercial umbrella insurance isn't about just buying the biggest policy you can find. It’s about taking a clear-eyed look at the practical details—your coverage limits, what isn’t covered, and how your premium is actually calculated.

Getting these elements right is the key to securing robust protection that truly fits your budget and your company’s unique risk profile. It turns a complex decision into a confident investment in your business's future.

How Much Coverage Do You Really Need?

Commercial umbrella insurance is typically sold in increments of $1 million. While a $1 million or $2 million policy is a common starting point, the right amount for your business depends entirely on your specific risk exposure. A small local retail shop simply doesn't face the same level of liability as a large-scale construction contractor.

So, how do you land on the right number? It comes down to evaluating a few key factors:

- Your Industry: Businesses in high-risk sectors like construction, transportation, or hospitality almost always need higher limits because the potential for severe accidents is just part of the job.

- Your Assets: Add up the total value of your business assets—property, equipment, cash reserves. Your coverage needs to be sufficient to protect all of it from being seized in a lawsuit.

- Public Interaction: The more your business interacts with the public, the higher your risk. This includes everything from customers walking into your store to your fleet of vehicles on the road every day.

Think of your coverage limit as a financial shield for your business. The goal is to have a shield so large that even a catastrophic legal judgment can't get around it to drain your company’s resources.

What Commercial Umbrella Insurance Does Not Cover

Just as important as knowing what your policy covers is understanding what it doesn't. An umbrella policy is built for excess liability, not as a catch-all for every possible business risk. It follows the rules of your underlying policies, which means if a claim isn't covered by your primary General Liability or Auto policy, your umbrella won't kick in either.

There are a few common exclusions you'll find in nearly every commercial umbrella policy:

- Intentional or Criminal Acts: Damage or injuries caused deliberately by you or your employees are never covered.

- Pollution Liability: Claims related to environmental damage, like a chemical spill, require a separate, specialized environmental insurance policy.

- Your Own Property Damage: An umbrella policy is for liability—damage you cause to others. It won’t cover damage to your own buildings, equipment, or inventory.

- Professional Errors: Mistakes tied to professional services (like a consultant giving bad advice) fall under Professional Liability (E&O) insurance, not a standard umbrella.

These exclusions aren't loopholes. They exist because these are unique risks that require their own dedicated insurance products.

Key Factors That Influence Your Premium Costs

The price you pay for your commercial umbrella insurance is your premium. This cost isn't just a number pulled from a hat; it's calculated based on a detailed risk assessment by the insurer. Several factors directly impact that final number.

It's a tough market out there. While U.S. commercial insurance rates saw an aggregate increase of 5.3% in early 2025, umbrella liability has been hit with double-digit hikes for 20 straight quarters. This trend is fueled by massive "nuclear verdicts" and social inflation, where claim costs are soaring, making insurers more cautious than ever. You can read more in this detailed commercial lines survey.

The primary drivers of your premium include:

- Your Industry: A roofing company will always pay more than a graphic design studio. Why? Because its daily operations carry far greater risk of a serious accident.

- Coverage Limits: This one is straightforward—the higher the liability limit you choose, the higher your premium will be.

- Claims History: A business with a history of frequent or large liability claims is seen as higher risk and will be charged more. A clean record pays off.

- Underlying Policy Limits: Insurers require your primary policies to have certain minimum limits before they'll even offer an umbrella. Higher underlying limits can sometimes result in a lower umbrella premium.

- Your Footprint: More employees and a larger vehicle fleet naturally increase your potential for liability incidents, and your cost will reflect that.

Understanding these variables is the first step toward managing your insurance expenses. If you want to dive deeper, our guide on what an insurance premium is provides a helpful breakdown.

Does Your Business Need an Umbrella Policy?

Figuring out if you need commercial umbrella insurance isn't just a "big company" problem. In reality, it's often the small and mid-sized businesses that are most at risk from a single, catastrophic lawsuit. The question isn't if a huge claim could happen, but whether your business could actually survive it.

Think of it as a quick risk check-up. The more public interaction and physical risk your business has, the more you need that extra layer of protection. This is especially true today, with lawsuits becoming more common and jury awards hitting record highs.

Key Risk Factors to Consider

If you answer "yes" to any of the questions below, a commercial umbrella policy should be on your radar. Each "yes" points to a significant liability risk that could easily blow past the limits of your standard insurance.

- Do you have a physical location? Anytime customers, clients, or even delivery drivers step onto your property, you're on the hook for potential slip-and-fall accidents.

- Do your employees work with the public? If your team is out in the field, visiting client sites, or representing your company, their actions can create a massive liability for you.

- Do you use vehicles for business? A single, serious car accident caused by an employee can trigger multi-million dollar lawsuits that a standard auto policy won't come close to covering.

- Are you in a high-risk industry? If you're in construction, hospitality, or transportation, the potential for causing serious injury or property damage is just part of the job.

This isn't a complete list, but it covers the most common red flags. Some businesses have unique risks that demand a solid foundation of primary coverage first. For example, knowing the basic food truck insurance requirements is step one before you can even think about adding an umbrella policy on top.

Why Small Businesses Are Especially at Risk

It's a dangerous myth that only huge corporations need millions in liability coverage. A massive company might have the cash reserves to weather a $1.5 million judgment. For a small business, that same lawsuit is a death sentence. It could mean bankruptcy overnight.

This is exactly why umbrella insurance is so popular. North America is the biggest market for these policies, largely because of the legal climate in the United States. Businesses of all sizes rely on this coverage, with small-to-medium enterprises (SMEs) making up over 60% of the market. They see it as an essential shield. You can read more about this dominant market for umbrella insurance.

At its core, commercial umbrella insurance is about protecting your company's future. It's the safety net that ensures one terrible day doesn't wipe out everything you've worked so hard to build.

How to Secure the Right Umbrella Coverage

Figuring out the world of commercial umbrella insurance can feel like a lot to take on, but it gets much simpler when you break it down into a few clear steps. The idea is to move from understanding the concept to taking confident action. Your goal isn't just to add another layer of insurance, but to get real peace of mind.

The best first move? Team up with an expert. An independent agent can cut through the market's complexity, helping you sidestep the two biggest pitfalls: being underinsured and exposed, or being overinsured and paying too much. Their job is to look at how your business runs and translate that into a clear risk profile.

Finding Your Ideal Coverage Limit

Pinpointing the right coverage amount isn't a guessing game; it's a science. It demands a close look at your specific business risks—everything from the industry you're in and your day-to-day operations to your total assets and potential legal threats. A "one-size-fits-all" policy just won't cut it here.

This is where good data and analytics make a huge difference. By analyzing data points unique to your business—like the number of vehicles in your fleet, your employee headcount, and how often you interact with the public—an experienced partner can recommend a limit that makes sense. This data-driven method makes sure your policy is built for your actual needs.

This process breaks down into:

- A deep-dive risk assessment to pinpoint your unique liability exposures.

- Benchmarking against industry peers to see what coverage similar companies carry.

- Balancing the premium cost with the right level of asset protection.

The right commercial umbrella insurance is a strategic asset. It’s tailored to cover your precise risk profile, providing a strong financial backstop without straining your budget. It’s the final, critical piece in your company’s financial safety net.

The Importance of a Seamless Process

Getting coverage shouldn't be a frustrating, paper-filled nightmare. Today’s best agencies put a premium on a smooth client experience, using digital tools that make everything from the application to managing your policy a breeze. You should look for a partner offering paperless onboarding and a secure 24/7 client portal for easy access to your policy documents.

Ultimately, picking the right partner is just as critical as picking the right policy. A skilled advocate won’t just help you find a competitive price; they’ll be in your corner if you ever have to file a claim. For more on this, our guide on how to choose an insurance broker offers practical advice for finding a team that truly has your back. With the right support, you can confidently build a comprehensive shield for your business.

Frequently Asked Questions

When you start digging into commercial umbrella insurance, a few questions always seem to pop up. Let's tackle some of the most common ones that business owners ask so you can get a clearer picture.

Can I Use My Personal Umbrella Insurance for My Business?

That’s a definite no, and it's a hugely important distinction to make. Your personal umbrella policy is built to sit on top of your personal home and auto insurance. It’s strictly for non-business liability.

Your commercial umbrella insurance, on the other hand, is engineered specifically for business risks. It layers over your commercial general liability, commercial auto, and employer’s liability policies. If you tried to file a business-related claim under your personal policy, it would be denied on the spot, leaving your business assets completely vulnerable.

What's the Minimum Coverage I Should Get?

You'll typically see commercial umbrella policies sold in increments of $1 million. For many small businesses, a $1 million policy is a solid starting point, but there's really no one-size-fits-all answer.

The right amount of coverage boils down to your unique risk profile. A good insurance advisor will walk you through an assessment of your industry, annual revenue, number of employees, and company assets. The ultimate goal is to have enough coverage to shield your business's net worth if a truly catastrophic lawsuit lands at your door.

Does an Umbrella Policy Cover Absolutely Everything?

An umbrella policy is a powerful safety net, but it doesn't cover every conceivable risk. Think of it as an extender for your existing liability policies, not a catch-all. If a claim isn't covered by your underlying general liability or commercial auto policy in the first place, your umbrella policy won't cover it either.

There are a few standard exclusions to be aware of. These often include:

- Intentional or criminal acts

- Damage to your own business property

- Pollution-related claims

- Professional mistakes (that's what a separate Errors & Omissions policy is for)

It's designed to handle the same kinds of events as your primary policies, just with a much higher dollar limit. For a deeper dive on specific scenarios, you might want to look into Can Umbrella Insurance Cover Me In The Event Of An Accident.

Protecting your business from a devastating financial blow shouldn't feel overwhelming. At Wexford Insurance Solutions, we pair smart analytics with dedicated service to help you secure the right commercial umbrella insurance with total confidence. Contact us today for a comprehensive risk assessment.

How much is engagement ring insurance: a clear guide to costs and coverageYour Guide to Errors & Omissions Insurance

How much is engagement ring insurance: a clear guide to costs and coverageYour Guide to Errors & Omissions Insurance